Quarter Ended: March 2026

Bank of Maharashtra – Q4 FY26 Results Analysis

NSE

mahabank

BSE

532525

Bank of Maharashtra delivered a fundamentally strong quarter with improved profitability, strong segment performance, healthy asset quality, and stable operating metrics.

key financial highlights

- Revenue from Operations:

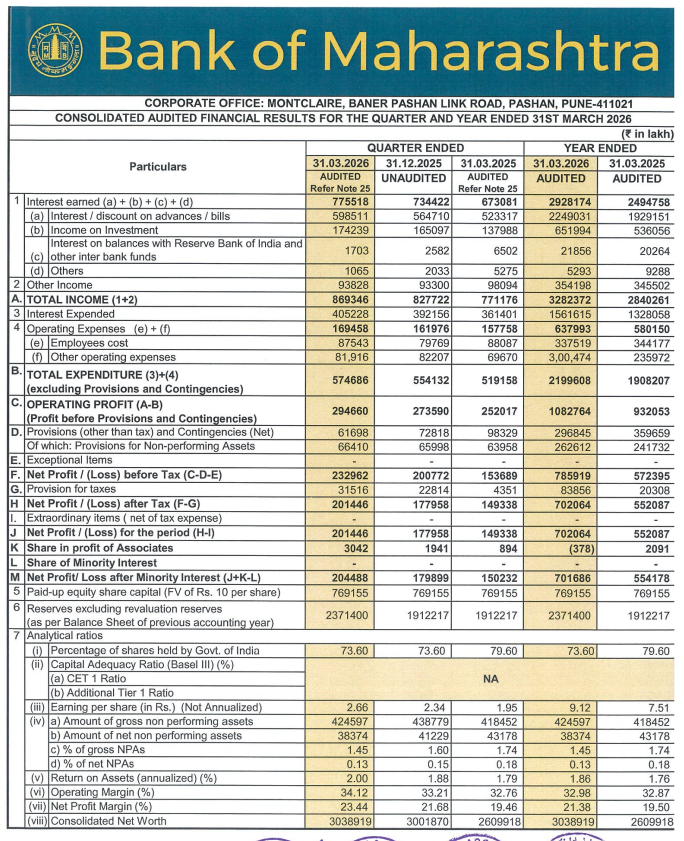

- Total Income (Q4 FY26): ₹869,346 lakh

- QoQ Change: +0.18%

- YoY Change: +11.80%

- Previous Quarter (Q3 FY26): ₹867,722 lakh

- Previous Year (Q4 FY25): ₹777,176 lakh

- Total Income (Q4 FY26): ₹869,346 lakh

- Revenue remained stable sequentially while maintaining double-digit growth YoY, reflecting continued growth in core banking operations.

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹204,488 lakh

- QoQ Growth: +14.93%

- YoY Growth: +36.08%

- Previous Quarter: ₹177,958 lakh

- Previous Year: ₹150,232 lakh

- PAT (Q4 FY26): ₹204,488 lakh

- Strong profit growth was driven by:

- Improved operating profit

- Lower sequential provisions

- Strong Treasury and Wholesale performance

- Better operating leverage

Margin Analysis

- Operating profit rose faster than expenses

- Provisions declined sharply YoY

- Net profit margin expanded

- Return on Assets improved

Key Signal: Margins improved due to Better cost control, Lower credit costs, Improved operating leverage

Segment performance

Treasury Operations

| Segment | Q4 FY26 | Y.O.Y |

|---|---|---|

| Revenue | ₹177,923 lakh | +15.39% |

| Segment Profit | ₹30,207 lakh | -16.11% |

Corporate / Wholesale Banking

| Segment | Q4 FY26 | Y.O.Y |

|---|---|---|

| Revenue | ₹294,606 lakh | +14.55% |

| Segment Profit | ₹105,131 lakh | +29.61% |

Retail Banking

| Segment | Q4 FY26 | Y.O.Y |

|---|---|---|

| Revenue | ₹396,045 lakh | +19.64% |

| Segment Profit | ₹93,456 lakh | +152.90% |

Other Banking Operations

| Segment | Q4 FY26 | Q4 FY25 |

| Revene Softened | ₹9,214 lakh | ₹12,834 lakh |

Segment Insight:

Strength Areas

- Retail Banking profitability surge

- Corporate/Wholesale stability

- Treasury revenue growth

- Diversified segment contribution

Weak Areas

- Other Banking Operations softness

- Treasury profitability moderation

Overall segment structure remains strong

Earning quality check

High Earnings Quality:

- Profit growth appears operationally driven rather than one-off driven

Supported By:

- Lower provisions

- Stable revenue growth

- Operating leverage

- Asset quality improvements

Interpretation:

This is high-quality earnings expansion

balance sheet analysis

Segment Assets

- FY26: ₹4,27,47,102 lakh

- FY25: ₹3,69,35,381 lakh

- Growth: +15.74%

Capital & Reserves

- FY26: ₹33,22,426 lakh

- FY25: ₹28,70,798 lakh

- Growth: +15.73%

Asset Quality

- Gross NPA: 1.45% (vs 1.74% last year)

- Net NPA: 0.13% (vs 0.18% last year)

Cash flow analysis

Operating Cash Flow

- Negative ₹1,13,36.03 lakh

- Interpretation:

- Driven by working capital and operating asset growth

- Needs monitoring, though common in balance sheet-heavy banks

Financing Cash Flow

- Negative ₹26,07.12 lakh

- Reflects:

- Dividend payouts

- Bond servicing

- Interest on borrowings

Cash Position

- FY26: ₹2,77,45.60 lakh

- FY25: ₹4,21,94.91 lakh

Indicates: Liquidity moderated

key risks

- Important monitoring factor

- Profit declined despite revenue growth

- Cash balance declined materially

management strategy signals

- Retail growth acceleration

- Wholesale strength

- Credit quality improvement

- Capital strengthening

- Efficiency-led profitability

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹869,346 Lakh | +0.18% | +11.80% |

| PBT | ₹232,962 Lakh | +16.09% | +51.51% |

| PAT | ₹204,488 Lakh | +14.93% | +36.08% |

| EPS | ₹2.66 | +13.68% | +36.41% |

Bank of Maharashtra delivered:

- Strong PAT growth

- Lower provisions

- Improved asset quality

- Strong retail banking performance

- Healthy margins

- Capital growth

Official Exchange Filing: Bank of Maharashtra

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED