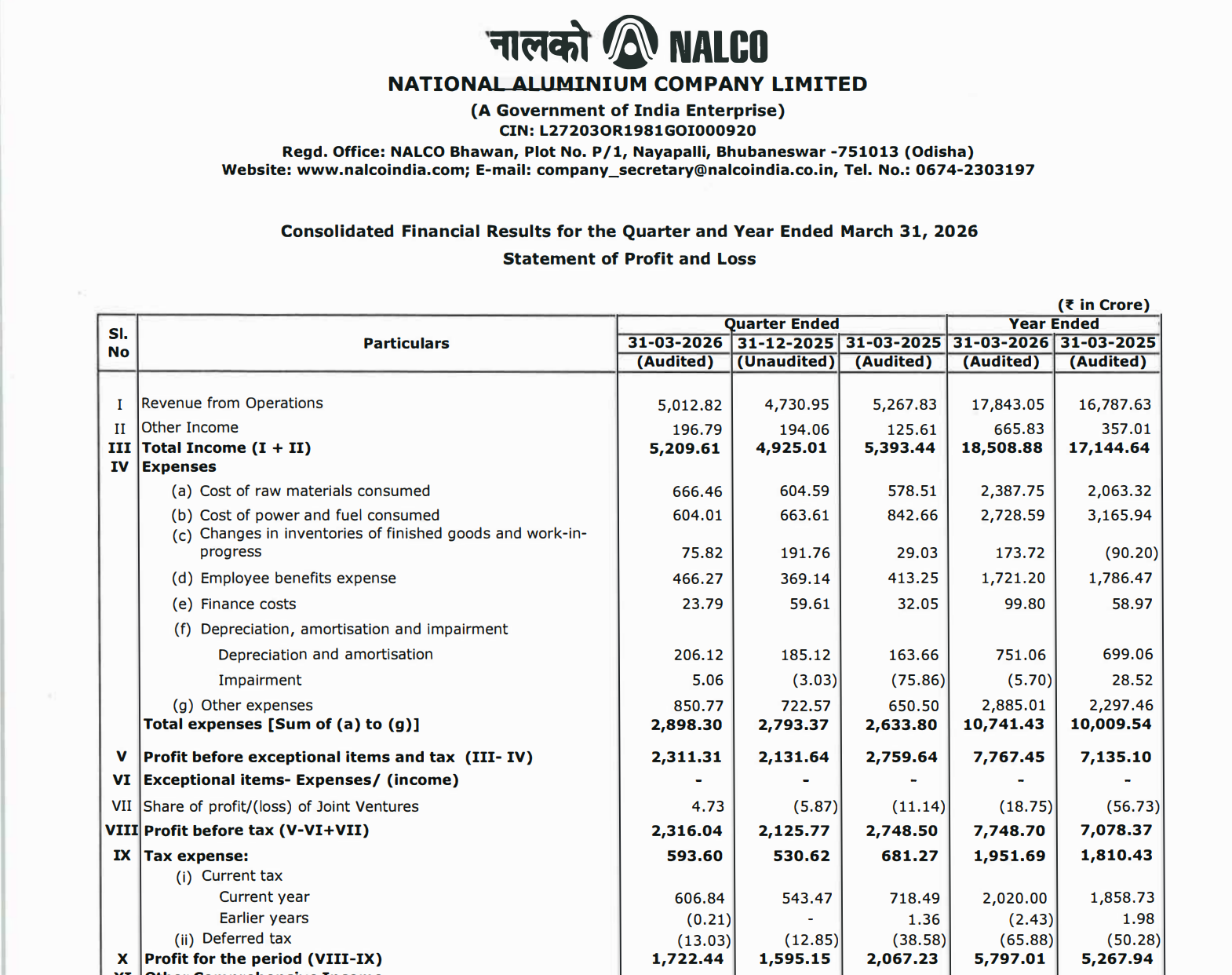

Quarter Ended: March 2026

National Aluminium Company Ltd (NALCO) – Q4 FY26 Results

NSE

NATIONALUM

BSE

532234

NALCO delivered stable topline growth QoQ, but rising cost structure and commodity normalization led to YoY profit decline.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹5,012.82 Cr

- QoQ Change: +6.0%

- YoY Change: -4.8%

- Previous Quarter (Q3 FY26): ₹4,730.95 Cr

- Previous Year (Q4 FY25): ₹5,267.83 Cr

- Revenue (Q4 FY26): ₹5,012.82 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹1,722.44 Cr

- QoQ Change: +7.9%

- YoY Change: -16.7%

- Previous Quarter (Q3 FY26): ₹1,595.15 Cr

- Previous Year (Q4 FY25): ₹2,067.23 Cr

- PAT (Q4 FY26): ₹1,722.44 Cr

- QoQ Performance

- Revenue Trend: Improved

- Profit Trend: Improved

Margin Analysis

Drivers:

- Increase in power & fuel cost

- Higher raw material consumption cost

- Moderation in aluminium realizations

Insight:

- Margins are compressing YoY, indicating cost pressure despite stable operations

Segment performance

Segment: Aluminium

- Revenue: ₹3,894.52 Cr

- Insights:

- Core revenue contributor (~75%)

- Strong QoQ recovery

- Sensitive to global aluminium prices

Segment: Chemical

- Revenue: ₹1,575.31 Cr

- Insights:

- Stable but declining YoY

- Lower margin compared to aluminium

Segment insight

Summary:

- NALCO operates in a commodity-driven structure where aluminium dominates revenue and profitability

Charcateristics:

- Highly cyclical earnings

- Dependent on global metal prices

- Energy-intensive operations

- PSU-driven strategic decisions

Earning quality check

Drivers:

- No major exceptional items

- Core operations driving earnings

- Stable cash-backed profits

Interpretations:

- Earnings are clean but cyclical, with no artificial boost

balance sheet Analysis

- Total Assets: ₹26,544.40 Cr

- Total Liabilities: ₹4,940.69 Cr

Insight:

- Strong balance sheet with low leverage and high equity base

key risks

- Aluminium price volatility

- Rising energy costs

- Global demand slowdown

- PSU policy-related constraints

management strategy signals

Focus Area:

- Cost optimization (especially power efficiency)

- Increasing production efficiency

- Expansion into value-added products

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹5,012.82 Cr | +6.0% | -4.8% |

| Total Expense | ₹2,898.30 Cr | +3.8% | +10.0% |

| Net Profit | ₹1,722.44 Cr | +7.9% | -16.7% |

NALCO remains financially strong with robust cash flows and a solid balance sheet. However, profitability is entering a cyclical downtrend due to rising costs and softer commodity pricing. Future performance will depend heavily on aluminium price trends and energy cost control.

Official Exchange Filing: National Aluminium Company Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

58%

NET PROFIT AS % OF REVENUE

34%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED