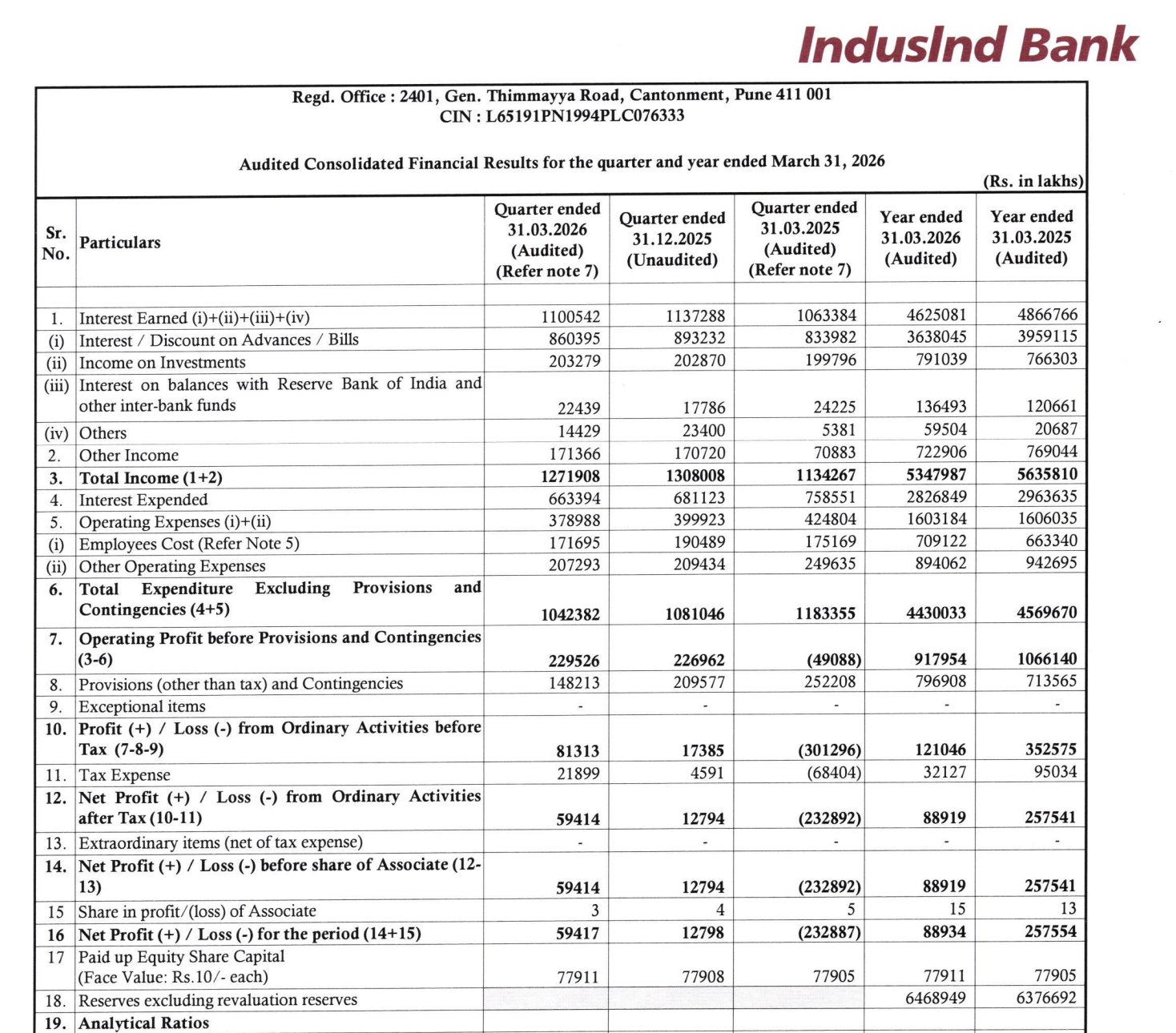

Quarter Ended: March 2026

IndusInd Bank Ltd – Q4 FY26 Financial Results Analysis

NSE

indusindbk

BSE

532187

While core income remained stable, high provisions and contingencies significantly impacted profitability, resulting in sharp YoY earnings decline

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹12,71,908 Lakhs

- QoQ Change: -2.77%

- YoY Change: +12.14%

- Previous Quarter (Q3 FY26): ₹13,08,008 Lakhs

- Previous Year (Q4 FY25): ₹11,34,267 Lakhs

- Total Income (Q4 FY26): ₹12,71,908 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹59,417 Lakhs

- QoQ Change: +364.30%

- YoY Change: -74.49%

- Previous Quarter (Q3 FY26): ₹12,798 Lakhs

- Previous Year (Q4 FY25): ₹2,32,887 Lakhs

- PAT (Q4 FY26): ₹59,417 Lakhs

- QoQ Performance

- Revenue Trend: Slight decline

- Profit Trend: Sharp recovery (low base)

Margin Analysis

Key Drivers:

- High provisions & contingencies (₹1,48,213 Lakhs)

- Pressure on asset quality

- Stable operating income but weak bottom-line conversion

- Elevated credit cost

Key Signal: Margins severely compressed YoY due to provisioning spike, indicating stress in loan book quality

Segment performance

Segment: Retail Banking

- Revenue: ₹8,16,145 Lakhs

Insights:

- Largest contributor

- Weak YoY performance

Segment: Treasury Operations

- Revenue: ₹2,63,778 Lakhs

Insights:

- Volatile earnings

- Impacted overall stability

Segment: Corporate / Wholesale Banking

- Revenue: ₹3,00,948 Lakhs

Insights:

- Stable segment

- Moderate contribution

Segment: Treasury Operations

- Revenue: ₹2,63,778 Lakhs

Insights:

- Volatile earnings

- Impacted overall stability

Segment: Other Banking Operations

- Revenue: ₹311 Lakhs

Insights:

- Negligible contribution

Segment insight

Summary:

- Retail banking dominates revenue but is likely the source of stress due to rising NPAs and provisions

Characteristics:

- Retail-heavy loan book

- Exposure to credit cycles

- Segment imbalance risk

Earning quality check

Drivers:

- High provisioning impacting net profit

- Core operating income intact

- No exceptional income support

- Weak profit conversion ratio

Interpretation:

- Earnings quality is weak due to elevated credit costs and stress in asset quality

balance sheet Analysis

- Total Assets: ₹5,43,393.92 Lakhs

- Total Liabilities: ₹5,43,393.92 Lakhs

Insight:

- Balance sheet remains large and stable, but loan book contraction and rising provisions indicate caution

key risks

- Rising NPAs (Gross NPA: 3.43%)

- Elevated credit cost

- Weak return ratios (ROA decline)

- Pressure in retail loan segment

management strategy signals

- Focus Areas:

- Asset quality improvement

- Reduction in NPAs

- Strengthening risk management

- Controlled lending growth

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹12,71,908 Lakhs | -2.77% | +12.14% |

| PBT | ₹81,313 Lakhs | +367.70% | -73.02% |

| PAT | ₹59,417 Lakhs | +364.30% | -74.49% |

IndusInd Bank reported a weak quarter marked by a sharp decline in profitability despite stable income growth. Elevated provisions and asset quality concerns remain the key overhang. While QoQ recovery is visible, the overall trend indicates stress in the lending book, making this a cautious outlook

Official Exchange Filing: IndusInd Bank Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED