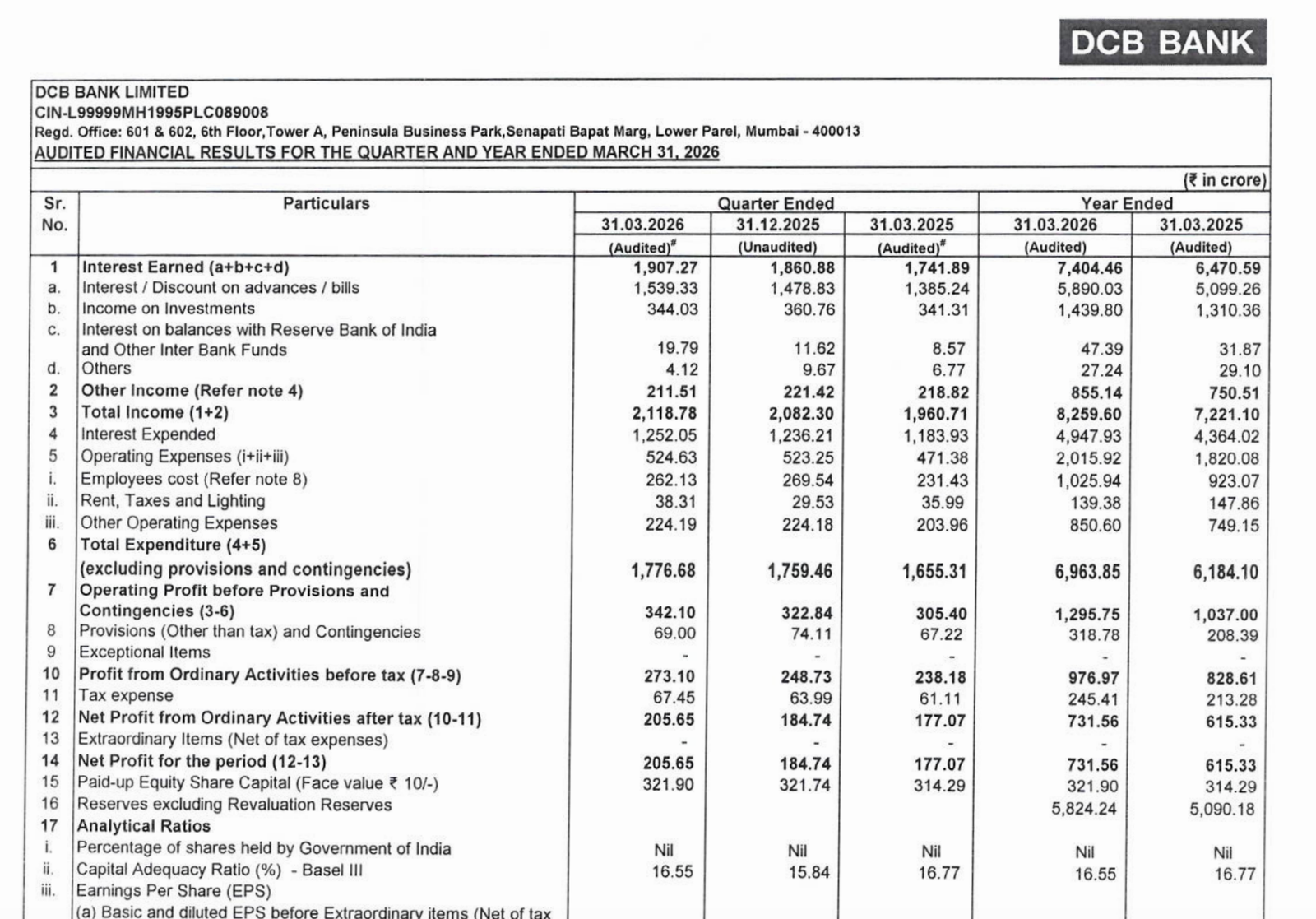

Quarter Ended: March 2026

DCB Bank Ltd – Q4 FY26 Financial Results Analysis

NSE

dcbbank

BSE

532772

The bank delivered stable growth in income and profitability with improving asset quality metrics and controlled provisions, indicating strengthening fundamentals.

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹2,118.78 Cr

- QoQ Change: +1.75%

- YoY Change: +8.06%

- Previous Quarter (Q3 FY26): ₹2,082.30 Cr

- Previous Year (Q4 FY25): ₹1,960.71 Cr

- Total Income (Q4 FY26): ₹2,118.78 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹205.65 Cr

- QoQ Change: +11.32%

- YoY Change: +16.14%

- Previous Quarter (Q3 FY26): ₹184.74 Cr

- Previous Year (Q4 FY25): ₹177.07 Cr

- PAT (Q4 FY26): ₹205.65 Cr

- QoQ Performance

- Revenue Trend: Stable growth

- Profit Trend: Moderate growth

Margin Analysis

Key Drivers:

- Stable Net Interest Income growth

- Controlled operating expenses

- Moderate provisioning levels

- Stable cost-to-income ratio

Key Signal: Margins remain stable with slight improvement, supported by controlled costs and steady lending spreads

Segment performance

Segment: Retail Banking

- Revenue: ₹1,793.13 Cr

Insights:

- Largest contributor

- Strong and consistent growth driver

Segment: Treasury Operations

- Revenue: ₹461.59 Cr

Insights:

- Volatile contribution

- Decline QoQ and YoY

Segment: Corporate / Wholesale Banking

- Revenue: ₹142.74 Cr

Insights:

- Smaller contribution

- Improving profitability

Segment: Other Banking Operations

- Revenue: ₹59.77 Cr

Insights:

- Stable ancillary contribution

Segment insight

Summary:

- Retail banking continues to dominate growth, while treasury income remains volatile.

Characteristics:

- Retail-focused lending model

- Diversified banking segments

- Improving segment profitability mix

Earning quality check

Drivers:

- Core banking income growth

- Controlled credit provisioning

- Strong operating cash flow generation

- No exceptional income dependency

Interpretation:

- Earnings quality is strong with sustainable core income and improving asset quality

balance sheet Analysis

- Total Assets: ₹88,069.47 Cr

- Total Liabilities: ₹81,534.48 Cr

Insight:

- Healthy balance sheet with strong deposit growth and improving advances book

key risks

- Exposure to retail credit cycles

- Interest rate sensitivity

- Treasury income volatility

- Competitive banking environment

management strategy signals

- Focus Areas:

- Retail loan growth

- Deposit franchise expansion

- Asset quality improvement

- Cost optimization

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹2,118.78 Crore | +1.75% | +8.06% |

| PBT | ₹273.10 Crore | +9.80% | +14.67% |

| PAT | ₹205.65 Crore | +11.32% | +16.14% |

DCB Bank delivered a steady quarter with consistent income growth and improving profitability. The bank’s focus on retail lending and asset quality is yielding results, though margin expansion remains gradual. Overall, the performance indicates stable and improving fundamentals

Official Exchange Filing: DCB Bank Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED