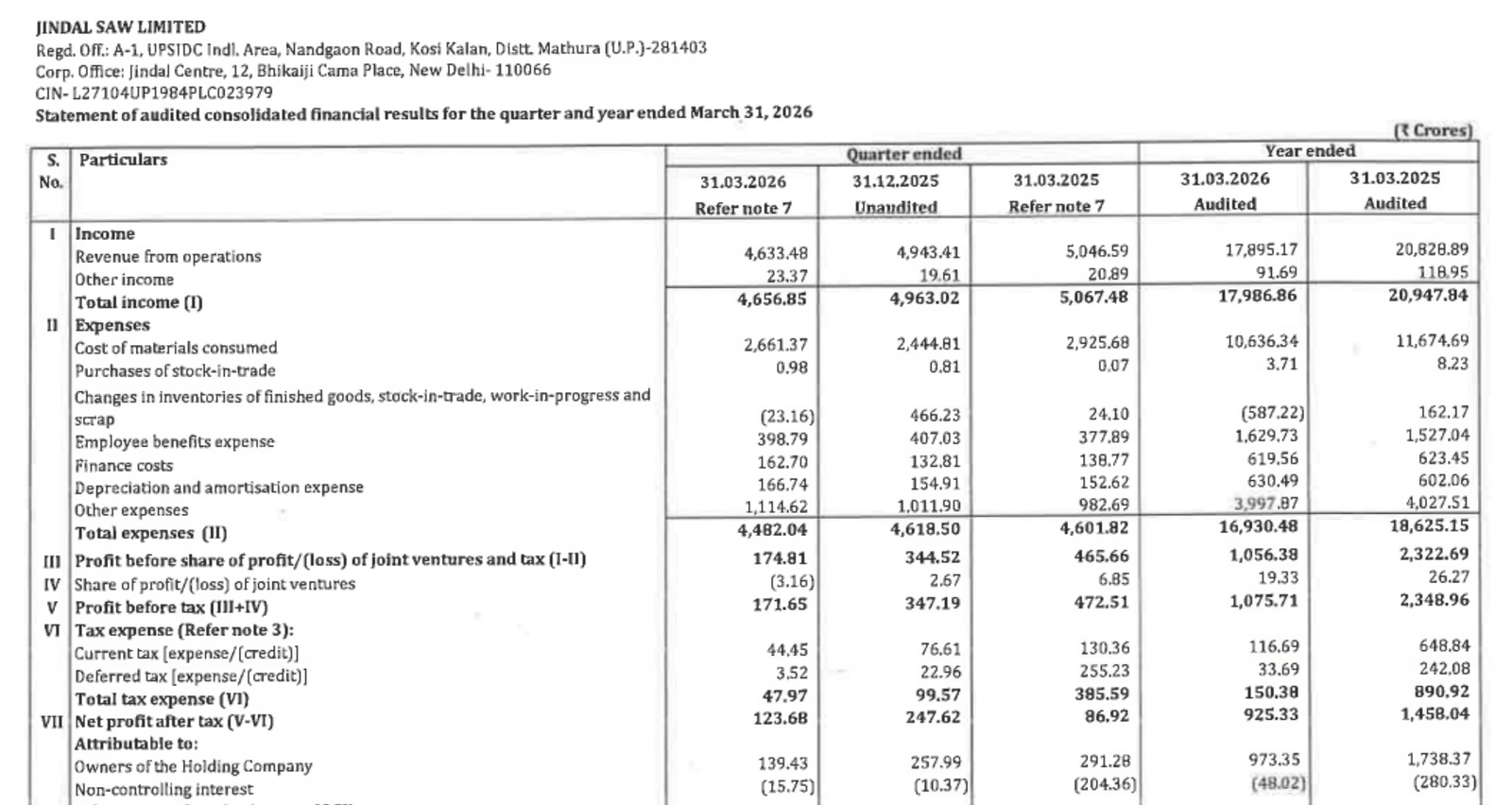

Quarter Ended: March 2026

Jindal Saw Limited – Q4 FY26 Results Analysis

NSE

jindalsaw

BSE

500378

Revenue contraction and margin compression have significantly impacted profitability, although operational cash flow remains resilient

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹4,633.48 Cr

- QoQ Change: -6.27%

- YoY Change: -8.18%

- Previous Quarter (Q3 FY26): ₹4,943.41 Cr

- Previous Year (Q4 FY25): ₹5,046.59 Cr

- Total Income (Q4 FY26): ₹4,633.48 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹123.68 Cr

- QoQ Change: -50.04%

- YoY Change: +42.29%

- Previous Quarter (Q3 FY26): ₹247.62 Cr

- Previous Year (Q4 FY25): ₹86.92 Cr

- PAT (Q4 FY26): ₹123.68 Cr

- QoQ Performance

- Revenue Trend: Declining

- Profit Trend: Sharp Decline

Margin Analysis

Key Drivers:

- Decline in operating revenue

- High fixed cost structure (employee + depreciation stable)

- Elevated finance costs (~₹162 Cr)

- Weak operating leverage

Key Signal: Severe margin compression, indicating demand slowdown and inability to absorb fixed costs

Earning quality check

Drivers:

- Lower core operating profit

- Reduced joint venture contribution

- Impact from inventory adjustments

Interpretation:

- Earnings quality is weak, with profitability heavily impacted by operational inefficiencies and demand pressure

balance sheet Analysis

- Total Assets: ₹21,686.20 Cr

- Total Liabilities: ₹9,403.49 Cr

Insight:

- Equity strengthened to ₹12,282 Cr

- Debt levels remain elevated (~₹4,000 Cr+ borrowings combined)

- Cash declined to ₹406.72 Cr vs ₹655.42 Cr YoY → liquidity tightening

key risks

- Demand slowdown in pipes & infrastructure sector

- High operating leverage risk

- Declining cash position

- Exposure to commodity price volatility

- Weak profitability impacting future growth

management strategy signals

Focus Area:

- Cost optimization

- Working capital management

- Focus on core business segments

- Maintaining operational efficiency

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹4,656.85 Crore | -6.18% | -8.11% |

| PBT | ₹171.65 Crore | -50.56% | -63.67% |

| PAT | ₹123.68 Crore | -50.04% | +42.29% |

Jindal Saw is currently in a margin stress phase, with declining revenue and sharp drop in profitability signaling weak operating conditions. While cash flow from operations remains decent, the earnings profile is deteriorating, making the near-term outlook cautious unless demand revival or cost control improves.

Official Exchange Filing: Jindal Saw Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

96%

NET PROFIT AS % OF REVENUE

3%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED