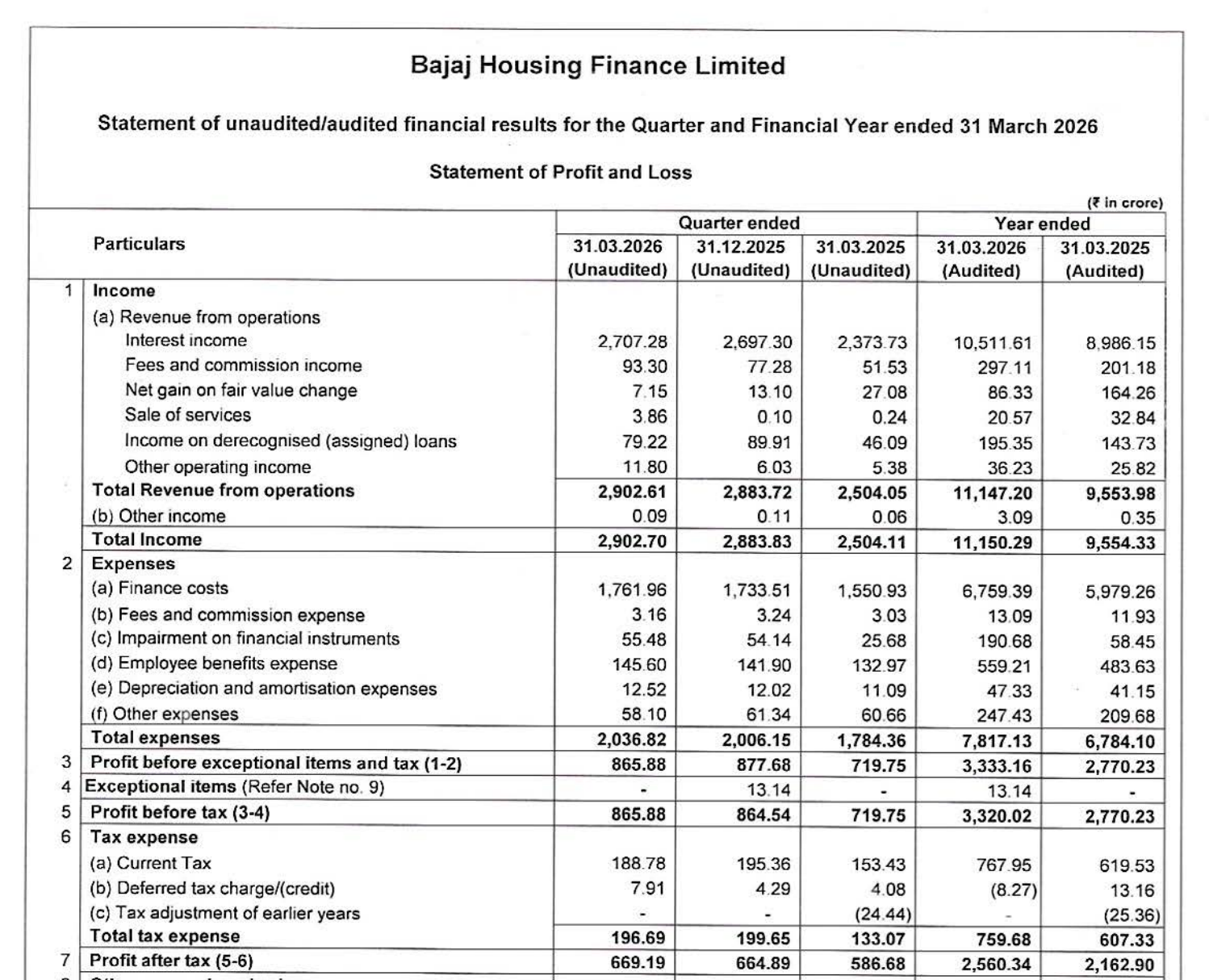

Quarter Ended: March 2026

Bajaj Housing Finance Ltd – Q4 FY26 Results Analysis

NSE

bajajhfl

BSE

544252

Revenue growth remains strong YoY, but profitability expansion is getting moderated due to rising borrowing costs and higher provisions

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹2,902.61 Cr

- QoQ Change: +0.65%

- YoY Change: +15.91%

- Previous Quarter (Q3 FY26): ₹2,883.72 Cr

- Previous Year (Q4 FY25): ₹2,504.05 Cr

- Total Income (Q4 FY26): ₹2,902.61 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹669.19 Cr

- QoQ Change: +0.65%

- YoY Change: +14.07%

- Previous Quarter (Q3 FY26): ₹664.89 Cr

- Previous Year (Q4 FY25): ₹586.68 Cr

- PAT (Q4 FY26): ₹669.19 Cr

- QoQ Performance

- Revenue Trend: Flat to Slightly Positive

- Profit Trend: Stable

Margin Analysis

Key Drivers:

- Rising finance costs (₹1,761.96 Cr, major expense driver)

- Increase in impairment on financial instruments

- Stable operating income growth offsetting cost pressure

Key Signal: Margins are under pressure, indicating cost of funds is rising faster than yield expansion

Earning quality check

Drivers:

- Strong growth in interest income (₹2,707 Cr)

- Increase in loan book (₹1.23 lakh Cr)

- Rising impairment charges

Interpretation:

- Earnings are core-operating driven, but rising credit cost and finance cost indicate moderate quality pressure

balance sheet Analysis

- Total Assets: ₹1,27,147 Cr

- Total Liabilities: ₹1,04,624 Cr

Insight:

- Strong loan book expansion (~24% YoY)

- Borrowings increased significantly → indicates aggressive growth strategy

- Liquidity improved (cash ₹161.8 Cr vs ₹61.6 Cr YoY)

key risks

- Rising interest rates impacting margins

- Increasing credit cost / impairments

- Heavy dependence on borrowed funds

- NBFC sector liquidity sensitivity

management strategy signals

Focus Area:

- Aggressive loan book expansion

- Focus on interest income growth

- Strengthening capital base & liquidity

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹2,902.70 Crore | +0.65% | +15.91% |

| PBT | ₹865.88 Crore | +0.15% | +20.30% |

| PAT | ₹669.19 Crore | +0.65% | +14.07% |

Bajaj Housing Finance continues to deliver consistent growth backed by strong loan expansion, but profitability is entering a consolidation phase due to rising funding costs and impairments. The business remains structurally strong, but near-term upside may be limited unless margin pressures ease.

Official Exchange Filing: Bajaj Housing Finance Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

70%

NET PROFIT AS % OF REVENUE

23%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED