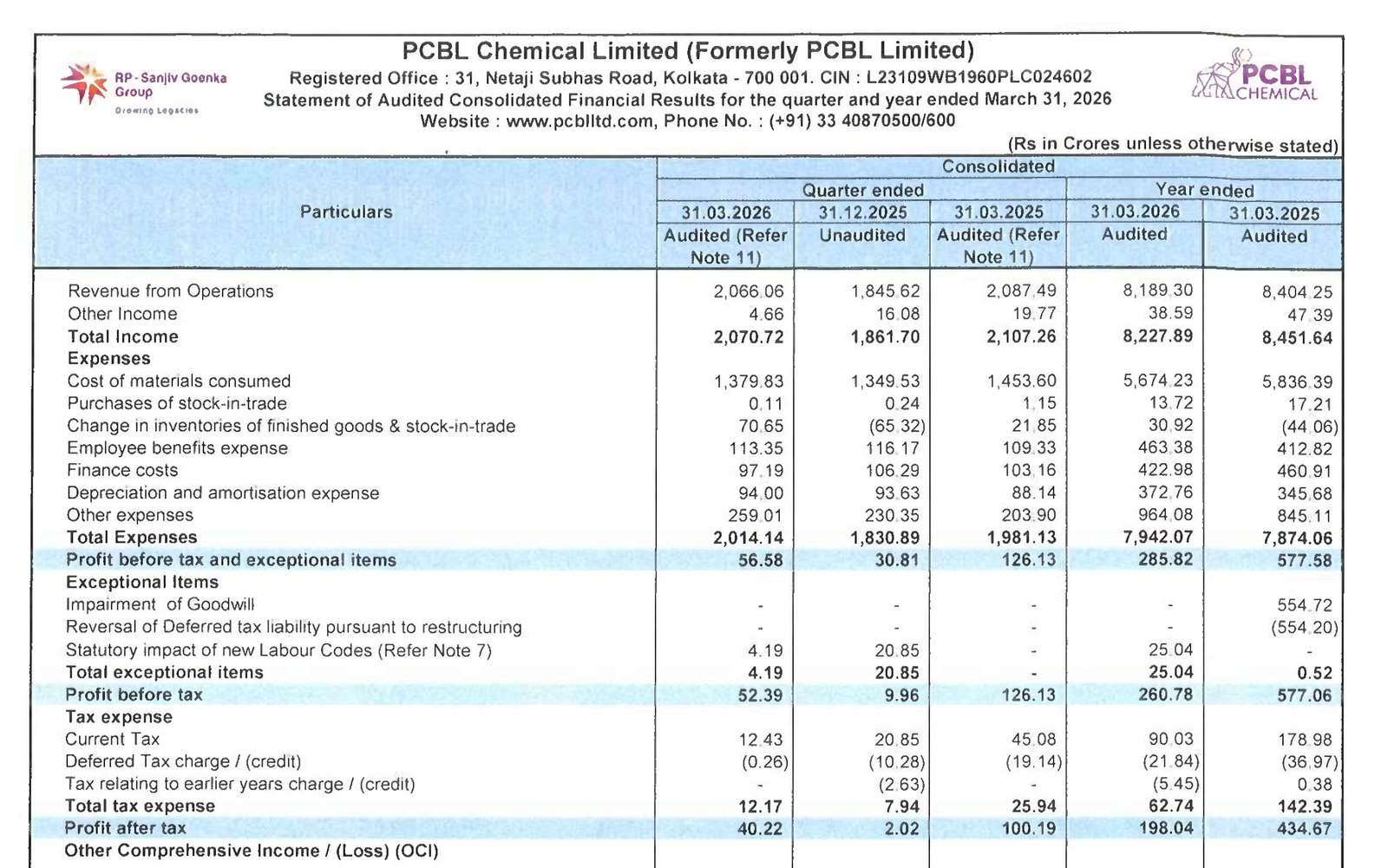

Quarter Ended: March 2026

PCBL Chemical Ltd – Q4 FY26 Results

NSE

pcbl

BSE

506590

While QoQ recovery is visible, profitability remains significantly below last year due to margin compression and weak chemical segment contribution

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹2,066.06 Cr

- QoQ Change: +11.0%

- YoY Change: -1.0%

- Previous Quarter (Q3 FY26): ₹1,845.62 Cr

- Previous Year (Q4 FY25): ₹2,087.49 Cr

- Revenue (Q4 FY26): ₹2,066.06 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹40.22 Cr

- QoQ Change: +1891%

- YoY Change: -59.9%

- Previous Quarter (Q3 FY26): ₹2.02 Cr

- Previous Year (Q4 FY25): ₹100.19 Cr

- PAT (Q4 FY26): ₹40.22 Cr

- QoQ Performance

- Revenue Trend: Strong recovery

- Profit Trend: Sharp rebound (low base driven)

Margin Analysis

Drivers:

- Significant decline in operating margins YoY

- High finance costs relative to operating profit

- Weak realization in carbon black segment

Insight:

- Margin compression remains the biggest concern despite QoQ improvement

Segment performance

Segment: Carbon Black

- Revenue: ₹1,680.58 Cr

- Core revenue contributor (~81%)

- Margins under pressure YoY

Segment: Power

- Revenue: ₹81.54 Cr

- Stable and predictable contribution

Segment: Chemical

- Revenue: ₹338.54 Cr

- Weak profitability despite stable revenue

Segment insight

Summary:

- Business is heavily dependent on carbon black, with chemical diversification still not contributing meaningfully to profits

Charcateristics:

- Cyclical commodity-linked business

- High dependence on spreads (raw material vs selling price)

- Early-stage specialty chemical expansion

Earning quality check

Drivers:

- Low PAT due to weak operating margins

- No major exceptional support in Q4

- Earnings recovery largely base-effect driven

Interpretations:

- Earnings quality is moderate; recovery is not yet structurally strong

balance sheet Analysis

- Total Assets: ₹11,294.54 Cr

- Total Liabilities: ₹7,275.39 Cr

Insight:

- Stable balance sheet with moderate leverage; no aggressive debt buildup

Cash flow analysis

Operating Cash Flow: ₹1,576.04 Cr (Strong improvement)

Investing Cash Flow: ₹(675.18 Cr)

Financing Cash Flow: ₹(989.87 Cr)

Insight:

- Strong operating cash generation but heavy financing outflows indicate debt servicing pressure

key risks

- Commodity price volatility (carbon black spreads)

- Weak margin sustainability

- Dependence on tyre industry demand

- Underperformance of chemical segment

management strategy signals

Focus Area:

- Expansion in specialty chemicals

- Margin improvement initiatives

- Cost optimization

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹2,066.06 Cr | +11.9% | -1.0% |

| EBITDA | ₹227.82 Cr | +20.6% | -17.8% |

| PAT | ₹40.22 Cr | +1891% | -59.9% |

PCBL is showing early signs of recovery on a sequential basis, but structurally the business is still facing margin pressure. The real trigger for re-rating will be sustained margin improvement and successful scale-up of the chemical segment

Official Exchange Filing: PCBL Chemical Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

97%

NET PROFIT AS % OF REVENUE

1.94%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED