Quarterly & Annual Financial Results

TCC Concept Reports Strong FY26 Growth with Revenue Surging 121% YoY Driven by Platform Expansion and Strategic Acquisitions

NSE

tcc

BSE

512038

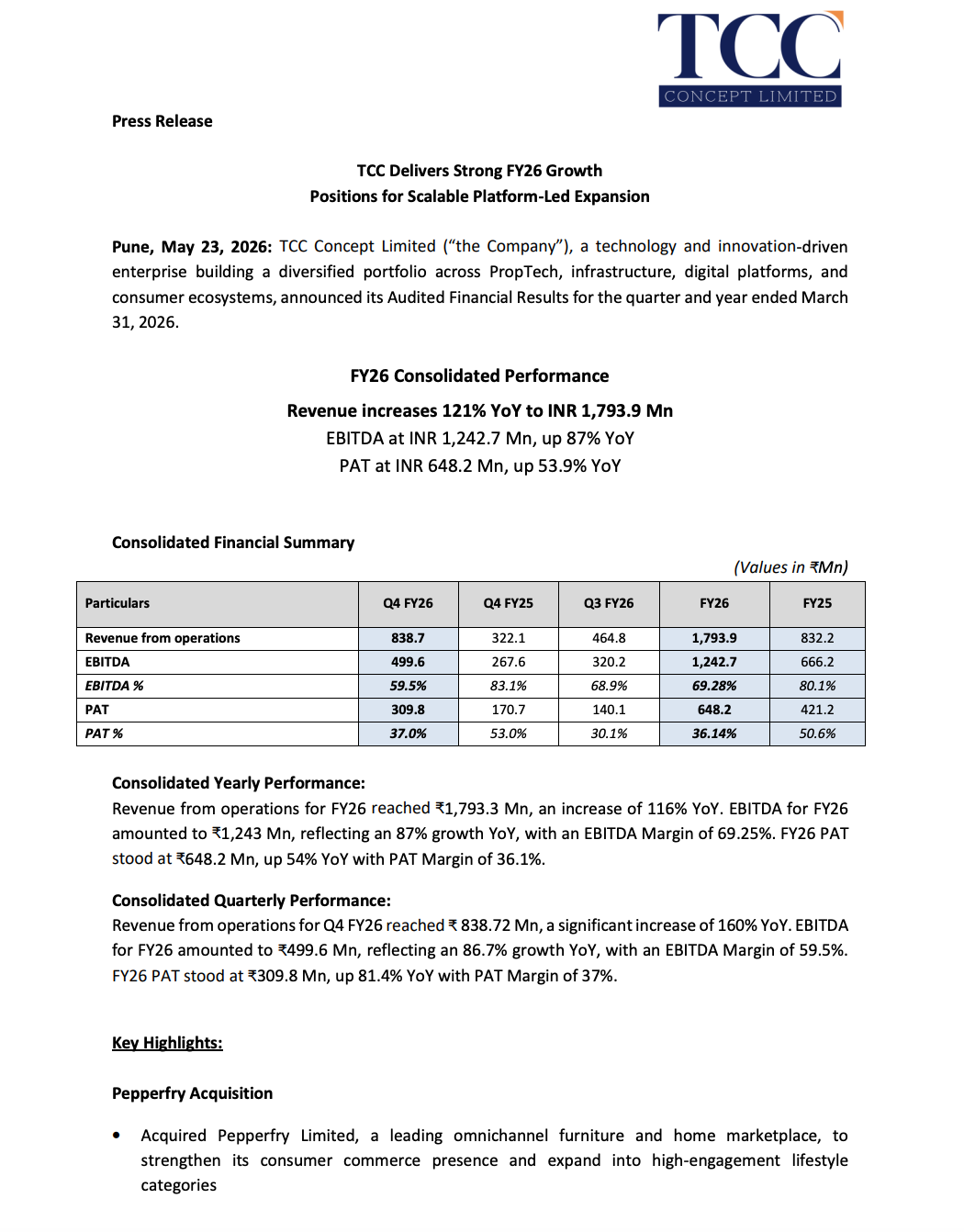

TCC Concept Limited reported robust FY26 audited consolidated performance with revenue rising 121% YoY to ₹179.39 crore while PAT increased 53.9% YoY to ₹64.82 crore. Growth was supported by acquisitions including Pepperfry and Pepcart, expansion in digital infrastructure platforms, and continued scaling of its technology-led ecosystem strategy.

PRICE-SENSITIVE TRIGGER

Event: FY26 Audited Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company reported sharp revenue and earnings growth alongside expansion across e-commerce, digital supply chain infrastructure, AI-led platforms, and consumer ecosystem businesses.

Key Metrics:

- FY26 Revenue from Operations:

- ₹179.39 crore

- Up 121% YoY from ₹83.22 crore

- FY26 EBITDA:

- ₹124.27 crore

- Up 87% YoY from ₹66.62 crore

- FY26 PAT:

- ₹64.82 crore

- Up 53.9% YoY from ₹42.12 crore

- FY26 EBITDA Margin:

- 69.28%

- Vs 80.1% in FY25

- FY26 PAT Margin:

- 36.14%

- Vs 50.6% in FY25

- Q4 FY26 Revenue:

- ₹83.87 crore

- Up nearly 160% YoY

- Q4 FY26 EBITDA:

- ₹49.96 crore

- Up 86.7% YoY

- Q4 FY26 PAT:

- ₹30.98 crore

- Up 81.4% YoY

- Q4 FY26 EBITDA Margin:

- 59.5%

- Q4 FY26 PAT Margin:

- 37%

Highlight:

- FY26 revenue more than doubled to ₹179.39 crore, reflecting aggressive expansion across platform-led businesses and strategic acquisitions.

What Happened ?

TCC Concept Limited announced strong FY26 audited consolidated financial results driven by rapid scaling of its technology-led ecosystem strategy spanning PropTech, consumer commerce, infrastructure, AI-driven solutions, and digital platforms.

The company completed multiple strategic initiatives during FY26, including:

- Acquisition of Pepperfry

- Integration of Pepcart

- Launch of MyFlopy.com

- Expansion into AI-driven property intelligence through TryThat.ai

- Growth in data infrastructure through NES Data

Management highlighted that the company is building an integrated ecosystem across:

- Consumer commerce

- Supply chain infrastructure

- Digital intelligence

- Data infrastructure

- Platform-led technology services

The company stated that FY26 growth was supported by:

- Platform integration

- Operational efficiencies

- Expansion into high-growth digital sectors

- Increasing recurring revenue streams

Key Details

Strategic and Operational Highlights

- Pepperfry acquisition strengthened TCC’s presence in omnichannel furniture and home commerce.

- The acquisition enhanced:

- Brand visibility

- Consumer engagement

- Supply chain scale

- E-commerce execution capabilities

- Pepcart integration improved digital supply chain infrastructure and vendor management capabilities.

- Pepcart is expected to support:

- Warehousing

- Logistics integration

- Fulfilment scalability

- Large-format commerce operations

- MyFlopy.com launch expanded the company into indigenous digital data storage solutions.

- MyFlopy.com aligns with the Government’s Atmanirbhar Bharat initiative.

- The company continued investments in:

- AI-driven property intelligence platforms

- Data infrastructure businesses

- Marketplace-led digital commerce

- TCC expanded its presence across:

- PropTech

- AI-driven solutions

- Infrastructure technology

- Consumer ecosystems

- Management emphasized a focus on scalable, high-margin recurring revenue streams.

Note:

- The company stated that platform integration and expansion into emerging technology-driven verticals remain central to its long-term growth strategy.

Risk Analysis

Summary:

- Despite strong growth momentum, TCC Concept remains exposed to execution risks associated with acquisitions, integration of multiple digital platforms, and sustainability of elevated margins amid rapid scaling.

Key Risks:

- EBITDA and PAT margins moderated during FY26 despite strong revenue growth.

- Integration risks remain around Pepperfry and Pepcart acquisitions.

- Expansion into multiple technology verticals may increase operational complexity.

- Scalability of platform-led businesses will depend on sustained customer adoption and ecosystem integration.

- High-growth digital commerce and AI segments remain highly competitive.

- Continued investments into infrastructure and technology platforms may impact short-term profitability.

- Revenue visibility may depend on successful monetization of recently acquired and launched platforms.

Worst Case Scenario:

- Failure to effectively integrate acquired businesses or scale platform monetization could pressure profitability and slow long-term growth momentum.

Risk Level: Medium

Company Commentary

- Management stated FY26 was a year of strong and resilient growth driven by operational efficiency and scalable platform expansion.

- The company highlighted that Pepperfry and Pepcart acquisitions significantly strengthened its consumer commerce and supply chain ecosystem.

- Management stated that TCC is building a unified ecosystem spanning infrastructure, intelligence, commerce, and digital fulfilment.

- The company emphasized increasing focus on high-margin recurring revenue streams across AI-led and marketplace-driven businesses.

- TCC stated it remains well positioned to capitalize on emerging opportunities across digital infrastructure, AI platforms, and consumer ecosystems.

- Management reiterated its commitment to innovation-led growth and long-term shareholder value creation.

Official Exchange Filing: TCC Concept Limited