Quarterly & Annual Financial Results

India Pesticides Crosses ₹1,000 Crore Revenue Milestone in FY26; PAT Jumps 45.8% YoY

NSE

ipl

BSE

543311

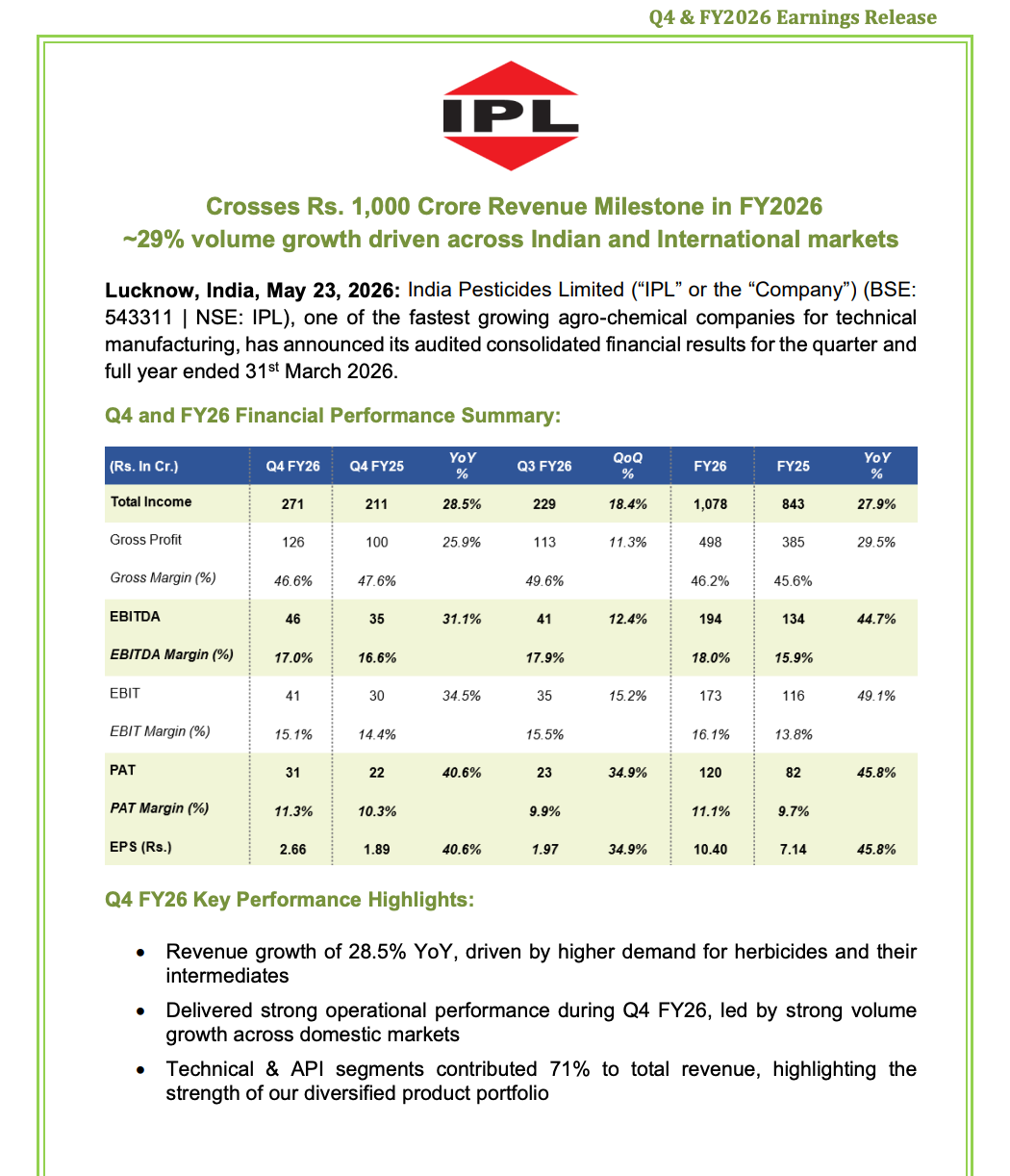

India Pesticides Limited reported strong audited FY26 consolidated performance with revenue crossing the ₹1,000 crore milestone for the first time. FY26 total income rose 27.9% YoY to ₹1,078 crore, while EBITDA and PAT increased 44.7% and 45.8% respectively, supported by strong domestic demand, higher capacity utilization, and improved operational efficiency.

PRICE-SENSITIVE TRIGGER

Event: FY26 Audited Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered robust growth across revenue, EBITDA, and profitability while improving margins and recording strong volume growth across domestic and international markets.

Key Metrics:

- FY26 Total Income:

- ₹1,078 crore

- Up 27.9% YoY from ₹843 crore

- FY26 EBITDA:

- ₹194 crore

- Up 44.7% YoY from ₹134 crore

- FY26 EBITDA Margin:

- 18.0%

- Vs 15.9% in FY25

- FY26 PAT:

- ₹120 crore

- Up 45.8% YoY from ₹82 crore

- FY26 PAT Margin:

- 11.1%

- Vs 9.7% in FY25

- FY26 EPS:

- ₹10.40

- Vs ₹7.14 in FY25

- Q4 FY26 Total Income:

- ₹271 crore

- Up 28.5% YoY

- Up 18.4% QoQ

- Q4 FY26 EBITDA:

- ₹46 crore

- Up 31.1% YoY

- Q4 FY26 EBITDA Margin:

- 17.0%

- Vs 16.6% in Q4 FY25

- Q4 FY26 PAT:

- ₹31 crore

- Up 40.6% YoY

- Q4 FY26 PAT Margin:

- 11.3%

- Vs 10.3% in Q4 FY25

- Volume Growth:

- Approximately 29% in FY26

- Technical & API Segment Contribution:

- 71% of total revenue

Highlight:

- India Pesticides crossed the ₹1,000 crore annual revenue milestone for the first time in FY26 while delivering strong profitability expansion.

What Happened ?

India Pesticides Limited announced audited consolidated financial results for Q4 and FY26, reporting strong operational and financial performance across key business segments.

The company benefited from:

- Higher demand for herbicides and intermediates

- Strong domestic market performance

- Improved capacity utilization

- Better operational efficiencies

- Consistent execution across key product categories

FY26 marked a major milestone as the company crossed ₹1,000 crore in annual revenue for the first time.

Management highlighted continued focus on:

- Process optimization

- Backward integration

- Product innovation

- Capacity expansion

- Manufacturing efficiency improvements

The company also continued to strengthen:

- R&D capabilities

- Project engineering

- International product registrations

- Development of new molecules and intermediates

Key Details

Operational and Strategic Highlights:

- FY26 volume growth stood at approximately 29%, reflecting strong execution and higher plant utilization.

- Strong demand for herbicides and intermediates supported revenue growth during Q4 FY26.

- Technical and API businesses contributed 71% of total revenue, highlighting portfolio diversification.

- EBITDA margin improved to 18.0% in FY26 from 15.9% in FY25.

- PAT margin improved to 11.1% from 9.7% in FY25.

- The company crossed the ₹1,000 crore annual revenue milestone for the first time.

- India Pesticides continued investments in:

- Backward integration

- Manufacturing optimization

- Product development

- Capacity enhancement

- R&D initiatives supported:

- Cost optimization

- Process innovation

- New molecule development

- International registrations

- The company maintained focus on expanding differentiated product offerings across domestic and export markets.

Note:

- Management indicated that strong customer relationships, operational discipline, and continued innovation remain key pillars for sustaining long-term growth momentum.

Risk Analysis

Summary:

- Despite strong earnings momentum, India Pesticides remains exposed to cyclical agrochemical industry risks including pricing pressure, demand volatility, and global supply-chain fluctuations.

Key Risks:

- Agrochemical markets remain vulnerable to pricing pressure and global demand fluctuations.

- Raw material and supply-chain volatility may affect margins.

- Export demand remains sensitive to global inventory cycles and regulatory changes.

- Margin sustainability may depend on continued operational efficiency and capacity utilization.

- Competitive pressure in technicals and APIs may impact pricing realization.

- Weather conditions and agricultural demand trends can influence product demand.

Worst Case Scenario:

- Sharp pricing corrections, lower agrochemical demand, or supply-chain disruptions could impact growth momentum and profitability in future quarters.

Risk Level: Medium

Company Commentary

- Management stated FY26 was marked by strong operational and financial performance despite a challenging agrochemical environment.

- The company highlighted that strong domestic demand, capacity utilization, and operational efficiency drove profitability growth.

- India Pesticides stated that crossing the ₹1,000 crore revenue milestone validates its execution capabilities and long-term strategy.

- Management reiterated focus on:

- Backward integration

- Capacity expansion

- Product innovation

- Manufacturing efficiency

- The company emphasized continued investments in R&D and differentiated product development.

- Management stated India Pesticides remains well positioned for sustainable long-term growth across Indian and international markets.

Official Exchange Filing: India Pesticides Limited