Quarterly & Annual Financial Results

Goodluck India Reports Strong EBITDA Growth in Q4 FY26; Defence, Solar and Infrastructure Expansion Drive Long-Term Outlook

NSE

goodluck

BSE

530655

Goodluck India Limited reported improved profitability and margin expansion in Q4 FY26 despite marginal quarterly revenue decline. The company strengthened its presence across defence, renewable energy, railways and infrastructure segments while maintaining strong operational efficiency and expanding value-added product contribution.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 audited financial results announcement.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered strong EBITDA, PBT and PAT growth along with margin expansion, supported by value-added products, operational efficiency and strategic diversification into defence and infrastructure-led sectors.

Key Metrics:

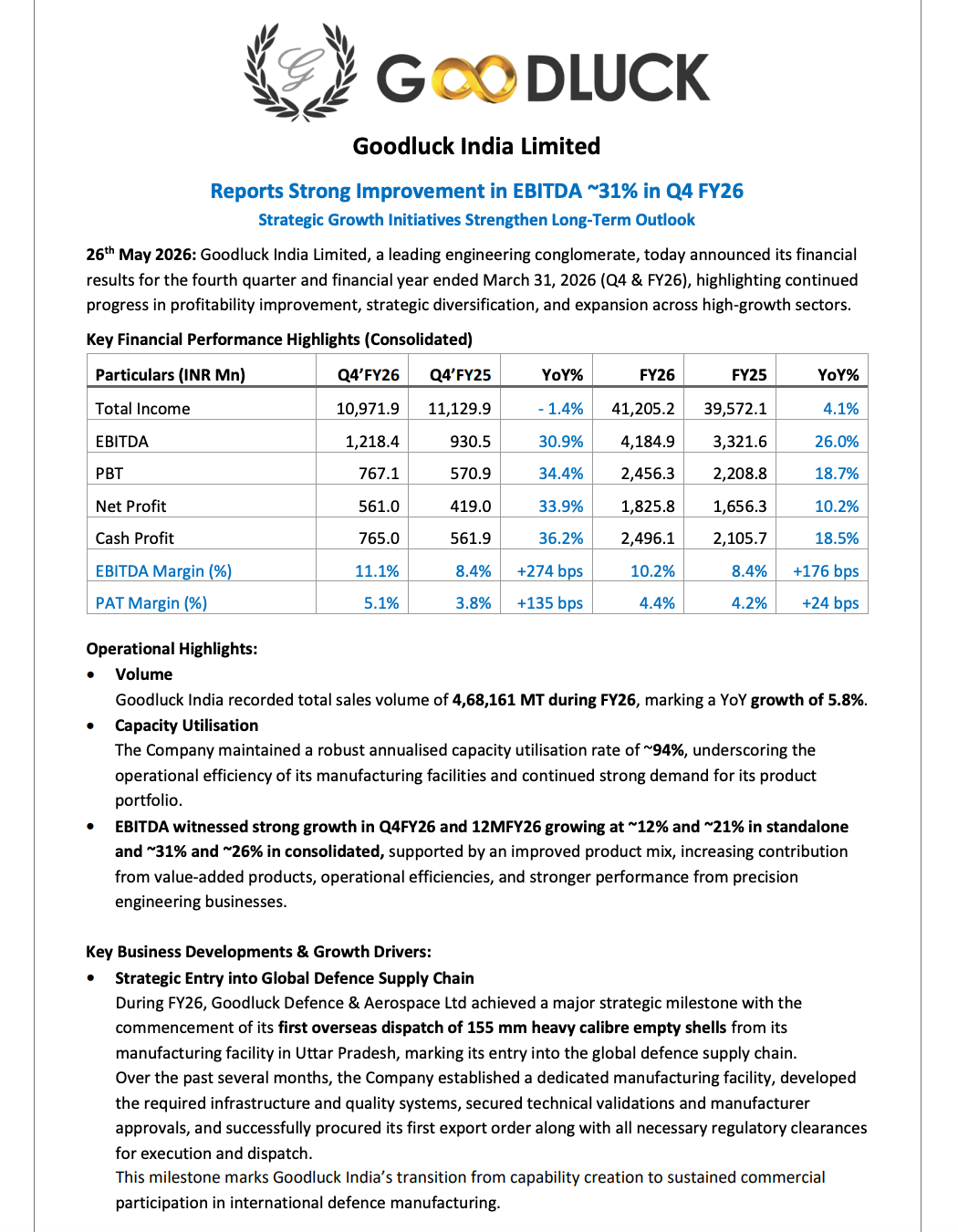

- Q4 FY26 Total Income: ₹10,971.9 million | YoY: -1.4%

- FY26 Total Income: ₹41,205.2 million | YoY: +4.1%

- Q4 FY26 EBITDA: ₹1,218.4 million | YoY: +30.9%

- FY26 EBITDA: ₹4,184.9 million | YoY: +26.0%

- Q4 FY26 PBT: ₹767.1 million | YoY: +34.4%

- FY26 PBT: ₹2,456.3 million | YoY: +18.7%

- Q4 FY26 Net Profit: ₹561.0 million | YoY: +33.9%

- FY26 Net Profit: ₹1,825.8 million | YoY: +10.2%

- Q4 FY26 EBITDA Margin: 11.1% | Expansion: +274 bps

- FY26 EBITDA Margin: 10.2% | Expansion: +176 bps

- Q4 FY26 PAT Margin: 5.1% | Expansion: +135 bps

- FY26 PAT Margin: 4.4% | Expansion: +24 bps

- FY26 Sales Volume: 4,68,161 MT | YoY Growth: 5.8%

- Capacity Utilisation: ~94% annualised

Highlight:

- Highlight Label: Profitability Improvement

- Highlight Value: Q4 FY26 EBITDA grew 30.9% YoY with EBITDA margin expanding 274 bps, reflecting improved product mix and higher contribution from value-added businesses.

What Happened ?

Goodluck India Limited announced its Q4 FY26 and FY26 financial results, highlighting strong profitability growth, margin expansion and strategic diversification across defence, renewable energy, railways and infrastructure sectors.

While Q4 revenue remained broadly stable, profitability improved significantly due to higher contribution from value-added products, operational efficiencies and stronger performance from precision engineering businesses.

The company also reported major progress in its defence manufacturing business with commencement of overseas dispatches of 155 mm heavy calibre empty shells, marking entry into the global defence supply chain.

Key Details

Operational Performance & Strategic Expansion:

- EBITDA growth remained strong in both quarterly and annual periods:

- Standalone EBITDA growth:

- Q4 FY26: ~12%

- FY26: ~21%

- Consolidated EBITDA growth:

- Q4 FY26: ~31%

- FY26: ~26%

- Standalone EBITDA growth:

- Defence business achieved a strategic milestone with first overseas dispatch of 155 mm heavy calibre empty shells from Uttar Pradesh manufacturing facility.

- Goodluck Defence & Aerospace Ltd established dedicated manufacturing infrastructure and secured technical validations along with export approvals.

- Solar structure volume grew by approximately 33% in Q4 FY26 driven by renewable energy demand.

- Company secured export infrastructure orders in Nepal for galvanized steel tower structures and fasteners for a 400 kV double circuit transmission line project.

- Infrastructure and railways opportunity pipeline strengthened under:

- PM Gati Shakti

- Rail modernization projects

- Bullet train initiatives

- Manufacturing footprint includes:

- Six manufacturing plants across Uttar Pradesh and Gujarat

- Combined annual capacity of 500,000 MT

- ~57% capacity dedicated to high-margin value-added products

- Defence manufacturing subsidiary currently has:

- Capacity of 1,50,000 shells annually

- Expansion underway toward 400,000 shells per annum

- Company continues to see demand momentum in:

- Hydraulic tubes

- Engineering products

- Infrastructure steel products

- Renewable energy structures

Note:

- Management indicated continued focus on expanding engineering capabilities, improving profitability, strengthening exports and scaling higher-margin businesses linked to defence, railways, solar and infrastructure sectors.

Risk Analysis

Summary:

- Despite improving profitability and strategic diversification, the business remains exposed to infrastructure cycles, raw material volatility and execution risks associated with scaling defence and value-added manufacturing operations.

Key Risks:

- Revenue growth remained moderate despite strong profit expansion

- Steel price volatility can impact margins

- Defence business scale-up depends on sustained export orders and regulatory execution

- Infrastructure and railway demand remains dependent on government spending momentum

- Renewable energy and export businesses remain sensitive to geopolitical and policy changes

Worst Case Scenario:

- Weak infrastructure demand, lower export orders or commodity cost inflation could pressure margins and slow execution of high-growth vertical expansion plans.

Risk Level: Medium

Company Commentary

- Chairman Mahesh Chandra Garg stated FY26 marked an important year for strengthening strategic positioning across high-growth sectors while significantly improving profitability and operational efficiency.

- Management attributed margin expansion to:

- Value-added product strategy

- Disciplined execution

- Focus on higher-margin businesses

- Company highlighted strong long-term opportunities from:

- Defence indigenization

- Renewable energy investments

- Railways modernization

- Infrastructure expansion

- Management reiterated focus on:

- Enhancing product value

- Expanding engineering capabilities

- Driving profitable growth

- Strengthening export presence

- Company remains focused on scaling defence and engineering businesses while improving operational efficiencies and long-term sustainability.

Official Exchange Filing: Goodluck India Limited