Quarterly & Annual Financial Results

Grasim Industries Reports Record FY26 Revenue of ₹1.75 Lakh Crore; EBITDA Surges 29% YoY

NSE

grasim

BSE

500300

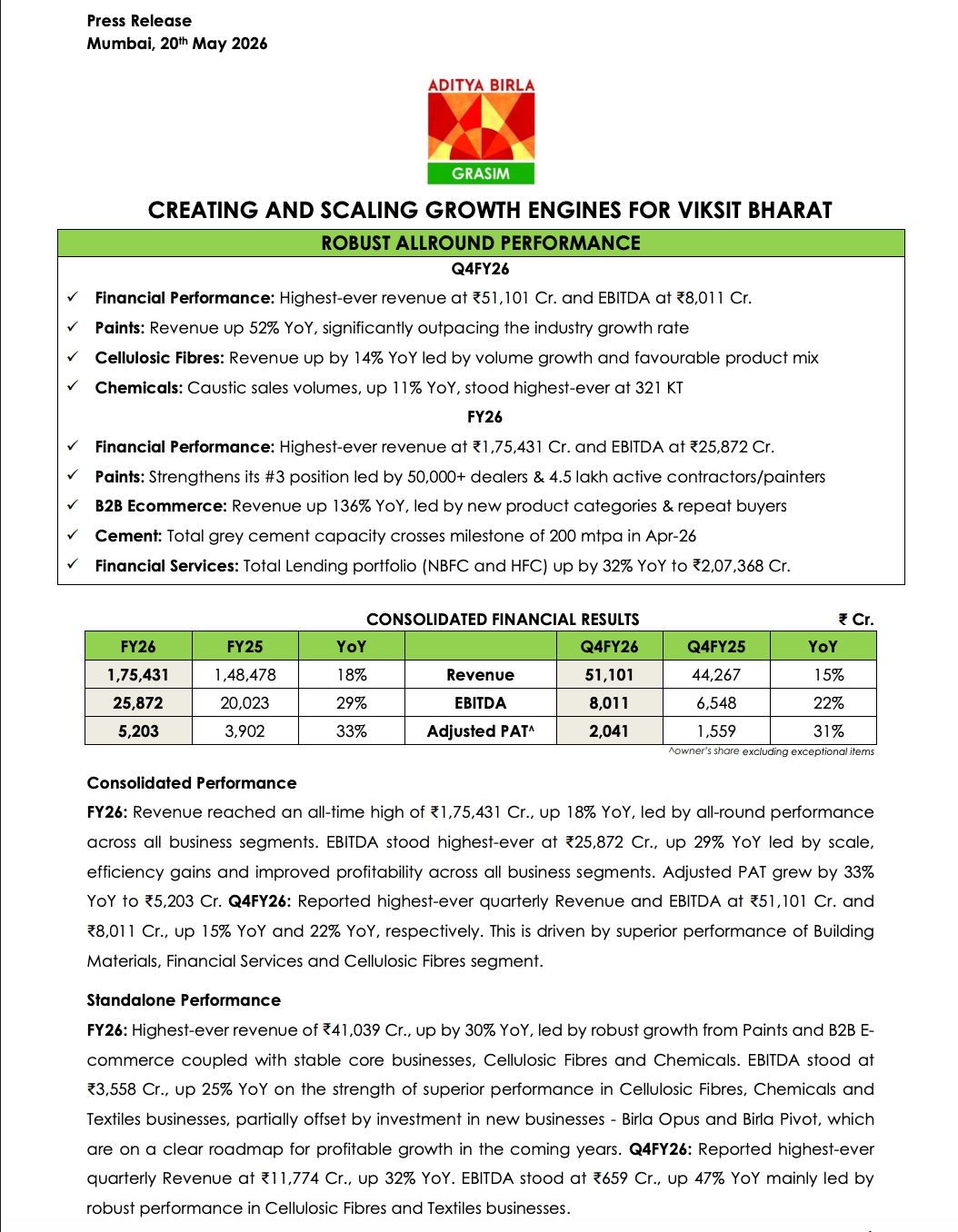

Grasim Industries reported its highest-ever consolidated revenue and EBITDA for FY26, supported by strong performance across building materials, paints, financial services, cellulosic fibres, and chemicals businesses. Revenue rose 18% YoY to ₹1,75,431 crore while adjusted PAT increased 33% YoY to ₹5,203 crore.

PRICE-SENSITIVE TRIGGER

Event: Audited Financial Results Announcement for Q4 and FY26

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company reported record revenue, EBITDA and PAT growth with strong expansion across paints, cement, B2B ecommerce and financial services businesses.

Key Metrics:

Consolidated FY26 Performance:

- Revenue: ₹1,75,431 crore (+18% YoY)

- EBITDA: ₹25,872 crore (+29% YoY)

- Adjusted PAT: ₹5,203 crore (+33% YoY)

Consolidated Q4FY26 Performance:

- Revenue: ₹51,101 crore (+15% YoY)

- EBITDA: ₹8,011 crore (+22% YoY)

- Adjusted PAT: ₹2,041 crore (+31% YoY)

Standalone FY26 Performance:

- Revenue: ₹41,039 crore (+30% YoY)

- EBITDA: ₹3,558 crore (+25% YoY)

Standalone Q4FY26 Performance:

- Revenue: ₹11,774 crore (+32% YoY)

- EBITDA: ₹659 crore (+47% YoY)

Key Business Highlights:

- Paints Revenue Growth: +52% YoY in Q4FY26

- B2B Ecommerce Revenue Growth: +136% YoY in FY26

- Financial Services Lending Portfolio: ₹2,07,368 crore (+32% YoY)

- Cement Capacity: Crossed 200 mtpa milestone

- Dividend Recommended: ₹10 per equity share

Highlight Metric:

- Grasim Industries achieved its highest-ever consolidated revenue of ₹1.75 lakh crore and EBITDA of ₹25,872 crore in FY26.

What Happened ?

Grasim Industries announced record FY26 and Q4FY26 financial performance driven by strong execution across all major business verticals.

The company highlighted strong momentum in the paints business under Birla Opus, rapid scaling of B2B ecommerce platform Birla Pivot, steady growth in financial services, and record cement capacity expansion through UltraTech Cement.

Management stated that all-round operational improvements, scale efficiencies, and business diversification supported the strong profitability growth during the year.

Key Details

Building Materials Business:

- Building materials segment delivered highest-ever quarterly revenue of ₹30,042 crore.

- UltraTech Cement crossed 200 mtpa global cement capacity milestone.

- Cement EBITDA improved due to operational efficiencies and scale benefits.

- Green power mix in cement business reached 43%.

Paints Business (Birla Opus):

- Paints revenue grew 52% YoY in Q4FY26.

- Birla Opus strengthened its position as the #3 player in organised decorative paints.

- Dealer network crossed 50,000 dealers across 11,500+ towns.

- Brand awareness crossed 90%.

B2B Ecommerce (Birla Pivot):

- Revenue more than doubled YoY in Q4FY26.

- Platform now offers 50,000+ SKUs across 1,000+ brands.

- Growth driven by repeat buyers and category expansion.

Financial Services:

- Lending portfolio rose 32% YoY to ₹2,07,368 crore.

- Total AUM reached ₹5,91,343 crore.

- ABCD digital platform crossed 11 million customers.

Cellulosic Fibres & Chemicals:

- Cellulosic fibres revenue grew 14% YoY.

- Chemicals business revenue rose 7% YoY.

- Caustic soda sales volumes reached record 321 KT.

Suitability & Expansion:

- Renewable power capacity share improved to 24%.

- Recycled water usage improved to 51%.

- Lyocell expansion project at Harihar progressing as planned.

Note:

- The company stated that its diversified business portfolio and strategic investments position it strongly for India’s long-term growth opportunity under the “Viksit Bharat” initiative.

Risk Analysis

Key Risks:

- Volatility in raw material and chemical prices.

- Competitive pricing pressure in decorative paints industry.

- Large investments in new businesses may temporarily impact margins.

- Global economic slowdown may affect demand across segments.

- Currency fluctuations can impact exports and imported inputs.

Worst Case Scenario:

- Sharp slowdown in construction, infrastructure or consumption demand could impact revenue growth and profitability across core business verticals.

Risk Level: Medium

Company Commentary

- Management stated FY26 reflected strong all-round business execution.

- Birla Opus continues gaining market share rapidly.

- UltraTech Cement remains on track to reach 240+ mtpa capacity by FY28.

- Grasim remains committed to long-term investments and sustainable growth.

- The company expects India’s infrastructure and consumption growth to support future expansion.

Official Exchange Filing: Grasim Industries Limited