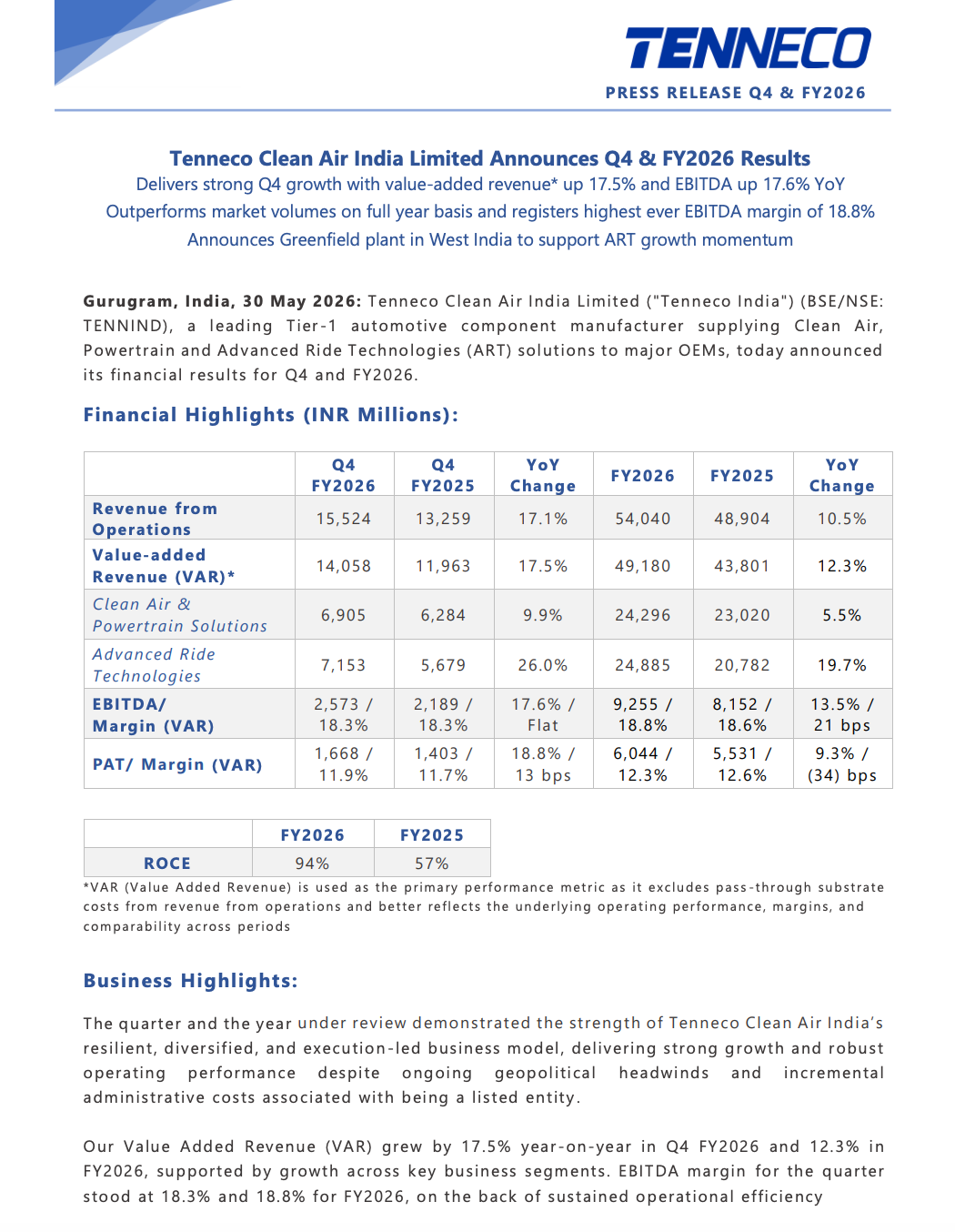

Quarterly & Annual Financial Results

Tenneco Clean Air India Delivers Record EBITDA Margin in FY26; Expands Order Book and Announces New Manufacturing Investments

NSE

TENNIND

BSE

544612

Tenneco Clean Air India Limited reported strong FY26 performance with double-digit growth across revenue, value-added revenue, EBITDA and PAT. The company achieved its highest-ever EBITDA margin of 18.8%, strengthened its lifetime order book to ₹12,400 crore, expanded into new OEM platforms, and announced fresh manufacturing investments in North and West India to support future growth.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong revenue growth, margin expansion, a record order book and additional capacity investments improve long-term growth visibility and support future earnings expansion.

Key Metrics:

- Q4 FY26 Revenue from Operations: ₹1,552.4 Cr | +17.1% YoY

- Q4 FY26 Value Added Revenue (VAR): ₹1,405.8 Cr | +17.5% YoY

- Q4 FY26 EBITDA: ₹257.3 Cr | +17.6% YoY

- Q4 FY26 EBITDA Margin: 18.3% | Flat YoY

- Q4 FY26 PAT: ₹166.8 Cr | +18.8% YoY

- Q4 FY26 PAT Margin: 11.9%

- FY26 Revenue from Operations: ₹5,404 Cr | +10.5% YoY

- FY26 Value Added Revenue (VAR): ₹4,918 Cr | +12.3% YoY

- FY26 EBITDA: ₹925.5 Cr | +13.5% YoY

- FY26 EBITDA Margin: 18.8% | Highest Ever | +21 bps

- FY26 PAT: ₹604.4 Cr | +9.3% YoY

- FY26 PAT Margin: 12.3%

- FY26 ROCE: 94% vs 57% in FY25

Highlight:

- FY26 EBITDA margin expanded to a record 18.8%, while the lifetime order book reached ₹12,400 crore, providing visibility covering more than 100% of FY28 revenue targets.

What Happened ?

Tenneco Clean Air India reported strong operational and financial performance for FY26 despite geopolitical disruptions and higher compliance costs associated with becoming a listed company.

Growth was driven by continued expansion in both Clean Air & Powertrain Solutions and Advanced Ride Technologies segments. The company secured multiple strategic program wins with Indian, Japanese and European OEMs, expanded into new product categories, strengthened its technology leadership and significantly increased its order book.

Management also announced new manufacturing investments in North and West India to support rising demand and future growth opportunities across emission control systems, suspension technologies and advanced automotive components.

Key Details

Strategic Growth Drivers and Business Developments:

- Lifetime order book reached ₹12,400 crore as of March 31, 2026.

- Current order book provides revenue visibility covering more than 100% of FY28 revenue targets.

- Won DCx DaVinci advanced suspension platform for a leading Indian OEM’s flagship SUV.

- Secured Clean Air System program from a leading Japanese passenger vehicle OEM.

- Won Clean Air after-treatment program from a leading European commercial vehicle OEM.

- Entered the bearings business through a leading Japanese passenger vehicle OEM.

- Completed strategic Proof of Concept for Euro VII-compliant Clean Air solutions with a leading European truck OEM.

- Received Toyota’s Zero-Defect Supplier Award in the Advanced Ride Technologies business.

- H2 FY26 order additions stood at ₹6,025.4 crore.

- Announced new greenfield Clean Air manufacturing facility in North India.

- Announced another greenfield plant for Advanced Ride Technologies in West India.

- Combined planned manufacturing investments total approximately ₹140 crore (₹1,400 million).

- Operates 12 manufacturing facilities and two R&D centers across India.

Note:

- Management expects the expanding order pipeline, technology-led product wins and manufacturing investments to support a healthy double-digit growth trajectory over the next several years.

Risk Analysis

Summary:

- While business momentum remains strong, future growth depends on OEM production volumes, successful execution of capacity expansion projects and broader automotive industry demand.

Key Risks:

- Automotive demand cycles directly impact component volumes.

- OEM production schedules and platform launches influence revenue realization.

- Expansion projects must be commissioned on time to support growth plans.

- Geopolitical developments can impact supply chains and operating costs.

- Increasing competition within emission-control and suspension technologies may affect future pricing.

- Revenue concentration in automotive OEM customers remains a sector-specific risk.

Worst Case Scenario:

- A slowdown in vehicle production, delays in OEM platform launches, weaker automotive demand or project execution delays could affect order conversion, revenue growth and profitability.

Risk Level: Medium

Company Commentary

- Management stated FY26 demonstrated the strength of Tenneco India’s diversified and execution-focused business model.

- The company delivered its highest-ever EBITDA margin despite geopolitical and cost pressures.

- Leadership highlighted confidence in scaling manufacturing capabilities to meet growing customer demand.

- New investments in North and West India are expected to support future growth and customer partnerships.

- Management emphasized strong opportunities in advanced emission technologies and ride-performance systems.

- The company believes its expanding order book and strategic wins position it for long-term value creation.

- Tenneco expects sustained double-digit growth supported by strong revenue visibility and increasing market opportunities.

Official Exchange Filing: Tenneco Clean Air India Limited