Quarter Ended: March 2026

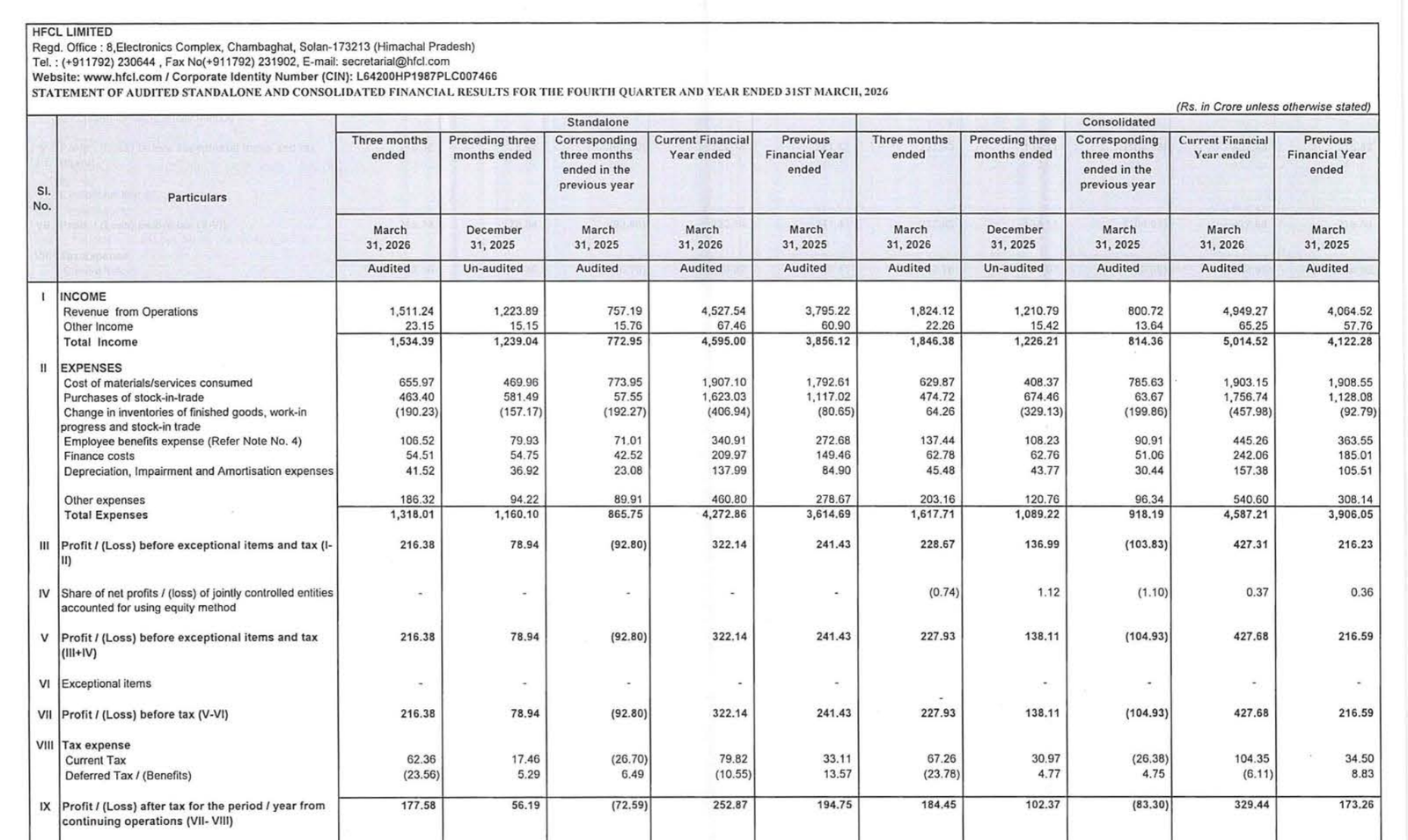

HFCL Limited – Q4 FY26 Financial Results

NSE

hfcl

BSE

500183

HFCL delivered strong revenue and profit growth, but significant working capital stress led to negative operating cash flow — a key red flag

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,511.24 Cr

- QoQ Change: +23.1%

- YoY Change: +99.6%

- Previous Quarter (Q3 FY26): ₹1,223.89 Cr

- Previous Year (Q4 FY25): ₹757.19 Cr

- Revenue (Q4 FY26): ₹1,511.24 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹177.58 Cr

- QoQ Change: +216%

- YoY Change: Turnaround

- Previous Quarter (Q3 FY26): ₹56.19 Cr

- Previous Year (Q4 FY25): – ₹72.59 Cr Loss

- PAT (Q4 FY26): ₹177.58 Cr

- QoQ Performance:

- Revenue Trend: Strong growth

- Profit Trend: Sharp improvement

Margin Analysis

Key Drivers:

- Strong revenue scaling

- Better absorption of fixed costs

- Improved segment profitability (Telecom & Defence)

- Stable finance cost relative to revenue growth

Key Signal: Margins are improving, but sustainability depends on working capital control

Segment performance

Segment: Telecom Products

- Revenue: ₹901.12 Cr

- Insights:

- Core growth driver

- Strong margin expansion

- High demand from telecom infra

Segment: Turnkey Contracts & Services

- Revenue: ₹609.93 Cr

- Insights:

- Stable execution business

- Lower margin vs product segment

Segment: Defence Products & Services

- Revenue: ₹0.19 Cr

- Insights:

- Early stage but strategic segment

- Future growth optionality

Segment insight

Summary:

HFCL operates across telecom equipment, turnkey projects, and emerging defence manufacturing

Characteristics:

- Telecom-led growth model

- Increasing focus on defence manufacturing

- Execution-heavy business

- Working capital intensive

Earning quality check

Drivers:

- Net profit growth supported by revenue

- High receivables and inventory buildup

- Negative operating cash flow

Interpretation:

- Earnings quality is weak, as profits are not converting into cash

balance sheet Analysis

- Total Assets: ₹8,867.58 Cr

- Total Liabilities: ₹3,366.79 Cr (current liabilities only, broader ~₹3,900+ Cr including non-current)

Insight:

- Balance sheet expansion is driven by:

- Increase in receivables

- Inventory buildup

- Higher working capital requirement

key risks

- Negative operating cash flow

- High working capital cycle

- Dependency on telecom capex cycle

- Execution delays in turnkey projects

- Margin pressure from competitive bidding

management strategy signals

Focus Area:

- Expand telecom equipment manufacturing

- Scale defence business

- Increase order book execution

- Improve product mix

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹1,534.39 Crore | +23.8% | +98.7% |

| PBT | ₹216.38 Crore | +174.2% | Turnaround |

| PAT | ₹177.58 Crore | +216.0% | Turnaround |

HFCL is a growth story with execution strength, but:

Strong positives:

- Strong revenue growth

- Profit turnaround

- Segment expansion

Concerns:

- Negative operating cash flow

- Working capital stress

- Cash conversion risk

Official Exchange Filing: HFCL Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

87%

NET PROFIT AS % OF REVENUE

11.75%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED