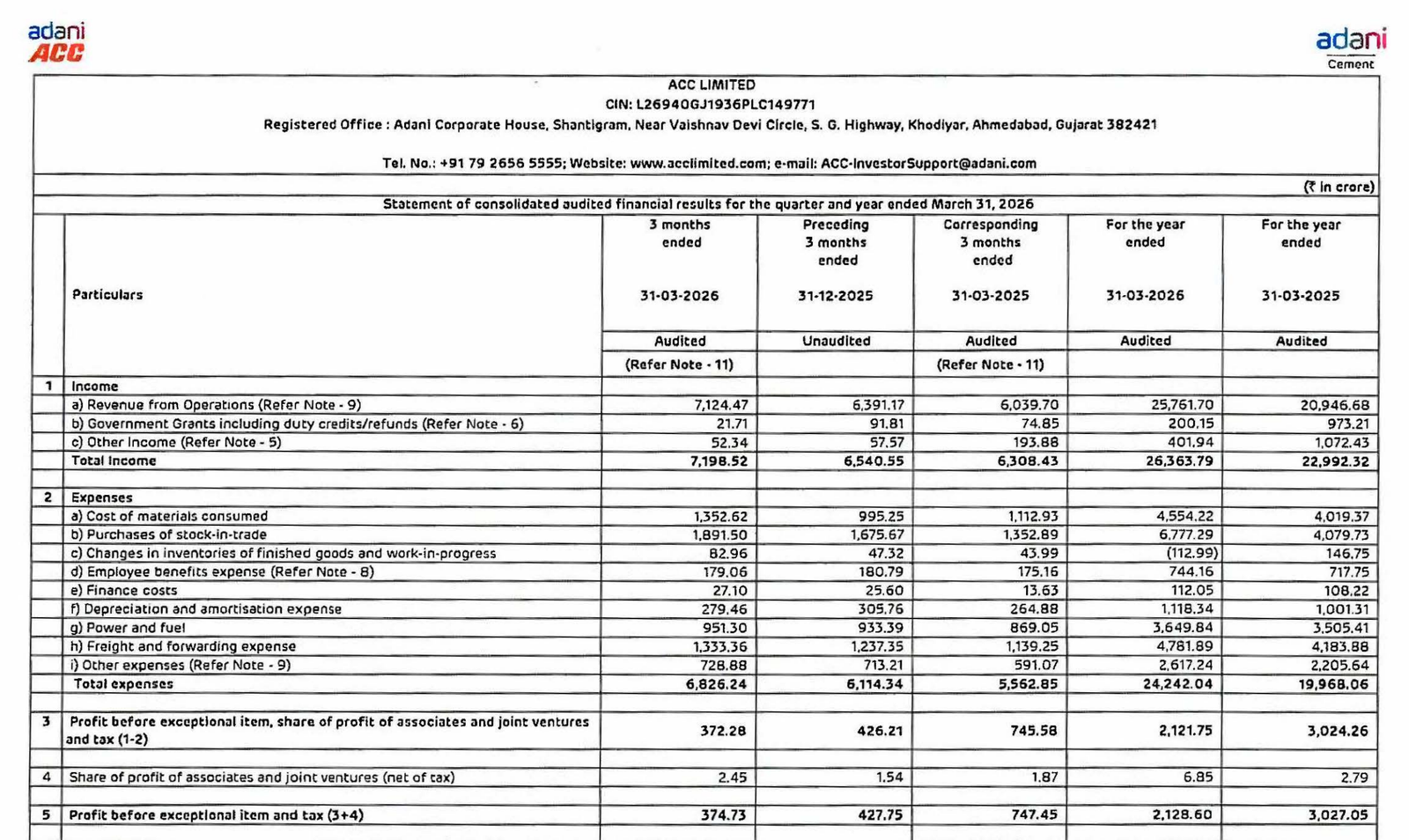

Quarter Ended: March 2026

ACC Ltd – Q4 FY26 Results

NSE

acc

BSE

500410

Despite strong topline growth, profitability declined due to cost pressures and lower operating efficiency

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹7,198.52 Cr

- QoQ Change: +10.06%

- YoY Change: +14.11%

- Previous Quarter (Q3 FY26): ₹6,540.55 Cr

- Previous Year (Q4 FY25): ₹6,308.43 Cr

- Revenue (Q4 FY26): ₹7,198.52 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹238.30 Cr

- QoQ Change: -40.05%

- YoY Change: -68.27%

- Previous Quarter (Q3 FY26): ₹404.25 Cr

- Previous Year (Q4 FY25): ₹751.04 Cr

- PAT (Q4 FY26): ₹238.30 Cr

- QoQ Performance

- Revenue Trend: Growth

- Profit Trend: Sharp Decline

Margin Analysis

Drivers:

- Significant increase in power & fuel costs

- Higher freight and logistics expenses

- Increase in raw material consumption cost

Insight:

- Operating margins compressed sharply → cost inflation impacting profitability

Segment performance

Segments:

- Cement & Ancillary Services

- Ready Mix Concrete

Performance Summary:

- Cement remains dominant contributor

- Ready Mix segment growing but still smaller in scale

- Segment profits declined due to cost pressures

Segment insight

Summary:

- ACC operates as a pure-play cement manufacturer, heavily dependent on infrastructure and construction demand.

Characteristics:

- Cyclical industry (linked to infra and real estate)

- High operating leverage

- Sensitive to fuel & logistics costs

Earning quality check

Drivers:

- Core operations under pressure

- No major dependence on other income

- Decline driven by operational inefficiencies, not accounting adjustments

Interpretations:

- Earnings quality is moderate, but current decline is structural cost-driven

balance sheet Analysis

- Total Assets: ₹27,525.26 Cr

- Total Liabilities: ₹6,970.77 Cr

Insight:

- Strong equity base (~₹20,554 Cr)

- Low leverage → financially stable

- Cash balance declined significantly

key risks

- Fuel cost volatility (coal, petcoke)

- Weak cement pricing environment

- High logistics cost exposure

- Cyclical infrastructure demand

management strategy signals

Focus Area:

- Cost optimization initiatives

- Capacity expansion

- Integration within Adani Group ecosystem

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹7,198.52 Cr | +10.06% | +14.11% |

| Total Expense | ₹370.36 Cr | -19.49% | -58.03% |

| Net Profit | ₹238.30 Cr | -41.05% | -68.27% |

ACC’s Q4 reflects a classic margin compression cycle — strong revenue but weak profitability. Until cost pressures ease, earnings recovery remains uncertain.

Official Exchange Filing: ACC Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

95%

NET PROFIT AS % OF REVENUE

3%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED