Quarter Ended: March 2026

Adani Green Energy Ltd (AGEL) – FY26 Results Deep Analysis

NSE

adanigreen

BSE

541450

Business is generating strong cash from operations, but aggressive capex and high leverage remain key structural concerns.

key financial highlights

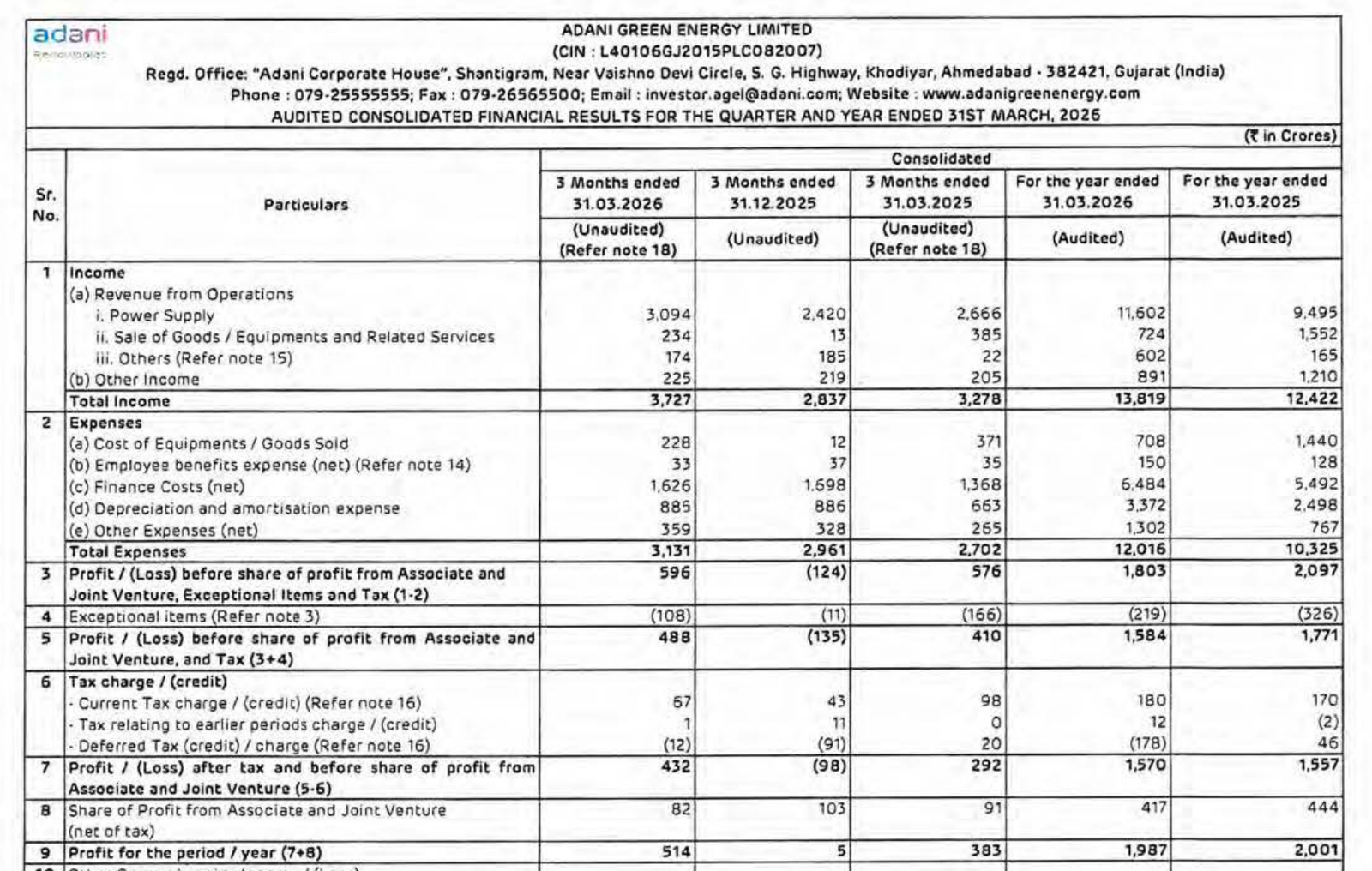

- Revenue (FY26): ₹13,819 Cr

- YoY Growth: +11.2% (vs ₹12,422 Cr)

- PAT (FY26): ₹1,987 Cr

- YoY Growth: Slight decline vs ₹2,001 Cr

- EBITDA Proxy Insight

- High depreciation + finance cost structure typical of infra/renewable model

Cash flow analysis

Operating Cash Flow (OCF): ₹10,135 Cr

- Strong and growing

- Indicates stable underlying power generation business

Investing Cash Flow: (₹26,227 Cr)

- Massive capex in:

- Solar/Wind assets

- Infrastructure expansion

Financing Cash Flow: ₹15,615 Cr

- Funded via:

- Debt (major contributor)

- Equity & instruments

Net Cash Movement

- Net cash decline despite strong OCF

- Reason: Capex >> Operating cash

Conclusion:

AGEL is in a hyper-growth infra phase

balance sheet Analysis

- Total Assets: ₹1,44,097 Cr

- Significant jump (expansion mode)

- Total Debt (approx):

- Non-current borrowings: ₹87,897 Cr

- Current borrowings: ₹10,476 Cr

Total Debt ~ ₹98,000+ Cr

- Equity: ₹29,879 Cr

- Debt-to-Equity ≈ 3.2x+ → HIGH LEVERAGE

Margin & cost structure

Key Cost Drivers:

- Finance Cost: ₹6,484 Cr

- Depreciation: ₹3,372 Cr

- These two alone eat a major portion of profits

Interpretation:

- Cash business strong

- Accounting profits suppressed due to infra nature

Earning quality check

Drivers:

- Cash flows strong (positive sign)

- Profit quality impacted by:

- High interest burden

- Depreciation

Interpretation:

- This is typical for renewable companies in expansion stage

key risks

- High Debt Load

- Rising interest cost risk

- Refinancing dependency

- Execution Risk

- Large-scale capex execution

- Regulatory Risk

- Power tariffs

- Government policies

- Cash Flow Timing Risk

- Delays in receivables from DISCOMs

Business Model Understanding

AGEL is:

- Asset-heavy renewable infra company

- Revenue = Long-term PPAs (stable)

- Growth = Continuous capex

Insights:

- High debt

- High depreciation

- Strong OCF but weak free cash flow

Strategic Interpretation

- Focus:

- Capacity addition

- Market dominance in renewables

- Not focused on near-term profitability

Final conclusion

- Suitable for long-term high-risk, high-growth investors

- Not suitable for conservative / low-risk profiles

Official Exchange Filing: Adani Green Energy Limited

FISCAL YEAR

2025-2026

AUDIT STATUS

AUDITED