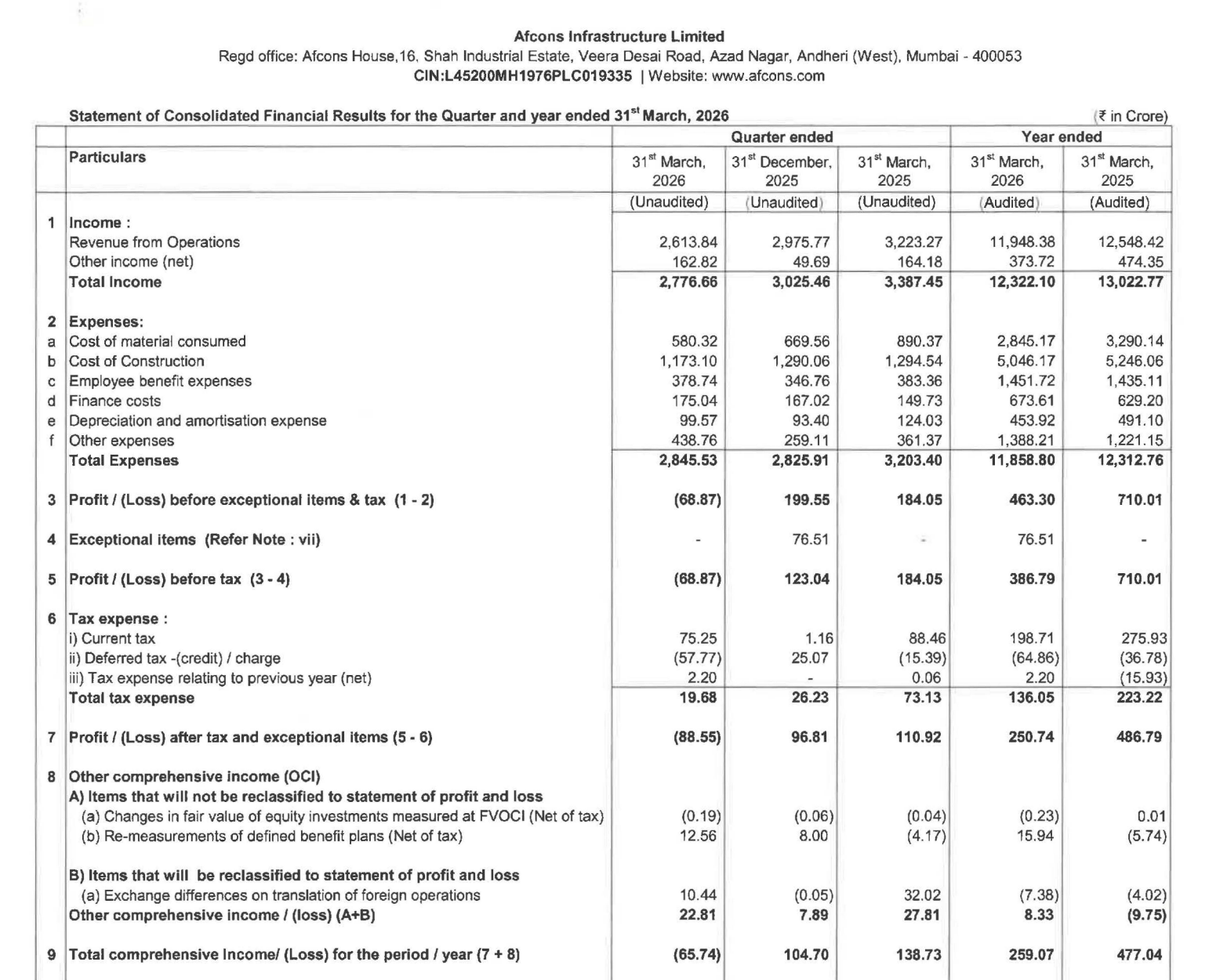

Quarter Ended: March 2026

Afcons Infrastructure Limited – Q4 FY26 Results

NSE

afcons

BSE

544280

Afcons Infrastructure reported weak Q4 FY26 earnings with revenue decline, quarterly loss, margin pressure, and weaker cash generation despite a stable balance sheet and higher borrowings.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹2,613.84 Crore

- QoQ Change: -12.16%

- YoY Change: -18.90%

- Previous Quarter (Q3 FY26): ₹2,975.77 Crore

- Previous Year (Q4 FY25): ₹3,223.27 Crore

- Revenue (Q4 FY26): ₹2,613.84 Crore

- Profit After Tax (PAT):

- PAT (Q4 FY26): -₹88.55 Crore Loss

- QoQ Change: -191.47%

- YoY Change: -179.83%

- Previous Quarter (Q3 FY26): ₹96.81 Crore

- Previous Year (Q4 FY25): ₹110.92 Crore

- PAT (Q4 FY26): -₹88.55 Crore Loss

- QoQ Performance:

- Revenue Trend: Sequential decline in execution and project activity impacted topline.

- Profit Trend: PAT turned negative from positive profitability in previous quarter.

- Revenue Trend: Sequential decline in execution and project activity impacted topline.

Margin Analysis

Drivers:

- Lower revenue absorption affected operating leverage.

- Construction costs remained elevated.

- Finance costs increased to ₹175.04 crore in Q4 FY26.

- Exceptional item benefit in previous quarter distorted sequential comparison.

- Lower project execution impacted profitability.

Insight:

- Margin profile weakened materially in Q4 FY26 as fixed costs and financing burden compressed earnings.

Segment insight

Business Summary:

The business continues to remain heavily dependent on infrastructure execution cycles, project mobilization, and working capital intensity.

Key Characteristics:

- EPC and infrastructure execution-driven business model.

- High working-capital dependence.

- Revenue visibility linked to order book execution pace.

- Margin volatility due to project mix and cost escalation.

Earning quality check

Key Drivers:

- Operating cash flow remained negative at ₹127.49 crore.

- Trade receivables increased sharply.

- Contract assets remained elevated.

- Finance costs stayed high at ₹673.61 crore annually.

- Borrowings increased significantly YoY.

Interpretations:

- Earnings quality remains under pressure due to weak operating cash generation and rising leverage despite large-scale project execution capability.

balance sheet Analysis

- Total Assets: ₹19,130.88 crore

- Total Liabilities: ₹13,680.30 crore

- Total Equity: ₹5,450.58 crore

Insight:

- The balance sheet expanded during FY26 driven by higher borrowings, receivables, and contract assets. Working capital intensity remains elevated.

key risks

- Declining revenue execution momentum.

- Rising debt and financing costs.

- Weak operating cash flow.

- High receivables and contract asset exposure.

- Margin pressure from infrastructure project execution.

- Dependence on government and large infrastructure spending cycles.

management strategy signals

Focus Area:

- Large infrastructure project execution.

- Working capital management.

- Order book monetization.

- Improving operating cash conversion.

- Managing leverage and finance costs.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹2776.66 Crore | -8.22% | -18.03% |

| PAT | ₹-88.55 Crore | -191.47% | -179.83% |

Afcons Infrastructure delivered a weak Q4 FY26 performance marked by revenue decline, quarterly losses, deteriorating margins, and negative operating cash flow. Although the company maintains a large infrastructure execution base and sizeable asset profile, rising borrowings, elevated working capital requirements, and profitability pressure remain key concerns. Recovery in execution pace and cash flow conversion will be critical going forward.

Official Exchange Filing: Afcons Infrastructure Limited

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED