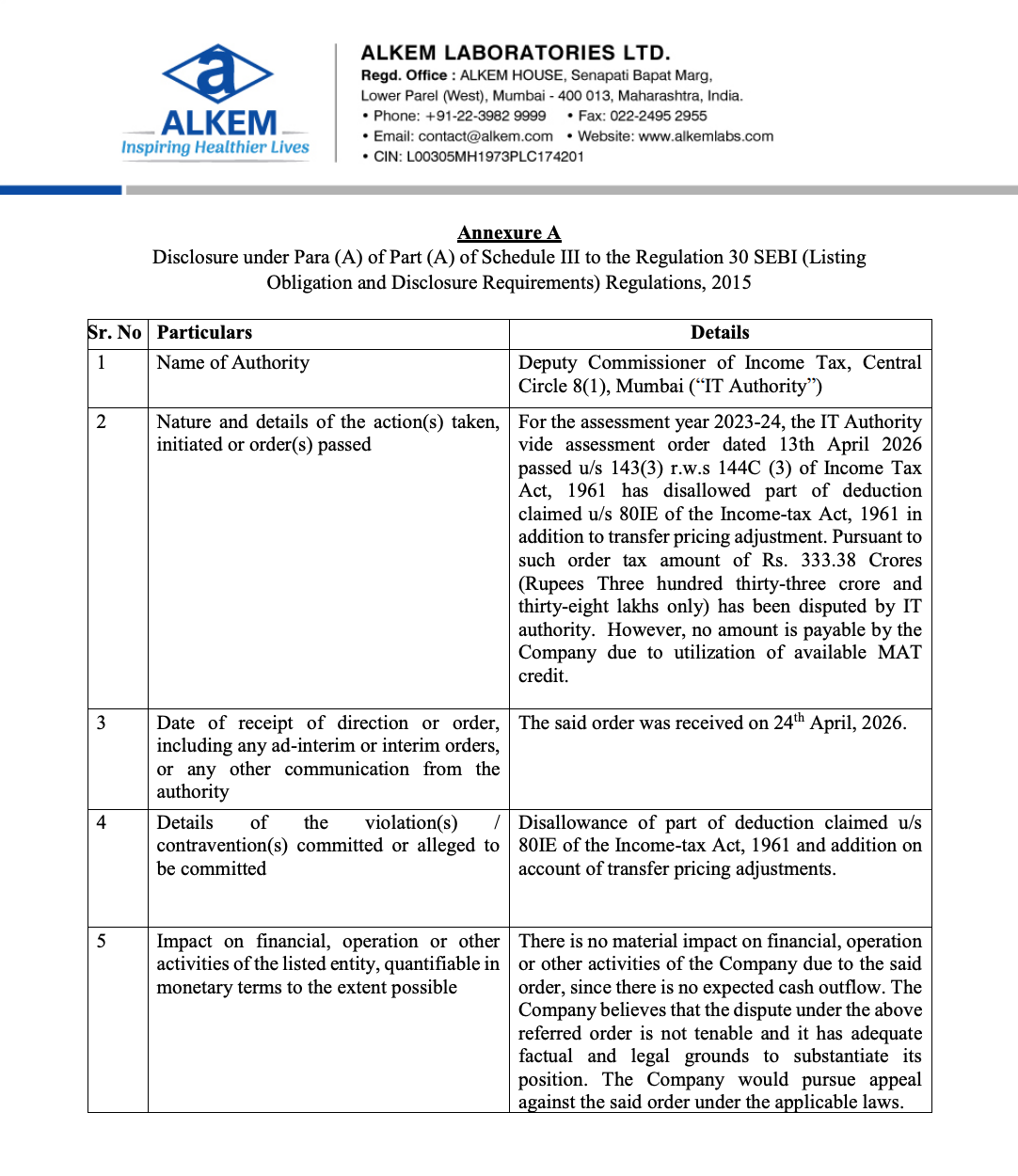

Regulatory / Tax Dispute

Alkem Labs receives ₹333 Cr tax order; no cash outflow expected, plans appeal

NSE

alkem

BSE

539523

Alkem Laboratories has received an Income Tax assessment order involving a disputed amount of ₹333.38 crore related to deduction disallowance and transfer pricing adjustments. However, the company clarified that there is no immediate cash outflow due to available MAT credit and plans to challenge the order.

PRICE-SENSITIVE TRIGGER

Event: Income Tax assessment order

Type: Regulatory / Tax Dispute

Impact: Neutral

Immediate Effect: No financial outflow; legal proceedings expected

Key Metrics:

- Disputed Tax Amount: ₹333.38 crore

- Assessment Year: FY23-24

- Cash Outflow: Nil (due to MAT credit)

Highlight:

- Large tax demand but no immediate financial impact

What Happened ?

The Income Tax Department issued an assessment order disallowing part of deductions under Section 80IE along with transfer pricing adjustments, leading to a tax demand. Alkem has disputed the order and will file an appeal.

key highlights

Authority:

- Deputy Commissioner of Income Tax

- Central Circle 8(1), Mumbai

Nature of Issue:

- Disallowance of:

- Deduction under Section 80IE

- Additional:

- Transfer pricing adjustments

Order Timeline:

- Order dated: April 13, 2026

- Received on: April 24, 2026

Financial Impact:

- Tax demand raised: ₹333.38 Cr

- However:

- No immediate payment required

- Covered via MAT credit

Company Stand:

- Order is:

- Not tenable

- Action:

- Will pursue legal appeal

Risk Analysis

Key Risks

- Litigation risk

- Potential future liability if appeal fails

- Regulatory scrutiny

Worst Case Scenario

- If the appeal is unsuccessful, the company may need to pay the tax along with possible interest/penalties

Risk Level: Medium

Company Commentary

- No material impact on operations

- No cash outflow expected

- Strong legal grounds to challenge order

Official Exchange Filing: Alkem Laboratories Limited