Quarterly & Annual Financial Results

Amara Raja Energy & Mobility reports 16% Q4 revenue growth; Board recommends ₹5.2 final dividend

NSE

are&M

BSE

500008

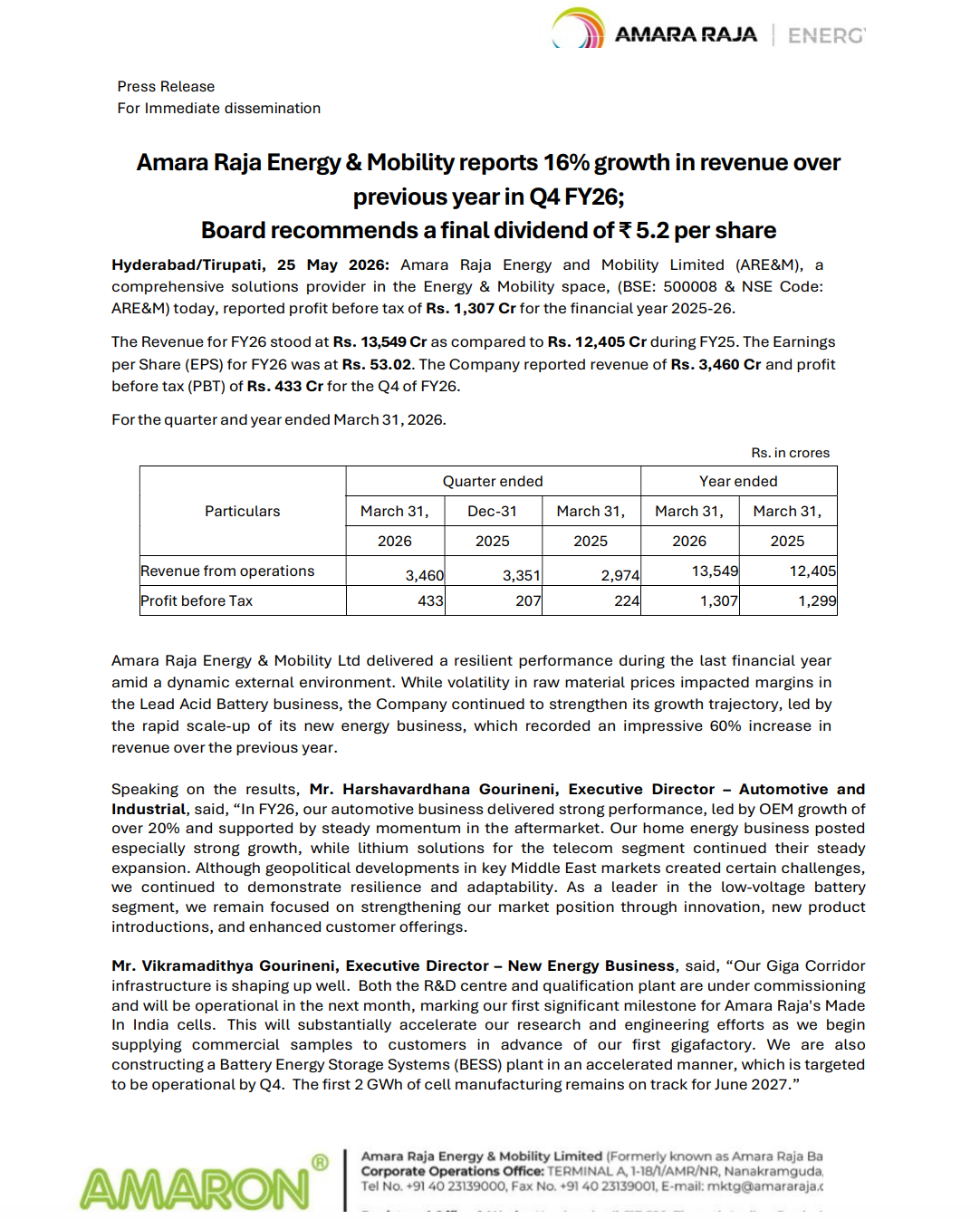

Amara Raja Energy & Mobility Limited reported FY26 revenue of ₹13,549 crore and profit before tax of ₹1,307 crore, supported by strong automotive battery demand, rapid growth in the new energy business, and expansion in lithium and energy storage initiatives. The Board recommended a final dividend of ₹5.2 per share.

PRICE-SENSITIVE TRIGGER

Event: Announcement of audited Q4 FY26 and FY26 financial results along with dividend recommendation.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered double-digit revenue growth, stable profitability, and strong traction in its new energy vertical while continuing execution of its lithium cell and battery storage expansion roadmap.

Key Metrics:

- FY26 Revenue: ₹13,549 crore vs ₹12,405 crore in FY25 (+9.2% YoY)

- FY26 Profit Before Tax (PBT): ₹1,307 crore vs ₹1,299 crore in FY25

- FY26 EPS: ₹53.02 per share

- Q4 FY26 Revenue: ₹3,460 crore vs ₹2,974 crore in Q4 FY25 (+16% YoY)

- Q4 FY26 PBT: ₹433 crore vs ₹224 crore in Q4 FY25

- New Energy Business Revenue Growth: ~60% YoY in FY26

- Final Dividend Recommended: ₹5.2 per share

Highlight:

- Label: Q4 Revenue Growth

- Value: Q4 FY26 revenue increased 16% YoY to ₹3,460 crore.

What Happened ?

Amara Raja Energy & Mobility Limited announced its audited financial results for Q4 FY26 and FY26, reporting continued growth across its automotive battery and new energy businesses.

The company recorded FY26 revenue of ₹13,549 crore alongside profit before tax of ₹1,307 crore. Quarterly revenue for Q4 FY26 stood at ₹3,460 crore, supported by strong OEM growth, aftermarket demand, and continued expansion in lithium-based energy solutions.

The Board also recommended a final dividend of ₹5.2 per share.

Management highlighted that the company’s new energy business delivered approximately 60% revenue growth during FY26 while major milestones in the lithium cell manufacturing ecosystem continue progressing.

Key Details

Operational & Strategic Business Developments:

- Automotive battery business delivered strong performance driven by over 20% OEM growth and sustained aftermarket momentum.

- Home energy business reported robust growth despite raw material volatility in the lead-acid segment.

- Lithium solutions business for telecom applications continued steady expansion.

- The company’s Giga Corridor infrastructure development is progressing as planned.

- R&D center and qualification plant are under commissioning and expected to become operational in the coming month.

- Commercial cell sample supplies are expected to begin ahead of commissioning of the first gigafactory.

- Battery Energy Storage Systems (BESS) manufacturing plant construction is progressing on an accelerated timeline.

- The first 2 GWh lithium cell manufacturing capacity remains on track for June 2027 commissioning.

- The company continued strategic diversification into next-generation chemistries, EV solutions, and energy storage technologies.

Note:

- Amara Raja continues transitioning from a traditional lead-acid battery company toward a broader energy storage and mobility platform with integrated lithium cell manufacturing ambitions.

Risk Analysis

Summary:

- The company continues to face raw material volatility, geopolitical uncertainties, and execution risks related to large-scale lithium and energy storage expansion projects.

Key Risks:

- Lead-acid battery margins remain exposed to fluctuations in commodity and raw material prices.

- Geopolitical developments in Middle East markets could impact export and supply chain conditions.

- Lithium cell manufacturing projects involve high capital expenditure and execution complexity.

- Commercialization timelines for gigafactory and BESS operations remain critical for future growth.

- Technology transitions in the energy storage industry could intensify competitive pressures.

- Scaling new energy businesses may temporarily impact return ratios and capital efficiency.

Worst Case Scenario:

- Delays in lithium manufacturing execution, weaker EV demand, or prolonged margin pressure in conventional battery operations could affect profitability and return on investments.

Risk Level: Medium

Company Commentary

- Executive Director Harshavardhana Gourineni stated that the automotive business delivered strong growth led by OEM momentum and aftermarket expansion.

- Management highlighted resilience in operations despite geopolitical developments and raw material volatility.

- Executive Director Vikramadithya Gourineni stated that the company’s Giga Corridor infrastructure, R&D center, and qualification plant are progressing well.

- The company confirmed that commercial cell samples will be supplied before commissioning of the first gigafactory.

- Chairman and Managing Director Jayadev Galla stated that Amara Raja is strengthening capabilities to emerge as India’s leading cell-to-grid energy player.

- Management reiterated focus on strategic diversification into new chemistries, energy storage systems, and mobility solutions.

Official Exchange Filing: Amara Raja Energy & Mobility Limited