Quarterly & Annual Financial Results

Astra Microwave Reports Strong FY26 Performance with Record Revenue, Margin Expansion and Robust Defence Order Book

NSE

astramicro

BSE

532493

Astra Microwave Products Limited reported strong Q4 FY26 and FY26 financial performance driven by healthy defence electronics demand, higher profitability and improved margins. The company achieved record annual revenue, expanded EBITDA margins significantly and maintained a strong consolidated order book of ₹2,610 crore while also approving an in-principle demerger of its Space, Meteorology and Hydrology business.

PRICE-SENSITIVE TRIGGER

Event: Announcement of Q4 FY26 and FY26 audited financial results.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered strong growth across revenue, EBITDA and PAT along with margin expansion and improved order visibility, strengthening its outlook in defence electronics, aerospace and space technology segments.

Key Metrics:

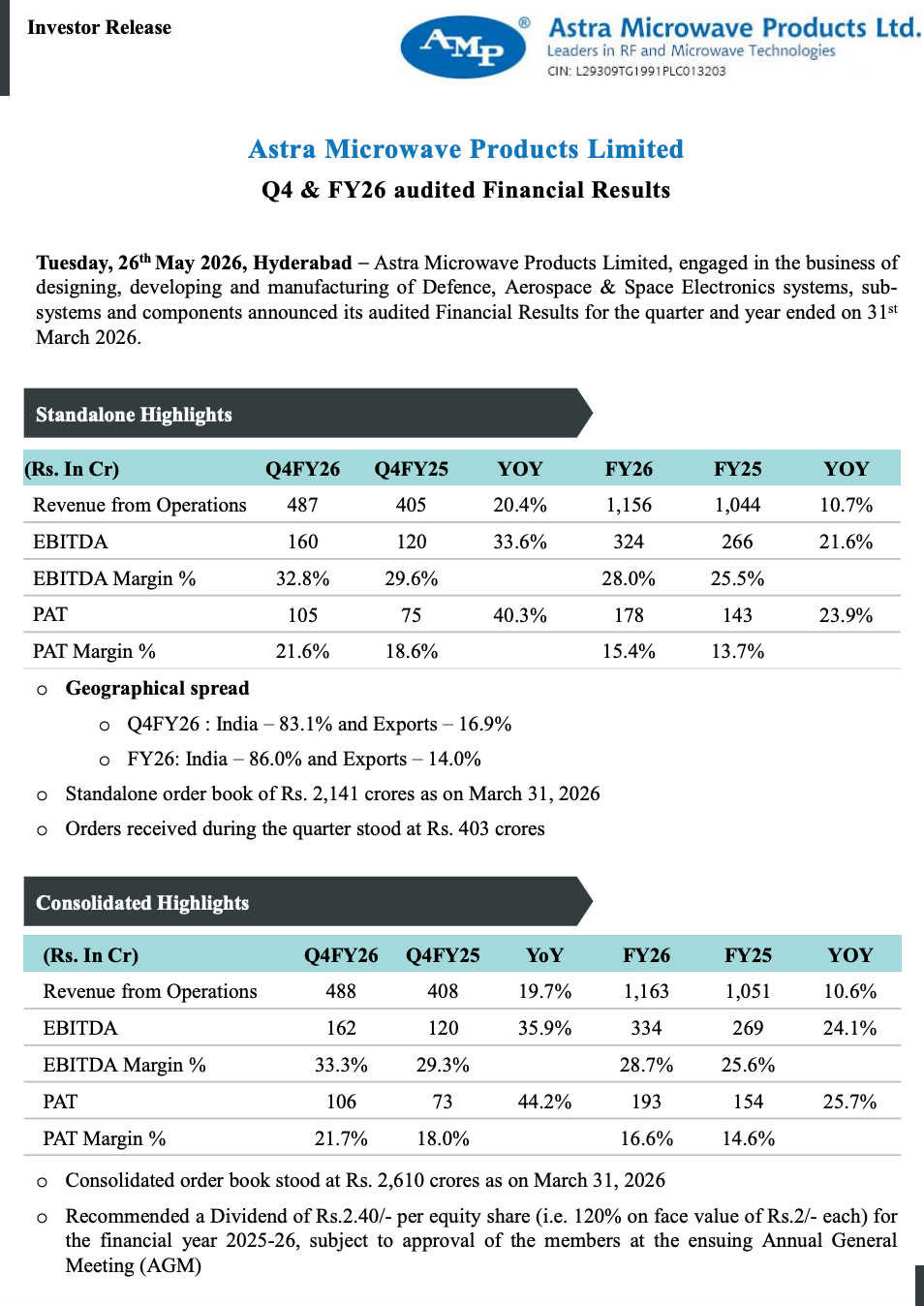

- Standalone Q4 FY26 Revenue: ₹487 crore | YoY Growth: 20.4%

- Standalone FY26 Revenue: ₹1,156 crore | YoY Growth: 10.7%

- Standalone Q4 FY26 EBITDA: ₹160 crore | YoY Growth: 33.6%

- Standalone FY26 EBITDA: ₹324 crore | YoY Growth: 21.6%

- Standalone Q4 FY26 EBITDA Margin: 32.8%

- Standalone FY26 EBITDA Margin: 28.0% | Expansion: +250 bps

- Standalone Q4 FY26 PAT: ₹105 crore | YoY Growth: 40.3%

- Standalone FY26 PAT: ₹178 crore | YoY Growth: 23.9%

- Standalone Q4 FY26 PAT Margin: 21.6%

- Standalone FY26 PAT Margin: 15.4%

- Consolidated Q4 FY26 Revenue: ₹488 crore | YoY Growth: 19.7%

- Consolidated FY26 Revenue: ₹1,163 crore | YoY Growth: 10.6%

- Consolidated Q4 FY26 EBITDA: ₹162 crore | YoY Growth: 35.9%

- Consolidated FY26 EBITDA: ₹334 crore | YoY Growth: 24.1%

- Consolidated FY26 EBITDA Margin: 28.7%

- Consolidated FY26 PAT: ₹193 crore | YoY Growth: 25.7%

- Standalone Order Book: ₹2,141 crore as of March 31, 2026

- Consolidated Order Book: ₹2,610 crore as of March 31, 2026

- Orders Received During Q4 FY26: ₹403 crore

- Recommended Dividend: ₹2.40 per equity share (120% on face value of ₹2)

Highlight:

- Highlight Label: Margin Expansion & Order Visibility

- Highlight Value: FY26 EBITDA margin expanded to 28.7% on a consolidated basis while consolidated order book stood at ₹2,610 crore, providing strong medium-term visibility.

What Happened ?

Astra Microwave Products Limited announced its audited Q4 FY26 and FY26 financial results, reporting record annual revenue, strong profitability growth and substantial margin expansion.

The company benefited from strong execution across defence, aerospace and space electronics programs along with improved revenue mix and operational efficiencies.

Management also announced that the Board has in-principle approved the demerger of the Space, Meteorology and Hydrology business to create sharper strategic focus and improve operational efficiency.

The company reiterated confidence in achieving 10%–15% topline growth in FY27 supported by robust domestic and international defence opportunities.

Key Details

Operational Performance & Strategic Developments:

- FY26 marked the company’s highest-ever annual revenue performance.

- EBITDA margins expanded significantly due to:

- Improved revenue mix

- Better operational efficiencies

- Higher-margin execution profile

- Geographical revenue mix:

- Q4 FY26:

- India: 83.1%

- Exports: 16.9%

- FY26:

- India: 86.0%

- Exports: 14.0%

- Q4 FY26:

- Consolidated order book stood at ₹2,610 crore including service orders of ₹231 crore.

- Orders received during Q4 FY26 totaled ₹403 crore.

- Company reaffirmed FY27 revenue growth guidance of 10%–15%.

- Board approved in-principle demerger of:

- Space business

- Meteorology business

- Hydrology business

- Proposed restructuring aims to:

- Improve strategic focus

- Enable segment-specific growth

- Simplify corporate structure

- Enhance governance and accountability

- Improve capital allocation efficiency

- Astra Microwave continues to benefit from:

- Rising defence electronics opportunities

- Growth in EW systems

- Aerospace and space electronics demand

- Domestic defence indigenization

- Company operates:

- 3 automatic PCB assembly lines

- 7 Class 10K cleanrooms

- 1 Class 100K cleanroom

- Product portfolio spans:

- Defence electronics

- RF & microwave systems

- Aerospace electronics

- Space systems

- Sub-systems and components

Note:

- Management indicated that the proposed demerger structure is expected to improve operational efficiency and unlock long-term growth opportunities across emerging defence and space electronics verticals.

Risk Analysis

Summary:

- Despite strong order visibility and profitability growth, Astra Microwave remains exposed to defence procurement cycles, execution timelines and technology-driven business risks.

Key Risks:

- Defence and aerospace revenue remains dependent on government procurement cycles.

- Export opportunities may be affected by geopolitical developments.

- Execution delays in strategic defence programs can impact revenue timing.

- High-technology manufacturing businesses require continuous R&D investments.

- Demerger execution may involve regulatory, operational and restructuring complexities.

Worst Case Scenario:

- Delays in defence order execution, lower government spending or slower conversion of strategic programs could impact growth momentum and margin sustainability.

Risk Level: Medium

Company Commentary

- Managing Director S G Reddy stated FY26 was another strong year with record revenue and improved profitability.

- Management highlighted:

- EBITDA margin expansion

- Strong Q4 performance

- Improved PAT margins

- Robust domestic and export opportunities

- Company reaffirmed FY27 topline growth guidance of 10%–15%.

- Management stated the proposed demerger aims to:

- Create sharper strategic focus

- Improve governance

- Enable dedicated management teams

- Improve operational efficiencies

- Company believes India’s defence electronics sector presents multi-dimensional long-term growth opportunities across EW and space businesses.

Official Exchange Filing: Astra Microwave Products Limited