Quarterly & Annual Financial Results

Belrise Industries Reports Strong FY26 Performance; Adjusted PAT Rises 41.2% YoY Amid Aerospace Expansion and OEM Order Wins

NSE

belrise

BSE

544405

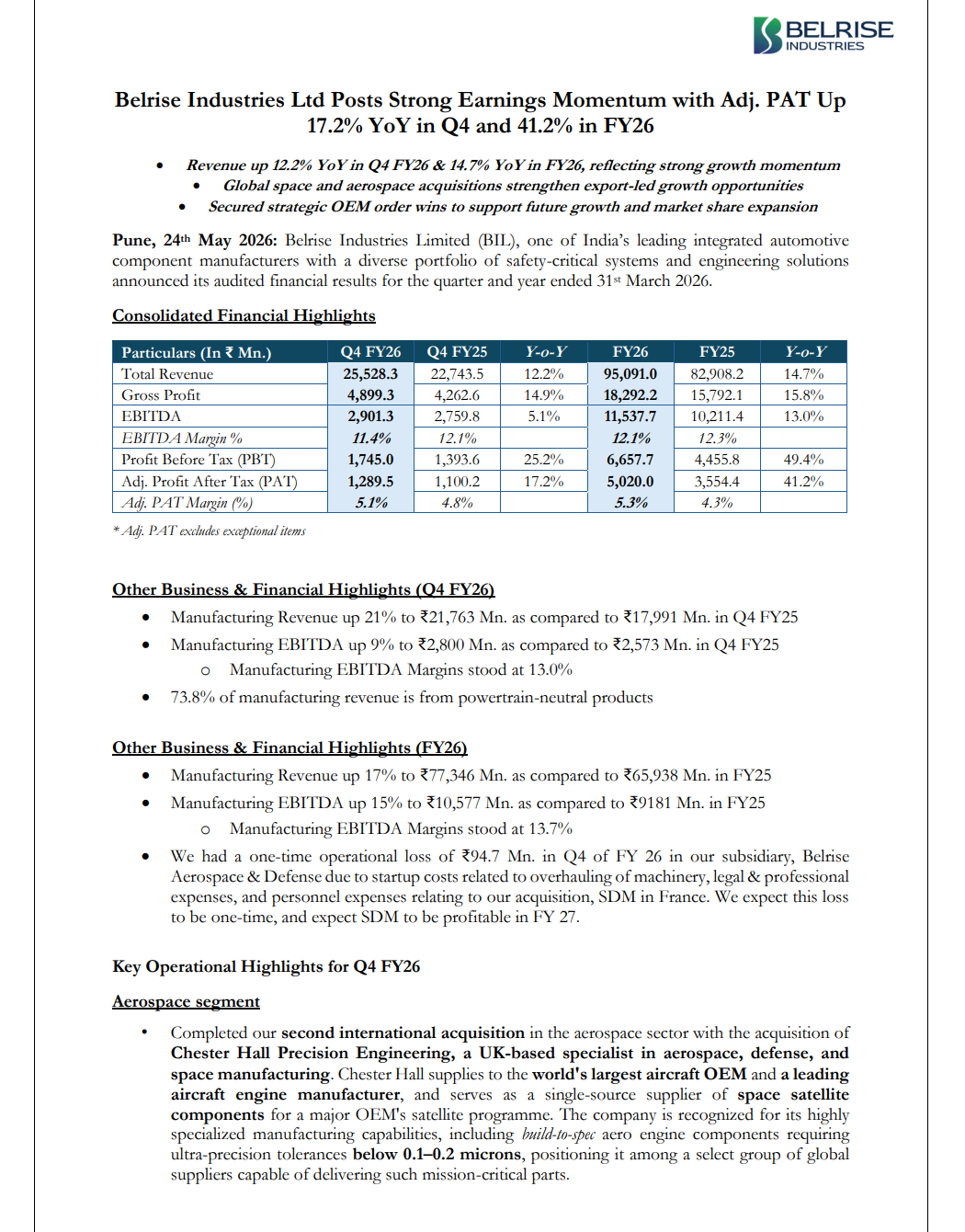

Belrise Industries Limited reported strong FY26 audited financial performance with total revenue rising 14.7% YoY to ₹9,509.1 crore and adjusted PAT increasing 41.2% YoY to ₹502 crore. Growth was supported by strong manufacturing execution, higher content per vehicle, strategic aerospace acquisitions, and major OEM order wins across two-wheeler and automotive segments.

PRICE-SENSITIVE TRIGGER

Event: FY26 Audited Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered steady revenue growth, margin stability, and strong earnings expansion while strengthening its aerospace business and securing new OEM supply programs expected to support future revenue growth.

Key Metrics:

- FY26 Total Revenue:

- ₹9,509.1 crore

- Up 14.7% YoY from ₹8,290.8 crore

- FY26 Gross Profit:

- ₹1,829.2 crore

- Up 15.8% YoY

- FY26 EBITDA:

- ₹1,153.8 crore

- Up 13.0% YoY from ₹1,021.1 crore

- FY26 EBITDA Margin:

- 12.1%

- Vs 12.3% in FY25

- FY26 Adjusted PAT:

- ₹502.0 crore

- Up 41.2% YoY from ₹355.4 crore

- FY26 Adjusted PAT Margin:

- 5.3%

- Vs 4.3% in FY25

- FY26 PBT:

- ₹665.8 crore

- Up 49.4% YoY

- Q4 FY26 Total Revenue:

- ₹2,552.8 crore

- Up 12.2% YoY

- Q4 FY26 Gross Profit:

- ₹489.9 crore

- Up 14.9% YoY

- Q4 FY26 EBITDA:

- ₹290.1 crore

- Up 5.1% YoY

- Q4 FY26 EBITDA Margin:

- 11.4%

- Vs 12.1% in Q4 FY25

- Q4 FY26 Adjusted PAT:

- ₹128.9 crore

- Up 17.2% YoY

- Manufacturing Revenue FY26:

- ₹7,734.6 crore

- Up 17% YoY

- Manufacturing EBITDA FY26:

- ₹1,057.7 crore

- Up 15% YoY

- Manufacturing EBITDA Margin FY26:

- 13.7%

- Powertrain-Neutral Revenue Contribution:

- 73.8% of manufacturing revenue

Highlight:

- Adjusted PAT surged 41.2% YoY in FY26 while the company strengthened its aerospace business through international acquisitions and strategic OEM wins.

What Happened ?

Belrise Industries Limited announced audited standalone and consolidated FY26 financial results reflecting strong operational momentum across automotive and aerospace segments.

The company reported:

- Double-digit revenue growth

- Strong adjusted profitability expansion

- Stable EBITDA margins

- Improved content per vehicle across multiple OEM platforms

Key strategic developments during FY26 included:

- Acquisition of Chester Hall Precision Engineering in the UK

- Continued integration of SDM in France

- Expansion into aerospace and defense precision engineering

- Major OEM order wins in two-wheeler and automotive segments

Management highlighted that the company is:

- Diversifying beyond automotive

- Building export-led aerospace capabilities

- Expanding precision engineering operations

- Increasing operational scale across global OEM supply chains

Belrise also reported significant progress in:

- Powertrain-neutral products

- Manufacturing efficiency

- Brownfield capacity expansion

- International aerospace supply integration

Key Details

Operational, Aerospace and OEM Expansion Highlights:

- Belrise completed the acquisition of Chester Hall Precision Engineering, a UK-based aerospace precision engineering company.

- Chester Hall supplies:

- Leading aircraft OEMs

- Aircraft engine manufacturers

- Satellite component programs

- Chester Hall specializes in:

- Titanium machining

- Advanced aerospace materials

- Ultra-precision components

- High-precision tolerance manufacturing below 0.1–0.2 microns

- The acquisition was completed for approximately £13.2 million.

- Chester Hall reported:

- Revenue exceeding £18.5 million in CY2025

- EBITDA of approximately £2.1 million

- Belrise indicated plans to transfer portions of subcontract manufacturing to India over time.

- The company secured a major order from a fast-growing two-wheeler and three-wheeler OEM for:

- Exhaust systems

- Fuel tanks

- Production for the above program is expected to commence from Q2 FY27 through a Bangalore brownfield expansion.

- Belrise also secured a major order from a Japanese OEM for:

- Complete exhaust systems

- Clutch assemblies

- Other automotive components

- The Japanese OEM program is expected to generate peak annual revenues of approximately ₹220 crore starting Q4 FY27.

- Manufacturing revenue growth was supported by:

- Higher content per vehicle

- Better operational efficiencies

- Strong customer execution

- Content per vehicle improved:

- ~65–70% in two-wheelers

- ~40–45% in four-wheelers and commercial vehicles

Note:

- The company stated that its aerospace acquisitions and OEM order pipeline are expected to strengthen export-led growth and long-term diversification beyond traditional automotive segments.

Risk Analysis

Summary:

- Despite strong growth momentum, Belrise remains exposed to automotive demand cycles, integration risks from international acquisitions, and execution risks related to new OEM programs and aerospace expansion.

Key Risks:

- EBITDA margins moderated slightly in Q4 FY26.

- Integration of aerospace acquisitions may create operational and execution challenges.

- Aerospace precision manufacturing requires sustained quality and regulatory compliance.

- Automotive demand remains cyclical and sensitive to macroeconomic conditions.

- Ramp-up of new OEM programs depends on timely production scaling.

- International operations may expose the company to currency and geopolitical risks.

- Startup-related costs in aerospace subsidiaries impacted profitability during FY26.

- Execution of brownfield expansion projects remains critical for future growth realization.

Worst Case Scenario:

- Delays in integrating aerospace assets, slower OEM demand, or operational inefficiencies in new manufacturing programs could pressure profitability and delay expected revenue ramp-up.

Risk Level: Medium

Company Commentary

- Management stated FY26 was Belrise’s first full financial year as a listed company with strong execution across operational commitments.

- The company highlighted stable EBITDA margins and sustained revenue growth despite industry challenges.

- Belrise stated that aerospace acquisitions significantly strengthen its global OEM supply-chain presence.

- Management emphasized continued focus on:

- Operational resilience

- Capacity expansion

- Precision engineering

- Export-led growth

- Long-term value creation

- The company reiterated that increasing content per vehicle and diversification into aerospace and defense remain major strategic growth drivers.

- Belrise stated it remains focused on sustaining long-term growth through operational efficiency, customer relationships, and strategic investments.

Official Exchange Filing: Belrise Industries Limited