Credit Rating Reaffirmation

Birla Corporation’s Subsidiary RCCPL Receives CARE AA; Stable Credit Rating Reaffirmation

NSE

birlacorpn

BSE

500335

CARE Ratings has reaffirmed the long-term and short-term bank facility ratings of RCCPL Private Limited, the wholly owned material subsidiary of Birla Corporation Limited, maintaining a Stable outlook. The reaffirmation reflects RCCPL’s strategic importance to the group, healthy operating profile, and improving financial metrics despite ongoing capacity expansion.

PRICE-SENSITIVE TRIGGER

Event: CARE Ratings reaffirmed the credit ratings of RCCPL Private Limited’s bank loan facilities.

Type: Credit Rating Reaffirmation

Impact: Positive

Immediate Effect: The reaffirmation maintains RCCPL’s strong credit profile, supporting continued access to bank financing for ongoing operations and planned capacity expansion.

Key Metrics:

- Credit Rating Agency: CARE Ratings Limited

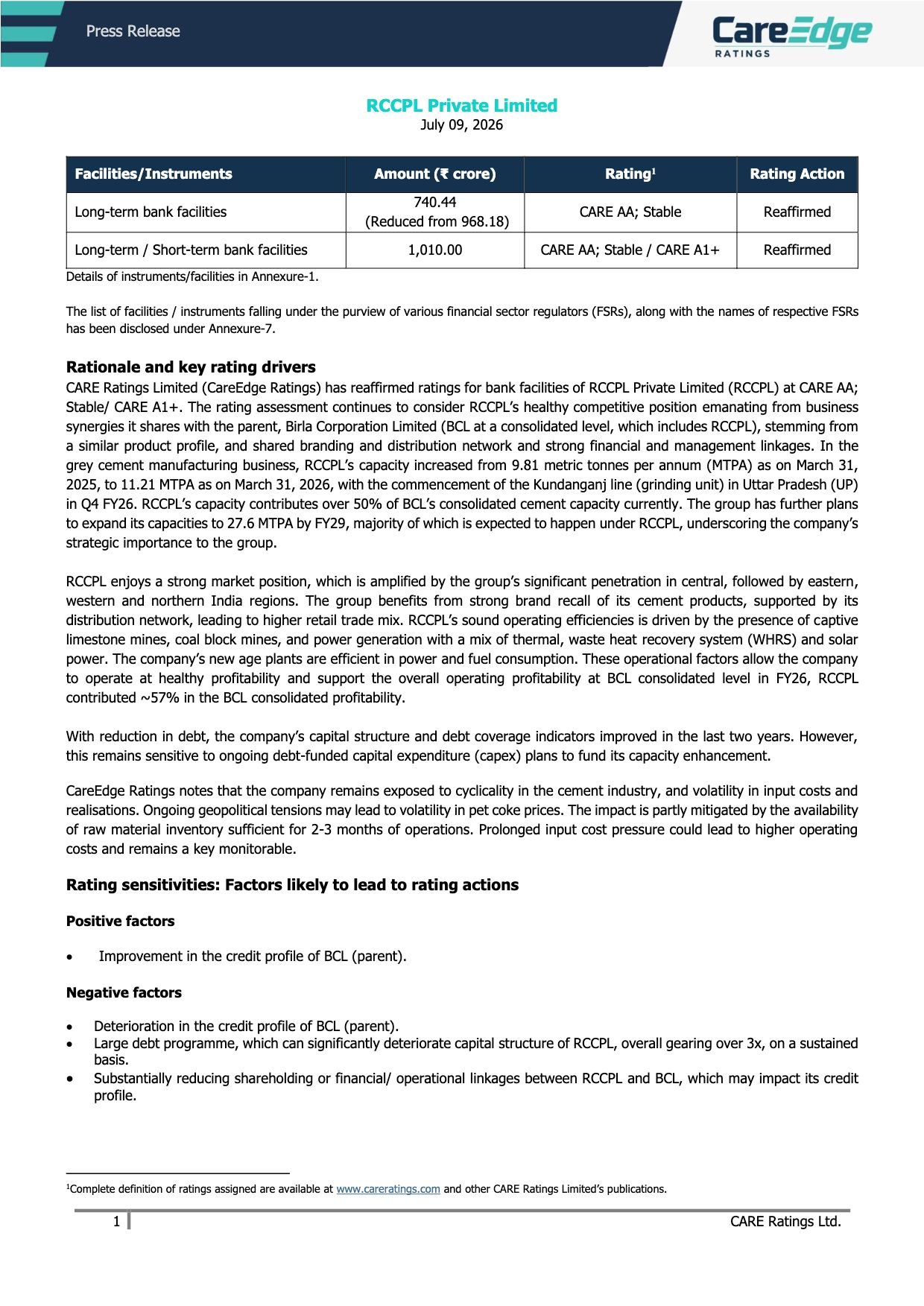

- Long-Term Bank Facilities: ₹740.44 crore — CARE AA; Stable (Reaffirmed)

- Long-Term / Short-Term Bank Facilities: ₹1,010.00 crore — CARE AA; Stable / CARE A1+ (Reaffirmed)

- FY26 Total Operating Income: ₹4,642.65 crore

- FY26 PBILDT: ₹838.63 crore

- FY26 PAT: ₹310.90 crore

- Overall Gearing: Improved to 0.93x (from 1.13x)

- Interest Coverage: Improved to 4.61x (from 3.59x)

- Installed Cement Capacity: Increased to 11.21 MTPA from 9.81 MTPA

- FY26 Cement Sales Volume: 9.30 MT (up from 8.71 MT in FY25)

Highlight:

- CARE Ratings reaffirmed RCCPL’s CARE AA; Stable / CARE A1+ ratings, citing strong parent support, improving leverage, operational efficiencies, and strategic importance within Birla Corporation.

What Happened ?

Birla Corporation Limited informed the stock exchanges that CARE Ratings Limited has reaffirmed the credit ratings assigned to the bank loan facilities of RCCPL Private Limited, its wholly owned material subsidiary.

The rating agency retained the CARE AA; Stable rating for long-term facilities and CARE AA; Stable / CARE A1+ for long-term and short-term facilities. The reaffirmation reflects RCCPL’s strong integration with Birla Corporation, healthy operating performance, improving debt metrics, and expanding cement manufacturing capacity.

key details

Rating Rationale:

- CARE reaffirmed CARE AA; Stable for ₹740.44 crore of long-term bank facilities.

- CARE reaffirmed CARE AA; Stable / CARE A1+ for ₹1,010 crore of long-term and short-term bank facilities.

- RCCPL contributes more than 50% of Birla Corporation’s consolidated cement capacity.

- Cement capacity increased from 9.81 MTPA to 11.21 MTPA following commissioning of the Kundanganj grinding unit in Uttar Pradesh.

- The Birla group plans to expand consolidated cement capacity to 27.6 MTPA by FY29, with a majority of expansion under RCCPL.

- RCCPL accounted for approximately 57% of Birla Corporation’s consolidated operating profitability in FY26.

- Overall gearing improved to 0.93x, while interest coverage strengthened to 4.61x, indicating an improving financial profile.

- CARE maintained a Stable Outlook, expecting the company to sustain its financial risk profile while continuing healthy operating performance.

Note:

- The reaffirmation is a credit quality assessment and does not represent new funding. It indicates continued lender confidence in RCCPL’s financial strength and its strategic role within Birla Corporation.

Risk Analysis

Summary:

- While the rating remains strong, CARE Ratings highlighted that future leverage from debt-funded expansion, cyclical cement demand, and volatility in fuel and raw material costs remain key monitoring factors.

Key Risks:

- Large debt-funded capacity expansion may increase leverage over the medium term.

- Cement demand remains cyclical and linked to economic activity.

- Volatility in coal, pet coke, diesel, and other input costs could pressure margins.

- Geopolitical developments may increase fuel procurement costs.

- Any deterioration in Birla Corporation’s credit profile could affect RCCPL’s ratings.

Worst Case:

- Significant deterioration in leverage, overall gearing above 3x on a sustained basis, weakening parent support, or substantial financial underperformance could result in a future credit rating downgrade.

Risk Level: Medium

Company Commentary

- CARE Ratings reaffirmed CARE AA; Stable and CARE AA; Stable / CARE A1+ ratings for RCCPL’s bank facilities.

- RCCPL continues to benefit from strong operational, financial, branding, and management linkages with Birla Corporation.

- The company remains focused on expanding cement capacity while maintaining healthy operating performance.

- The rating agency expects RCCPL to sustain its financial profile under a Stable Outlook despite ongoing expansion plans.

Official Exchange Filing: Birla Corporation Limited