Earnings Release

Cipla Reports FY26 Results with Record Revenue; Final Dividend of ₹13 per Share Recommended

NSE

cipla

BSE

500087

Cipla Limited reported audited FY26 consolidated revenue of ₹28,163 crore, up 2% YoY, while EBITDA stood at ₹5,925 crore. The company delivered strong growth in India and Africa markets despite weakness in North America. The Board recommended a final dividend of ₹13 per equity share for FY26.

PRICE-SENSITIVE TRIGGER

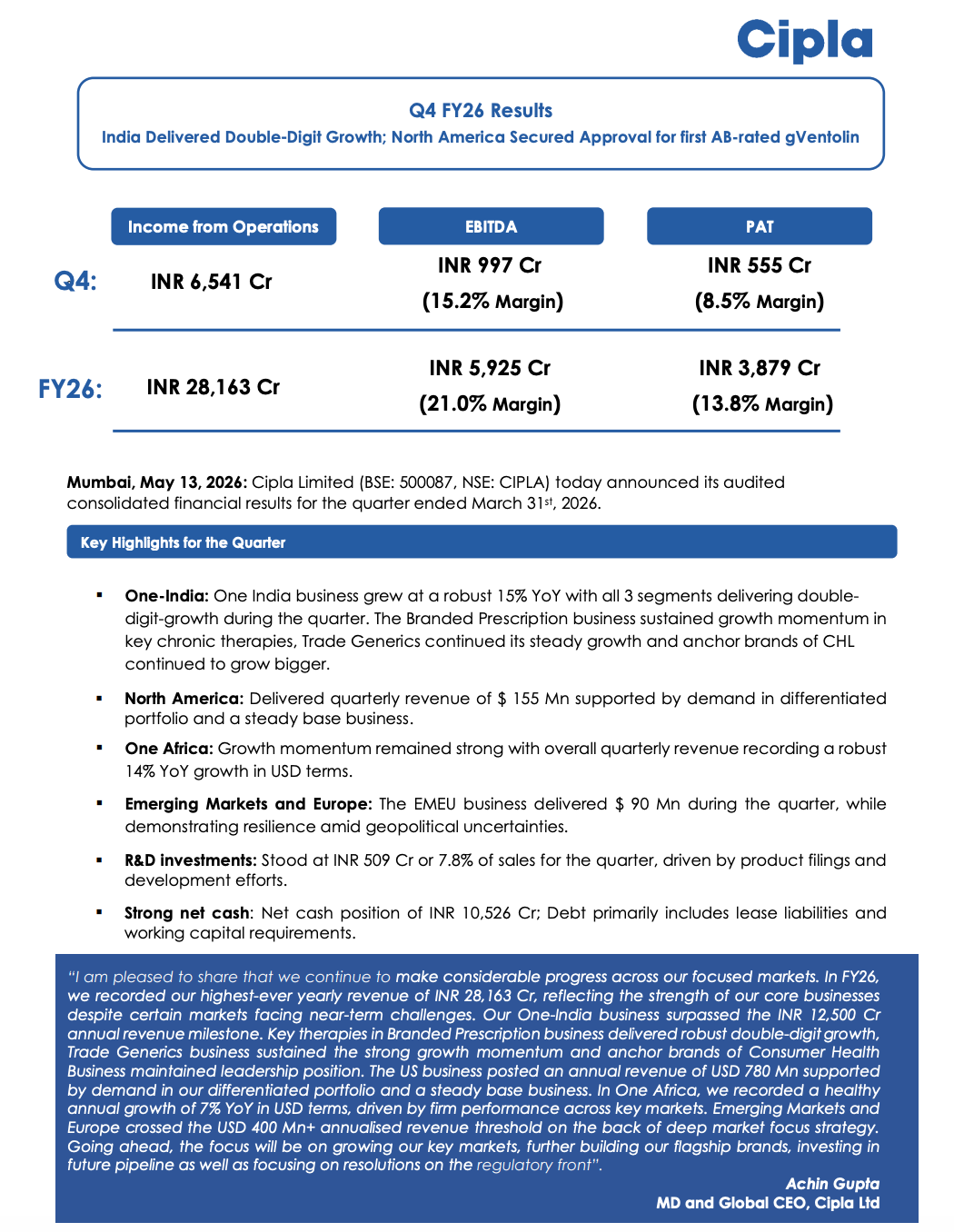

Event: Q4 FY26 and FY26 Audited Financial Results

Type: Earnings Release

Impact: Neutral

Immediate Effect: Strong India and Africa growth supported annual performance, though pressure in North America and lower profitability impacted margins and PAT during Q4 and FY26.

Key Metrics:

- FY26 Revenue: ₹28,163 Cr (+2% YoY)

- FY26 EBITDA: ₹5,925 Cr

- FY26 EBITDA Margin: 21.0%

- FY26 PAT: ₹3,879 Cr

- Q4 FY26 Revenue: ₹6,541 Cr (-3% YoY)

- Q4 FY26 EBITDA: ₹997 Cr

- Q4 FY26 PAT: ₹555 Cr

- Final Dividend Recommended: ₹13 per equity share

- Net Cash Position: ₹10,526 Cr

Highlight:

- Label: FY26 Revenue

- Value: ₹28,163 Cr

What Happened ?

Cipla Limited announced its audited consolidated financial results for Q4 FY26 and FY26.

The company reported FY26 revenue growth of 2% YoY to ₹28,163 crore, driven by strong performance in India and Africa businesses. EBITDA for FY26 stood at ₹5,925 crore with EBITDA margin of 21.0%, while PAT came at ₹3,879 crore.

For Q4 FY26, revenue declined 3% YoY to ₹6,541 crore, while EBITDA and PAT fell to ₹997 crore and ₹555 crore respectively, mainly due to normalization in North America business and lower margins.

The Board recommended a final dividend of ₹13 per equity share for FY26, subject to shareholder approval.

key highlights

Business Performance & Operational Highlights:

- India business delivered strong 15% YoY growth in Q4 FY26.

- One India business crossed ₹12,500 crore annual revenue milestone in FY26.

- North America business generated annual revenue of US$780 million despite quarterly weakness.

- Cipla received USFDA approval for first AB-rated gVentolin product with CGT.

- One Africa business reported healthy 7% annual growth in USD terms.

- Emerging Markets and Europe business crossed US$400 million annual revenue milestone.

- R&D investments stood at ₹509 crore during Q4 FY26.

- Company maintained strong net cash position of ₹10,526 crore.

- USFDA inspections at Bengaluru, Navi Mumbai, and Goa facilities received “VAI” or “NAI” classification.

- Consumer Health brands Nicotex, Omnigel, and Cipladine maintained leadership positions.

Note:

- The company highlighted resilient India operations and continued global diversification despite pressure in certain international markets.

Risk Analysis

Key Risks

- North America revenue declined during Q4 FY26.

- EBITDA margin declined to 15.2% in Q4 FY26 from 22.8% last year.

- FY26 PAT declined compared to FY25 levels.

- US generic pricing pressure and regulatory risks remain key concerns.

- Currency fluctuations and geopolitical uncertainties may impact overseas businesses.

Worst Case Scenario

- Sustained pricing pressure in the US market, regulatory setbacks, or margin compression across global operations could impact future profitability and earnings growth.

Risk Level: Medium

Company Commentary

- Management stated FY26 marked Cipla’s highest-ever annual revenue.

- Cipla highlighted robust double-digit growth in key chronic therapies within India.

- The company emphasized continued expansion in differentiated portfolios across North America.

- Management reiterated focus on flagship brands, future pipeline investments, and regulatory compliance.

- Cipla stated that strong net cash position provides flexibility for long-term growth investments.

Official Exchange Filing: Cipla Limited