Business Outlook

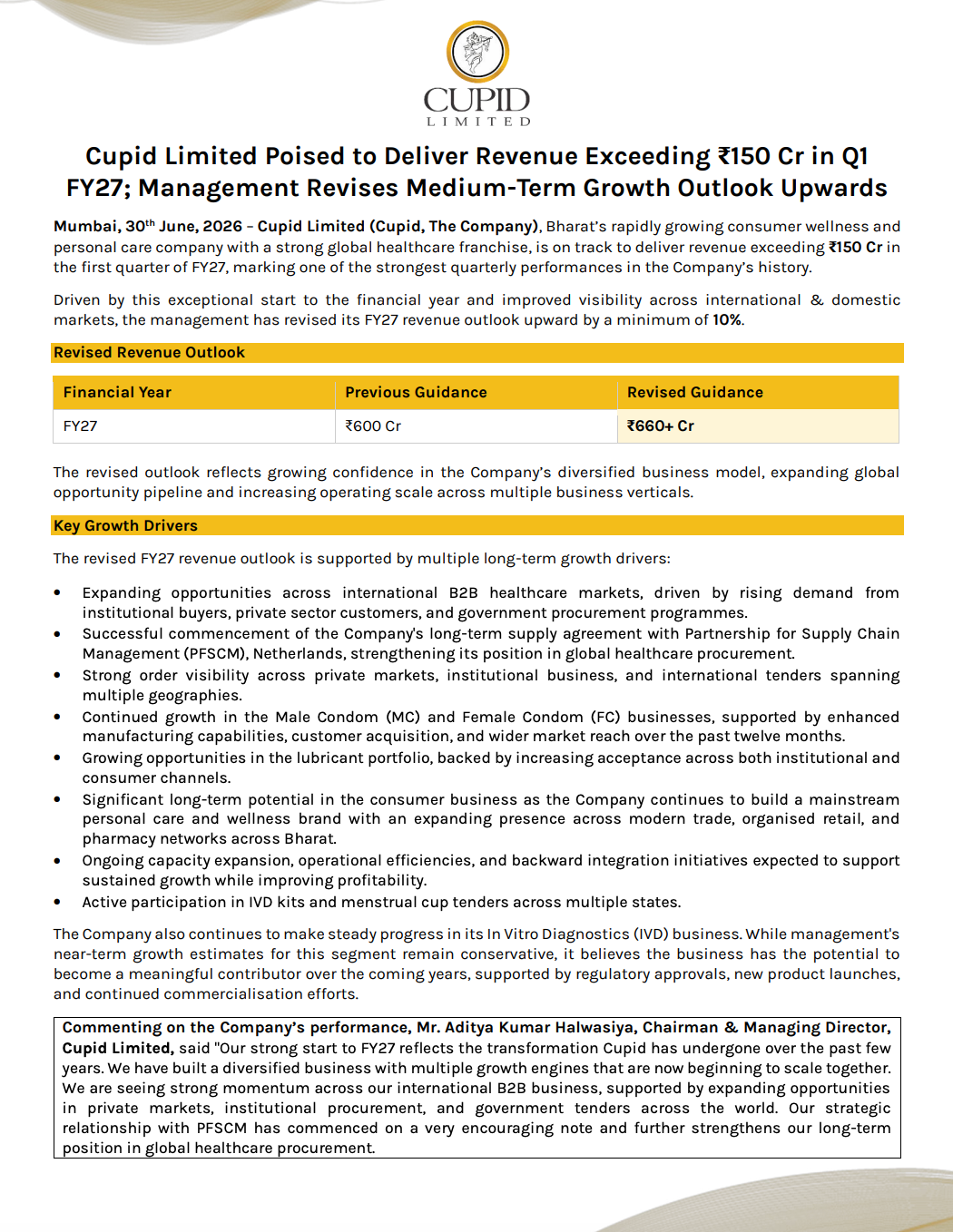

Cupid Limited Revises FY27 Revenue Outlook Upward; Expects Q1FY27 Revenue to Cross ₹150 Crore

NSE

cupid

BSE

530843

Cupid Limited has announced a strong business update, projecting Q1FY27 revenue to exceed ₹150 crore and revising its FY27 revenue guidance upward from ₹600 crore to over ₹660 crore. The company attributed the improved outlook to strong international demand, expanding manufacturing capabilities, growing order visibility, and continued progress across its healthcare and consumer wellness businesses.

PRICE-SENSITIVE TRIGGER

Event: Cupid Limited announced a Q1FY27 business update along with an upward revision of its FY27 revenue outlook.

Type: Business Outlook

Impact: Positive

Immediate Effect: The revised guidance reflects stronger-than-expected business momentum and improves revenue visibility for FY27.

Key Metrics:

- Q1FY27 Revenue: Expected to exceed ₹150 crore.

- FY27 Revenue Guidance (Previous): ₹600 crore.

- FY27 Revenue Guidance (Revised): ₹660+ crore.

- Guidance Revision: Minimum 10% increase over previous outlook.

- Margins: Profit margins expected to remain strong, supported by favourable USD-INR realizations and pricing trends.

- PAT: Management expects net profit margins to outperform its current guidance.

Highlight:

- Cupid Limited has raised its FY27 revenue guidance to over ₹660 crore, supported by strong order visibility and expanding global opportunities.

What Happened ?

Cupid Limited informed investors that it expects to deliver one of the strongest quarterly performances in its history, with Q1FY27 revenue projected to exceed ₹150 crore. Encouraged by improving visibility across domestic and international markets, the company has revised its FY27 revenue guidance upward by more than 10%, citing sustained business momentum and execution across multiple growth verticals.

Key Details

Business Update:

- FY27 revenue guidance increased from ₹600 crore to ₹660+ crore.

- Strong order book and expanding opportunity pipeline continue to improve business visibility.

- International B2B healthcare business continues to gain momentum.

- Long-term supply agreement with Partnership for Supply Chain Management (PFSCM), Netherlands, has commenced successfully.

- Institutional procurement, private markets and government tenders continue to support growth across multiple geographies.

Growth Drivers:

- Continued expansion in Male Condom and Female Condom businesses through improved manufacturing capacity and customer acquisition.

- Lubricants portfolio continues to witness healthy demand across institutional and consumer segments.

- Consumer wellness business is expanding through modern trade, organised retail and pharmacy channels.

- IVD business is expected to become a meaningful long-term growth contributor as commercialisation progresses.

- Capacity expansion, backward integration and operational efficiencies are expected to support future growth.

Operational Outlook:

- Medium-term revenue outlook has been revised upward based on stronger execution and market visibility.

- Profit margins are expected to remain healthy due to favourable currency movements and pricing trends.

- The new Palava manufacturing facility is expected to become operational during the coming quarter, strengthening production capacity.

- Management expects multiple business verticals to contribute meaningfully to future revenue and profitability.

Note:

- Management believes current projections remain conservative and provide room for additional upside as execution continues.

Risk Analysis

Summary:

- Although business momentum remains strong, the revised outlook depends on continued execution, capacity expansion and sustained demand across domestic and international markets.

Key Risks:

- Delay in commissioning the Palava manufacturing facility.

- Slower commercialisation of the IVD business.

- Currency volatility impacting export profitability.

- Execution risks across expanding international operations.

Worst Case:

- Delays in capacity expansion or weaker global healthcare procurement could moderate the company’s revised growth expectations.

Risk Level: Low

Company Commentary

- Strong Q1FY27 performance reflects the successful transformation of Cupid into a diversified healthcare and consumer wellness company.

- International healthcare opportunities continue to expand across institutional procurement and private markets.

- Consumer wellness and lubricants businesses continue to strengthen market presence across India.

- The IVD business has significant long-term growth potential.

- Management remains confident of sustaining strong revenue growth, healthy profitability and disciplined capital allocation.

- The company expects multiple business verticals to drive long-term shareholder value.

Official Exchange Filing: Cupid Limited