Credit Rating Reaffirmation

Elecon Engineering Credit Rating Reaffirmed at ICRA AA (Positive); A1+ for ₹400 Crore Bank Facilities

NSE

elecon

BSE

505700

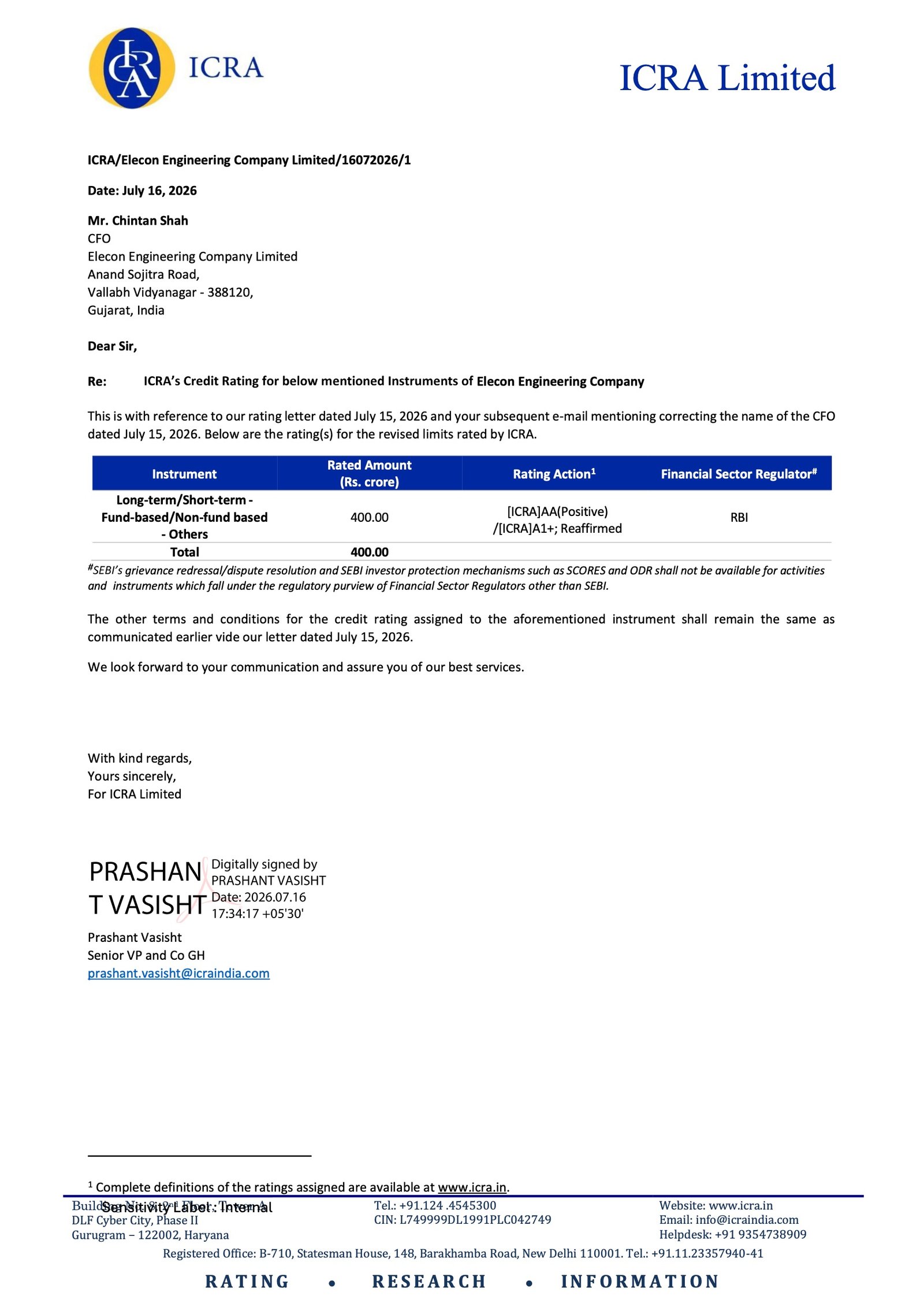

Elecon Engineering Company Limited has announced that ICRA Limited has reaffirmed the company’s credit ratings for its ₹400 crore long-term and short-term fund-based and non-fund-based bank facilities. The facilities continue to be rated [ICRA]AA (Positive) for long-term borrowings and [ICRA]A1+ for short-term borrowings, reflecting continued confidence in the company’s credit profile.

PRICE-SENSITIVE TRIGGER

Event: ICRA reaffirmed the credit ratings for the company’s bank facilities.

Type: Credit Rating Reaffirmation

Impact: Positive

Immediate Effect: The reaffirmation indicates that the company’s credit quality remains strong, supporting continued access to banking facilities under existing credit terms.

Metrics:

Key Metrics:

- Total Rated Bank Facilities: ₹400 crore

- Long-Term Rating: [ICRA]AA (Positive)

- Short-Term Rating: [ICRA]A1+

- Rating Action: Reaffirmed

Facility-wise Breakdown:

- State Bank of India: ₹170 crore

- Axis Bank: ₹70 crore

- HDFC Bank: ₹70 crore

- IDBI Bank: ₹90 crore

Highlight:

- Credit Rating: ICRA reaffirmed [ICRA]AA (Positive) and [ICRA]A1+ ratings for the company’s aggregate ₹400 crorebanking facilities.

What Happened ?

Elecon Engineering Company Limited informed the stock exchanges that ICRA Limited has reaffirmed the company’s credit ratings for its long-term and short-term fund-based and non-fund-based banking facilities.

The reaffirmation covers aggregate banking limits of ₹400 crore and follows ICRA’s review of the revised limits. The rating agency confirmed that all other terms and conditions relating to the assigned ratings remain unchanged.

key details

Credit Rating Update:

- ICRA reaffirmed the [ICRA]AA (Positive) long-term rating.

- Short-term facilities continue to be rated [ICRA]A1+.

- The reaffirmation applies to both fund-based and non-fund-based banking facilities.

- The rating action covers total bank facilities of ₹400 crore.

Note:

- The announcement is a reaffirmation of existing ratings and does not represent a rating upgrade or downgrade.

Bank-wise Rated Facilities:

- State Bank of India: ₹170 crore

- Axis Bank: ₹70 crore

- HDFC Bank: ₹70 crore

- IDBI Bank: ₹90 crore

Note:

- All facilities continue to carry the same [ICRA]AA (Positive) / [ICRA]A1+ ratings.

Operational Significance:

- A reaffirmed AA (Positive) rating reflects strong credit quality and financial discipline.

- Stable ratings support continued access to working capital and long-term financing.

- The positive outlook indicates the rating agency’s favorable view of the company’s credit profile.

Note:

- The filing does not disclose any change in borrowing limits or financing structure beyond the reaffirmed facilities.

Risk Analysis

Summary:

- The rating reaffirmation indicates stable credit quality; however, future ratings will remain dependent on business performance, profitability, leverage, liquidity, and cash flow generation.

Key Risks:

- The announcement does not represent a rating upgrade.

- Future rating actions remain subject to financial and operating performance.

- Any deterioration in leverage, liquidity, or earnings could affect future credit assessments.

Worst Case:

- If the company’s financial profile weakens materially, ICRA could revise the outlook or downgrade the credit rating during subsequent reviews.

Risk Level: Low

Company Commentary

- ICRA reaffirmed the company’s [ICRA]AA (Positive) long-term rating.

- Short-term bank facilities continue to be rated [ICRA]A1+.

- The reaffirmation covers ₹400 crore of fund-based and non-fund-based banking facilities.

- The company submitted the disclosure under Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Official Exchange Filing: Elecon Engineering Company Limited