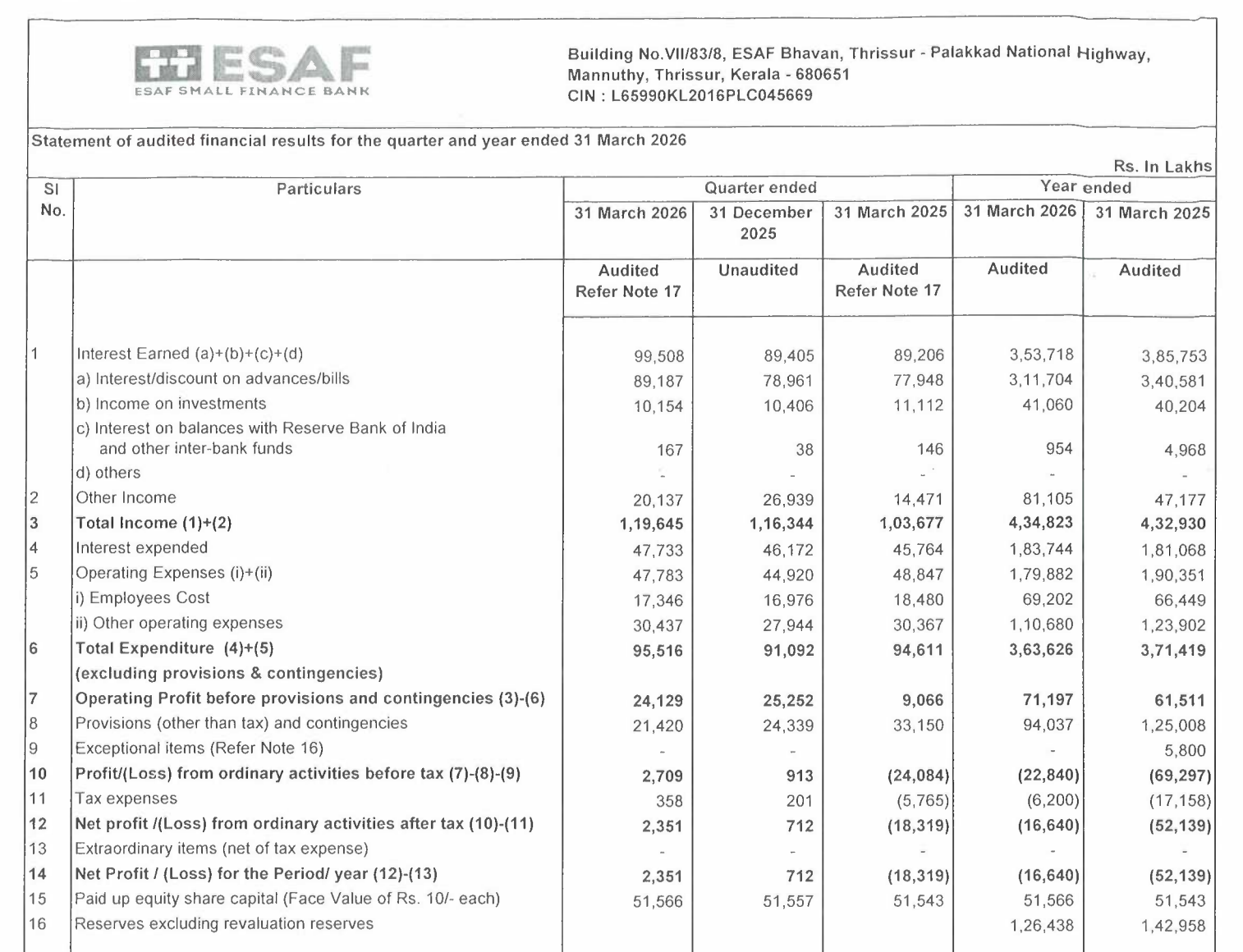

Quarter Ended: March 2026

ESAF Small Finance Bank – Q4 FY26 Results

NSE

esafsfb

BSE

543457

ESAF Bank delivered a sharp QoQ profit recovery, but underlying stress from NPAs and provisioning continues to impact overall earnings quality

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,19,645 Lakh

- QoQ Change: +2.83%

- YoY Change: +15.40%

- Previous Quarter (Q3 FY26): ₹1,16,344 Lakh

- Previous Year (Q4 FY25): ₹1,03,677 Lakh

- Revenue (Q4 FY26): ₹1,19,645 Lakh

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,351 Lakh

- QoQ Change: +230.1%

- YoY Change: Turnaround

- Previous Quarter (Q3 FY26): ₹712 Lakh

- Previous Year (Q4 FY25): ₹(18,319) Lakh Loss

- PAT (Q4 FY26): ₹2,351 Lakh

- QoQ Performance

- Revenue Trend: Stable growth

- Profit Trend: Strong recovery

Margin Analysis

Drivers:

- Lower provisioning compared to FY25

- Improvement in operating profitability

- Stable interest income

Insight:

- Margins are improving but remain structurally weak due to high credit cost

Segment performance

Segment: Retail

- Revenue: ₹1,01,530 Lakhs

- Loss-making segment despite dominance

Segment: Wholesale

- Revenue: ₹2,551 Lakhs

- Small but profitable

Segment: Treasury

- Revenue: ₹9,679 Lakhs

- Volatile performance

Segment: Other Banking Operations

- Revenue: ₹5,885 Lakhs

- Key profitability support

Segment insight

Summary:

- Retail dominates revenue but profitability is driven by non-core segments.

Charcateristics:

- Retail heavy book with stress

- Treasury volatility

- Other operations supporting profits

- Limited diversification

Earning quality check

Drivers:

- High provisioning (₹94,502 Lakhs)

- Low base effect aiding growth

- Improvement in operating profit

Interpretations:

- Earnings quality is weak-to-moderate, as profit recovery is not fully supported by stable asset quality

balance sheet Analysis

- Total Assets: ₹30,86,798 Lakhs

- Total Liabilities: ₹30,86,798 Lakhs

Insight:

- Balance sheet expansion is driven by deposits and advances growth, but rising borrowings signal funding pressure

key risks

- High GNPA (~5.41%)

- Low ROA (~0.08%)

- High provisioning requirement

- Retail loan stress

- Rising leverage

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹1,19,645 Lakhs | +2.83% | +15.40% |

| PBT | ₹2,709 Lakhs | +196.6% | Turnaround |

| PAT | ₹2,351 Lakhs | +230.1% | Turnaround |

This is a recovery quarter, not a turnaround yet. ESAF Bank is improving, but asset quality stress and weak profitability metrics keep the outlook cautiously mixed.

Official Exchange Filing: ESAF Small Finance Bank

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

80%

NET PROFIT AS % OF REVENUE

2%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED