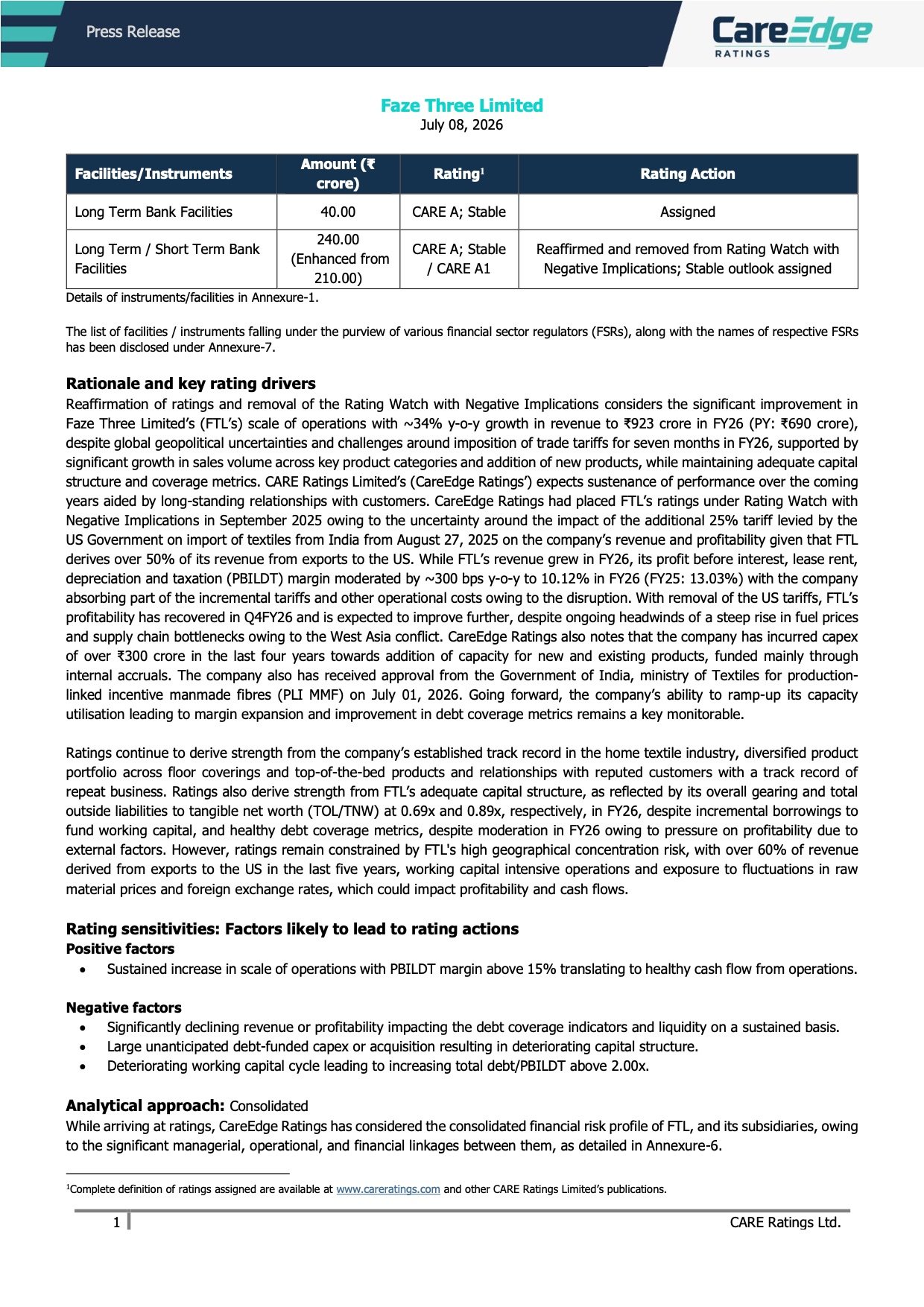

Credit Rating Reaffirmation

Faze Three Credit Rating Reaffirmed by CARE Ratings; ₹280 Crore Bank Facilities Retain CARE A; Stable / CARE A1

NSE

faze3q

BSE

530079

Faze Three Limited has announced that CARE Ratings Ltd. has reaffirmed the company’s credit ratings for its ₹280 crore bank facilities, assigning a Stable outlook and removing the facilities from Rating Watch with Negative Implications. The rating action reflects strong revenue growth in FY26, resilient business performance despite US tariff-related headwinds, and continued financial stability.

PRICE-SENSITIVE TRIGGER

Event: CARE Ratings reaffirmed Faze Three Limited’s long-term and short-term bank facility ratings while assigning a Stable outlook.

Type: Credit Rating Reaffirmation

Impact: Positive

Immediate Effect: The company’s aggregate bank facilities of ₹280 crore continue to be rated CARE A; Stable / CARE A1, with the earlier Rating Watch with Negative Implications withdrawn, indicating improved confidence in its financial and operational profile.

Financials:

Key Metrics:

- Revenue (FY26): ₹923.07 crore (+33.8% YoY)

- Revenue (FY25): ₹689.94 crore

- PBILDT (FY26): ₹93.46 crore

- PBILDT (FY25): ₹89.93 crore

- PBILDT Margin: 10.12% (vs. 13.03% in FY25)

- PAT (FY26): ₹33.57 crore

- PAT (FY25): ₹40.64 crore

- Overall Gearing: 0.69x

- Interest Coverage: 3.08x

- Working Capital Cycle: Improved to 116 days from 134 days

- Cash Flow from Operations (FY26): ₹35 crore

- Free Cash & Liquid Investments: ₹31 crore

- Rating: CARE A; Stable / CARE A1

- Total Rated Bank Facilities: ₹280 crore

Highlight:

- CARE Ratings removed the company from Rating Watch with Negative Implications after FY26 revenue increased nearly 34% to ₹923 crore while maintaining an adequate capital structure and debt coverage profile.

What Happened ?

Faze Three Limited informed the exchanges that CARE Ratings Ltd. has reaffirmed the company’s long-term and short-term bank facility ratings aggregating ₹280 crore at CARE A; Stable / CARE A1.

The rating agency also removed the company’s facilities from Rating Watch with Negative Implications, where they had been placed in September 2025 due to uncertainty surrounding additional US import tariffs on Indian textile exports.

CARE Ratings cited significant improvement in FY26 operating performance, healthy revenue growth, established customer relationships, adequate leverage metrics and sustained operational resilience as key reasons supporting the Stable outlook.

Key details

Rating Action:

- Long-term bank facilities of ₹40 crore assigned CARE A; Stable.

- Long-term/short-term bank facilities of ₹240 crore reaffirmed at CARE A; Stable / CARE A1.

- Rating Watch with Negative Implications has been removed.

- Stable outlook assigned following improved business performance.

Key Business Drivers:

- FY26 revenue increased by approximately 34% YoY.

- Growth supported by higher sales volumes across key product categories.

- New product additions contributed to revenue expansion.

- Long-standing relationships with global retailers continue to support order visibility.

- More than ₹300 crore invested over the past four years for capacity expansion, largely funded through internal accruals.

- The company also received approval under the Government’s PLI MMF scheme on 1 July 2026.

Financial Position:

- Capital structure remains comfortable despite higher working capital borrowings.

- Overall gearing remained below 1x at 0.69x.

- Debt servicing indicators continue to remain adequate.

- Liquidity remains sufficient with positive operating cash flows and ₹31 crore of free cash and liquid investments.

Note:

- CARE Ratings expects future performance to benefit from higher capacity utilisation, expanding product offerings and stable customer relationships. However, margin expansion and improvement in debt coverage metrics remain important monitoring factors.

Risk Analysis

Summary:

- Although the Stable outlook reflects improved financial resilience, the company remains exposed to external risks arising from export concentration, raw material price volatility and geopolitical developments.

Key Risks:

- Over 60% of revenue is generated from exports to the United States.

- Profitability remains sensitive to changes in global trade policies and tariffs.

- Exposure to cotton, polyester and foreign exchange fluctuations.

- Working capital requirements remain relatively high because of inventory-intensive operations.

- Rising logistics and fuel costs could pressure margins.

Worst Case:

- A sustained decline in export demand, renewed tariff-related disruptions or margin compression could weaken profitability, cash flows and debt coverage metrics, potentially affecting future credit ratings.

Risk Level: Medium

Company Commentary

- CARE Ratings has reaffirmed the company’s CARE A; Stable / CARE A1 ratings.

- Rating Watch with Negative Implications has been removed and replaced with a Stable outlook.

- Revenue growth and diversified product expansion supported the rating action.

- The company continues to maintain an adequate capital structure and debt servicing profile.

- Future growth is expected to be supported by recently added manufacturing capacity and continued customer relationships.

Official Exchange Filing: Faze Three Limited