Quarterly & Annual Financial Results

Fujiyama Power Systems Reports Strong FY26 Growth; Expands Solar Manufacturing Capacity

NSE

utlsolar

BSE

544613

Fujiyama Power Systems Limited (UTL Solar) reported robust FY26 financial performance driven by strong rooftop solar demand, higher backward integration, and expansion in manufacturing capacity. The company also announced ongoing investments in solar cell and power electronics manufacturing.

PRICE-SENSITIVE TRIGGER

Event: Q4FY26 and FY26 Financial Results Announcement with Buyback Approval

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong revenue growth, margin expansion, and aggressive capacity expansion plans reinforce the company’s growth outlook in India’s rapidly expanding rooftop solar market.

Key Metrics:

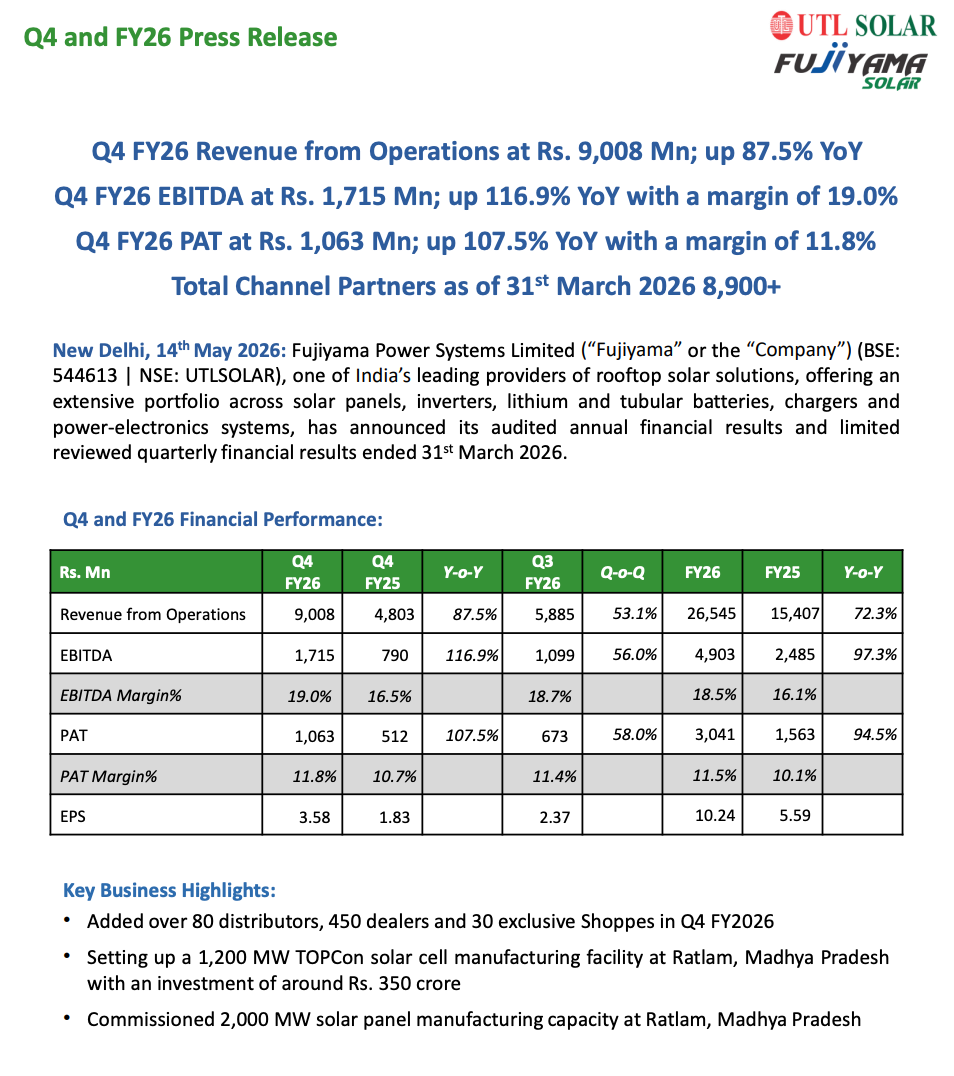

Q4FY26 Highlights:

- Revenue from Operations: ₹9,008 million (+87.5% YoY)

- EBITDA: ₹1,715 million (+116.9% YoY)

- EBITDA Margin: 19.0%

- PAT: ₹1,063 million (+107.5% YoY)

- PAT Margin: 11.8%

- EPS: ₹3.58

FY26 Highlights:

- Revenue from Operations: ₹26,545 million (+72.3% YoY)

- EBITDA: ₹4,903 million (+97.3% YoY)

- EBITDA Margin: 18.5%

- PAT: ₹3,041 million (+94.5% YoY)

- PAT Margin: 11.5%

- EPS: ₹10.24

Operational Highlights:

- Added over 80 distributors, 450 dealers, and 30 exclusive shoppes during Q4FY26.

- Total channel partner network crossed 8,900+.

- Commissioned 2,000 MW solar panel manufacturing capacity at Ratlam.

- Proposed 1,200 MW TOPCon solar cell manufacturing facility with investment of approximately ₹350 crore.

Highlight Metric:

- FY26 revenue surged 72.3% YoY to ₹26,545 million with PAT rising 94.5% YoY

What Happened ?

Fujiyama Power Systems announced audited annual and quarterly financial results for FY26, reporting strong growth across revenue, EBITDA, and profitability.

The company continued strengthening its manufacturing ecosystem, expanded its distribution network, and advanced backward integration initiatives in solar modules, solar cells, batteries, and power electronics.

key highlights

Manufacturing Expansion:

- Commissioned 2,000 MW solar panel manufacturing capacity at Ratlam, Madhya Pradesh.

- Developing a 1,200 MW TOPCon solar cell manufacturing facility.

- Expansion aligns with backward integration and domestic solar manufacturing strategy.

Distribution & Market Reach:

- Channel partner network crossed 8,900+.

- Strong presence in Tier-2 and Tier-3 cities continued driving rooftop solar adoption.

- Added new distributors, dealers, and exclusive retail outlets during FY26.

Product Portfolio:

- The company operates across:

- Solar panels

- Inverters

- Lithium batteries

- Tubular batteries

- Chargers

- Power electronics systems

Operational Commentary:

- Improved profitability was supported by higher operating leverage and utilization levels.

- Backward integration contributed positively to margins.

- Management highlighted strong demand for residential rooftop solar and power backup solutions.

Future Capacity Plan:

- Inverter manufacturing line expected to be commissioned by Q1FY27.

- Battery machinery orders placed; commissioning expected by Q2FY27.

- The company expects government-backed rooftop solar schemes to support future demand growth.

Note:

- The company’s manufacturing and supply-chain integration strategy is aimed at improving cost efficiency and reducing dependency on external sourcing.

Risk Analysis

Key Risks:

- Delays in commissioning new manufacturing lines.

- Dependence on government solar policies and subsidies.

- Competitive pricing pressure in solar equipment.

- Technology transition risks in solar cell manufacturing.

- Supply-chain disruptions and raw material volatility.

Worst Case Scenario:

- If demand growth slows or expansion projects face delays, the company may experience lower utilization and pressure on profitability despite heavy capex investments.

Risk Level: Medium

Company Commentary

- Management stated FY26 marked the company’s first full year as a listed entity and a major operational milestone.

- The company emphasized continued focus on backward integration and manufacturing scale-up.

- Management expects rooftop solar demand to remain strong due to supportive policies and rising consumer adoption.

- The company remains focused on operational efficiency, supply-chain resilience, and nationwide distribution expansion.

Official Exchange Filing: Fujiyama Power Systems Limited