Credit Rating

Goodluck India Receives India Ratings’ IND AA-/Stable & IND A1+ Rating for ₹1,150 Crore Bank Facilities

NSE

goodluck

BSE

530655

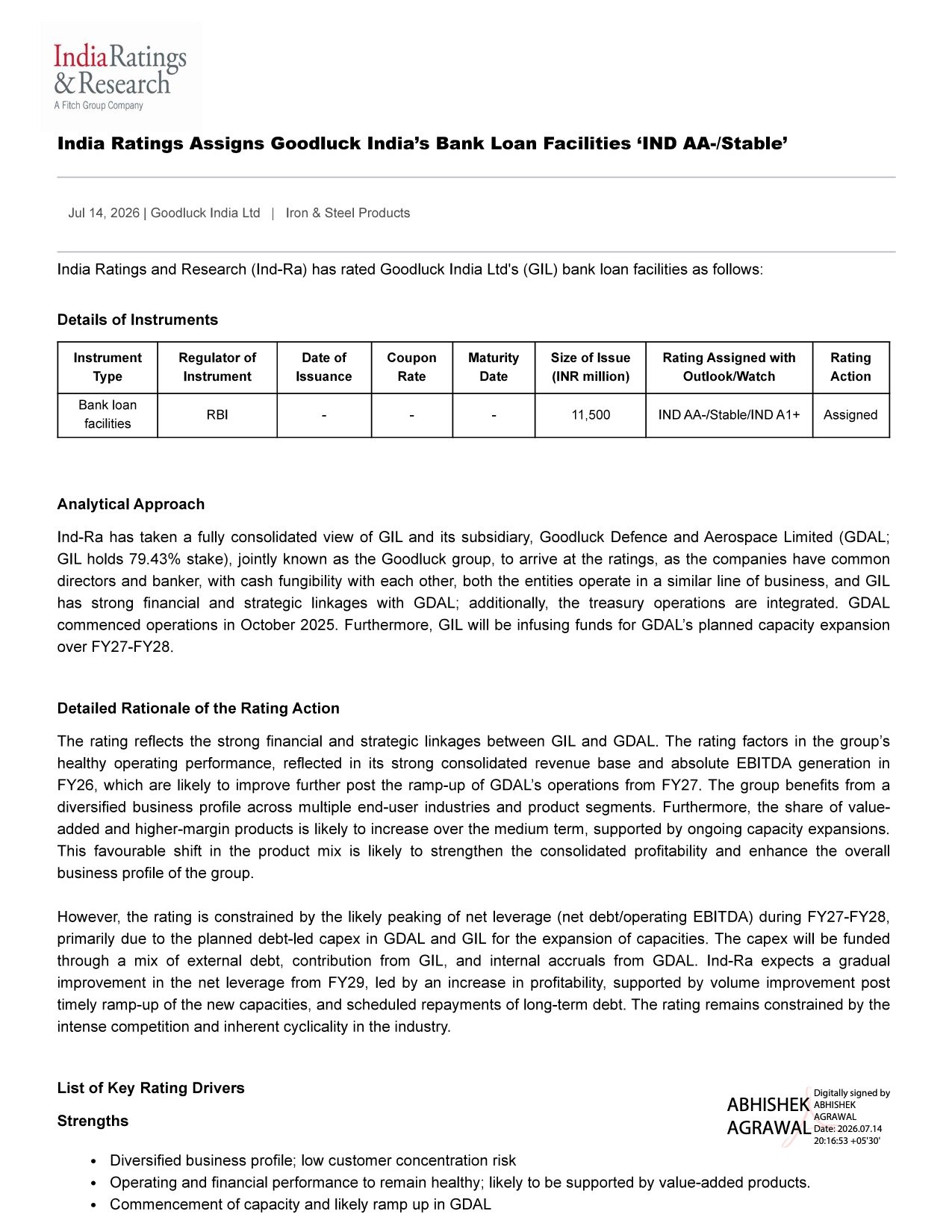

Goodluck India Limited has announced that India Ratings & Research (Ind-Ra) has assigned IND AA-/Stable for its long-term bank facilities and IND A1+ for short-term facilities covering total bank loan facilities of ₹11,500 million (₹1,150 crore). The rating reflects the company’s strong consolidated financial profile, strategic integration with Goodluck Defence and Aerospace Limited (GDAL), diversified business portfolio, and healthy profitability outlook.

PRICE-SENSITIVE TRIGGER

Event: India Ratings & Research assigned new credit ratings to Goodluck India Limited’s bank loan facilities.

Type: Credit Rating

Impact: Positive

Immediate Effect: The investment-grade rating strengthens the company’s credit profile and reflects lenders’ confidence in its financial strength, operational performance, and long-term business prospects.

Financials:

Metrics:

- Total Bank Loan Facilities Rated: ₹11,500 million (₹1,150 crore)

- Long-Term Rating: IND AA-/Stable

- Short-Term Rating: IND A1+

- Rating Agency: India Ratings & Research (Ind-Ra)

- Rating Action: Assigned

Highlight:

- India Ratings assigned Goodluck India’s ₹1,150 crore bank facilities an IND AA-/Stable and IND A1+ rating, citing strong consolidated financials, strategic business linkages, and diversified operations.

What Happened ?

Goodluck India Limited informed the stock exchanges that India Ratings & Research has assigned fresh credit ratings to the company’s bank loan facilities.

According to the accompanying rating rationale, Ind-Ra evaluated the consolidated Goodluck Group, including Goodluck Defence and Aerospace Limited (GDAL), owing to strong financial and strategic integration, common management, banking relationships, cash fungibility, and operational linkages. The agency expects these strengths to support the group’s credit profile despite ongoing expansion-led leverage.

key details

Rating Rationale:

- Rating based on the consolidated financial profile of Goodluck India and GDAL.

- GDAL is 79.43% owned by Goodluck India.

- Strong strategic and financial linkages exist between both entities.

- Treasury operations are integrated across the group.

- Goodluck India will support GDAL’s planned capacity expansion through FY27-FY28.

- GDAL commenced commercial operations in October 2025.

Note:

- Ind-Ra considered the group as an integrated operating platform while assigning the rating.

Key Credit Strengths:

- Diversified business profile across multiple end-user industries.

- Low customer concentration risk.

- Healthy operating and financial performance.

- Strong consolidated revenue base.

- Healthy EBITDA generation during FY26.

- Increasing contribution from value-added and higher-margin products.

- Capacity expansion expected to improve profitability over the medium term.

- New GDAL capacities expected to ramp up from FY27 onwards.

Growth Outlook:

- The rating agency expects ongoing capacity expansion and the gradual increase in value-added products to strengthen consolidated profitability over the coming years.

- The integration of GDAL’s new facilities is expected to contribute additional operating leverage once utilization improves.

Investor Relevance:

- Investment-grade rating supports stronger banking relationships.

- Reflects confidence in Goodluck India’s consolidated financial profile.

- Indicates adequate financial flexibility for future expansion plans.

- Positive validation of the group’s defence and aerospace diversification strategy through GDAL.

- Rating may improve financing efficiency as expansion projects progress successfully.

Risk Analysis

Summary:

- While the rating reflects strong business fundamentals, India Ratings highlighted that leverage is expected to peak during FY27-FFY28 due to debt-funded capacity expansion before gradually moderating.

Key Risks:

- Net leverage is expected to rise during FY27-FY28.

- Expansion projects are primarily debt funded.

- Timely ramp-up of new manufacturing capacities remains important.

- Scheduled repayment of long-term borrowings will influence future leverage.

- Steel industry remains cyclical and highly competitive.

- Delay in profitability improvement from new capacities could pressure credit metrics.

Worst Case:

- If capacity utilization ramps up slower than expected, debt remains elevated for longer, or profitability weakens due to industry cyclicality, leverage metrics could remain under pressure and affect future rating outlook.

Risk Level: Medium

Company Commentary

- Goodluck India informed exchanges that India Ratings & Research assigned IND AA-/Stable and IND A1+ ratings to its bank loan facilities.

- The company disclosed that the total bank facilities covered under the rating amount to ₹11,500 million (₹1,150 crore).

- The disclosure was made pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Official Exchange Filing: Goodluck India Limited