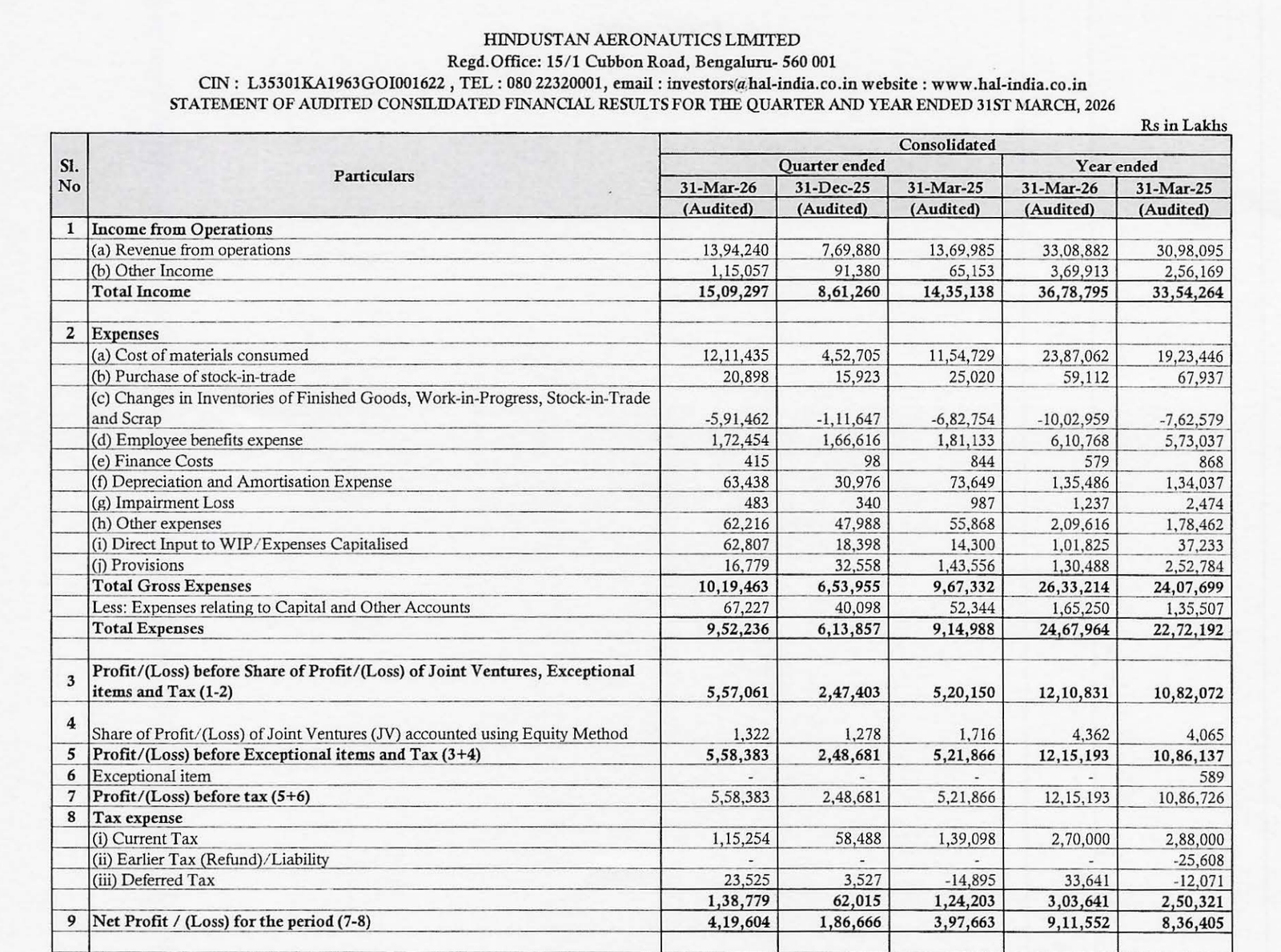

Quarter Ended: March 2026

Hindustan Aeronautics Limited – Q4 FY26 Results

NSE

hal

BSE

541154

Hindustan Aeronautics Limited delivered a strong Q4 FY26 performance with robust profitability, improved operational execution, and significant YoY earnings growth despite volatility in quarterly execution cycles.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹13,94,240 Lakh

- QoQ Change: +81.10%

- YoY Change: +1.77%

- Previous Quarter (Q3 FY26): ₹7,69,880 Lakh

- Previous Year (Q4 FY25): ₹13,69,985 Lakh

- Revenue (Q4 FY26): ₹13,94,240 Lakh

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹4,19,604 Lakh

- QoQ Change: +124.80%

- YoY Change: +5.52%

- Previous Quarter (Q3 FY26): ₹1,86,666 Lakh

- Previous Year (Q4 FY25): ₹3,97,663 Lakh

- PAT (Q4 FY26): ₹4,19,604 Lakh

- QoQ Performance:

- Revenue Trend: Strong Sequential Growth

- Profit Trend: Significant Sequential Expansion

Margin Analysis

Drivers:

- Higher execution volume in aerospace and defence manufacturing during Q4 FY26.

- Better operating leverage due to scale-up in production and delivery.

- Negative inventory movement supported profitability.

- Strong other income contribution aided earnings stability.

- Controlled finance costs despite higher operational scale.

Insight:

- HAL maintained strong profitability despite higher employee-related provisioning and pension contribution adjustments, indicating operational resilience and pricing strength in defence contracts.

Earning quality check

Key Drivers:

- Operating cash flow remained strong at ₹10,90,638 lakh.

- Working capital generation improved materially during FY26.

- Inventories increased due to execution cycle requirements.

- Other liabilities increased substantially due to contract execution advances.

- Finance costs remained negligible relative to profitability.

- Cash and bank balances continued at elevated levels.

Interpretations:

- HAL’s earnings quality remains strong as profitability is backed by healthy cash generation, robust balance sheet strength, and strong order execution capability.

balance sheet Analysis

- Total Assets: ₹1,32,41,459 lakh

- Total Liabilities: ₹91,36,999 lakh

Insight:

- The company maintains a very strong balance sheet with high liquidity, negligible debt exposure, strong cash reserves, and substantial working capital support from defence contracts.

key risks

- Revenue concentration on Government of India defence procurement.

- Delay in pricing finalisation under FPQ mechanism.

- Pension and gratuity liability revisions impacting employee costs.

- Long execution cycles in aerospace manufacturing.

- Exposure to project milestone delays and customer acceptance timelines.

- Joint venture operational uncertainties in certain subsidiaries/JVs.

management strategy signals

Focus Area:

- Expansion in defence aerospace manufacturing capacity.

- Strengthening indigenous defence production ecosystem.

- Focus on helicopters, aircraft platforms, and avionics programs.

- Long-term defence execution visibility.

- Investment in advanced aerospace technologies and infrastructure.

- Improved working capital and execution management.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹15,09,297 Lakh | +75.24% | +5.16% |

| PBT | ₹5,58,383 Lakh | +124.54% | +7.00% |

| PAT | ₹4,19,604 Lakh | +124.80% | +5.52% |

Hindustan Aeronautics Limited delivered a fundamentally strong Q4 FY26 performance with robust execution-led growth, strong margins, excellent cash generation, and a very healthy balance sheet.

The company continues to benefit from India’s long-term defence indigenisation push and remains strategically positioned for sustained long-term growth despite periodic execution volatility and policy-linked pricing adjustments.

Official Exchange Filing: Hindustan Aeronautics Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED