Regulatory Filing

HLE Glascoat Credit Ratings Reaffirmed by ICRA; Stable Outlook Maintained Across Key Banking Facilities

NSE

hleglas

BSE

522215

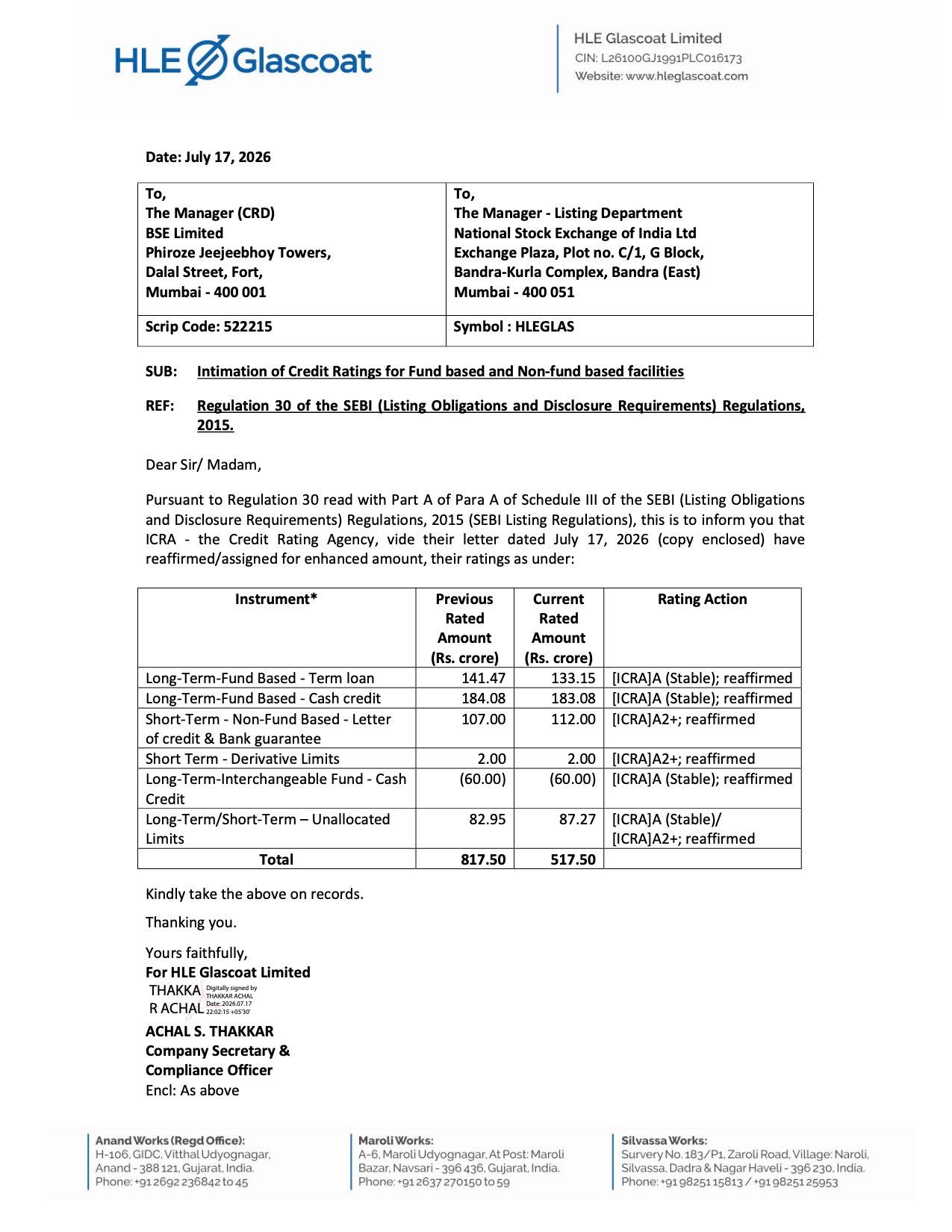

- HLE Glascoat Limited has informed the stock exchanges that ICRA has reaffirmed its long-term and short-term credit ratings for its fund-based and non-fund-based banking facilities.

- The reaffirmation reflects the company’s established market position, diversified engineering portfolio, healthy order book, comfortable capital structure and adequate liquidity despite temporary pressure on profitability arising from recent acquisitions.

PRICE-SENSITIVE TRIGGER

Event: ICRA Reaffirms Credit Ratings

Type: Regulatory Filing

Impact: Positive

Immediate Effect: ICRA reaffirmed HLE Glascoat’s long-term [ICRA]A (Stable) ratings and short-term [ICRA]A2+ ratings across its key banking facilities. The reaffirmation indicates continued confidence in the company’s credit profile and financial strength.

financials:

Revenue:

- FY2026 Operating Income: ₹1,353.0 crore

- FY2025 Operating Income: ₹1,027.6 crore

- YoY Growth: Approximately 32%

EBITDA:

- FY2026 EBITDA Margin (OPBDIT/OI): 10.3%

- FY2025 EBITDA Margin: 13.0%

- YoY Movement: Margin declined due to losses from the recently acquired Omeras business, integration expenses and pressure in the domestic glass-lined equipment segment.

PAT:

- FY2026 PAT: ₹56.6 crore

- FY2025 PAT: ₹61.8 crore

- YoY Movement: Declined by approximately 8.4%.

Margins:

- PAT Margin FY2026: 4.2%

- PAT Margin FY2025: 6.0%

- EBITDA Margin FY2026: 10.3%

- EBITDA Margin FY2025: 13.0%

QoQ / YoY Movement:

- PAT Margin FY2026: 4.2%

- PAT Margin FY2025: 6.0%

- EBITDA Margin FY2026: 10.3%

- EBITDA Margin FY2025: 13.0%

Segment Performance:

The filing does not provide segment-wise financial results. However, ICRA highlighted healthy performance across:

- Glass-Lined Equipment (GLE)

- Filtration & Drying (F&D)

- Heat Transfer Equipment

- Glass-Fused-to-Steel Storage Solutions

The company also continued to benefit from contributions from Kinam Engineering and the first-time consolidation of Omeras.

Highlight:

- ICRA reaffirmed HLE Glascoat’s long-term [ICRA]A (Stable) and short-term [ICRA]A2+ ratings while recognizing 32% revenue growth, a healthy ₹682 crore order book and improving leverage metrics.

What Happened ?

HLE Glascoat informed the exchanges that ICRA has reaffirmed its credit ratings for multiple banking facilities, including term loans, cash credit facilities, letters of credit, bank guarantees, derivative limits and unallocated limits.

The rating agency cited the company’s established leadership in process equipment, successful acquisition-led diversification, healthy order inflows and comfortable balance sheet as key factors supporting the reaffirmation. At the same time, ICRA noted that profitability moderated during FY2026 because of integration costs and losses associated with the recently acquired Omeras business.

key details

Credit Rating Action:

- Long-Term Term Loan: [ICRA]A (Stable) reaffirmed.

- Long-Term Cash Credit: [ICRA]A (Stable) reaffirmed.

- Short-Term Letter of Credit & Bank Guarantee: [ICRA]A2+ reaffirmed.

- Short-Term Derivative Limits: [ICRA]A2+ reaffirmed.

- Long-Term Interchangeable Cash Credit: [ICRA]A (Stable) reaffirmed.

- Long-Term/Short-Term Unallocated Limits: [ICRA]A (Stable)/[ICRA]A2+ reaffirmed.

Key Strengths Highlighted by ICRA:

- Established leadership across glass-lined equipment, filtration & drying and process equipment.

- Diversified engineering portfolio following acquisitions of Thaletec, Kinam Engineering and Omeras.

- Healthy consolidated order book of approximately ₹682 crore as of 31 March 2026.

- Strong demand outlook from pharmaceutical, specialty chemicals, oil & gas, water treatment and biogas sectors.

- Comfortable capital structure with improving leverage.

- Diversified customer base and manufacturing footprint across India and Germany.

Operational Developments:

ICRA noted that the acquisitions have expanded HLE Glascoat’s:

- Technology capabilities.

- International market presence.

- Product portfolio.

- Cross-selling opportunities.

- Exposure to renewable energy and water infrastructure applications.

Liquidity Position:

The agency assessed the company’s liquidity as Adequate, supported by:

- Free cash balances of approximately ₹34.4 crore.

- Comfortable debt repayment profile.

- Improved working capital intensity.

- Healthy operating cash generation.

- Planned capex of ₹25–30 crore for the Omeras India facility, expected to be funded through internal accruals and debt.

Note:

- ICRA expects future growth to be supported by the company’s healthy order pipeline, stronger pharmaceutical and specialty chemical demand, increasing opportunities in oil & gas through Kinam, and the gradual turnaround of Omeras.

Risk Analysis

Summary:

- Although the company’s credit profile remains stable, ICRA identified profitability, working capital intensity and integration of acquired businesses as the principal factors that could influence future ratings.

Key Risks:

- Working-capital-intensive operations because of long manufacturing cycles.

- Profitability pressure from Omeras integration and lower margins.

- Exposure to cyclical capital expenditure by pharmaceutical and chemical industries.

- Raw material price volatility.

- Execution and integration risks associated with recently acquired businesses.

- Dependence on sustained improvement in Omeras’ operational performance.

Worst Case:

- Any sustained decline in revenue or profitability, deterioration in working capital or significant debt-funded expansion could weaken leverage metrics and lead to downward pressure on the company’s credit ratings.

Risk Level: Medium

Company Commentary

- ICRA reaffirmed all major long-term and short-term ratings with a Stable outlook.

- Revenue growth remained strong during FY2026 despite temporary profitability pressure.

- The company maintains a diversified engineering portfolio across multiple industrial sectors.

- Healthy order inflows and a strong order book provide revenue visibility for FY2027.

- Improving leverage, comfortable liquidity and strategic acquisitions continue to support the company’s long-term credit profile.

Official Exchange Filing: HLE Glascoat Limited