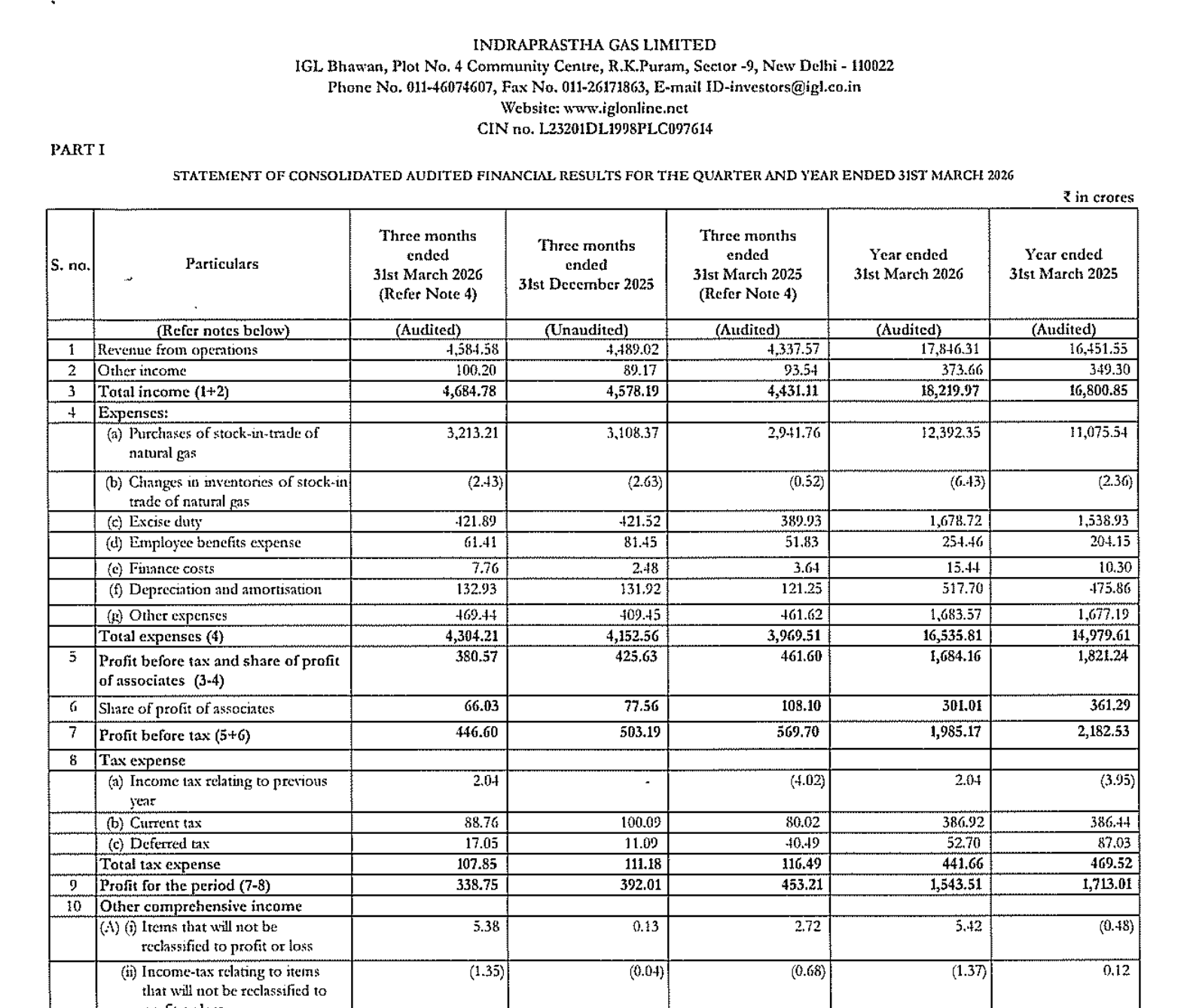

Quarter Ended: March 2026

Indraprastha Gas Limited – Q4 FY26 Results

NSE

igl

BSE

532514

Indraprastha Gas Limited reported a subdued Q4 FY26 performance with revenue growth remaining stable, while profitability declined sharply due to weaker operating margins and elevated gas procurement costs.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹4,584.58 Crore

- QoQ Change: +2.13%

- YoY Change: +5.69%

- Previous Quarter (Q3 FY26): ₹4,489.02 Crore

- Previous Year (Q4 FY25): ₹4,337.57 Crore

- Revenue (Q4 FY26): ₹4,584.58 Crore

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹338.75 Crore

- QoQ Change: -13.59%

- YoY Change: -25.25%

- Previous Quarter (Q3 FY26): ₹392.01 Crore

- Previous Year (Q4 FY25): ₹453.21 Crore

- PAT (Q4 FY26): ₹338.75 Crore

- QoQ Performance:

- Revenue Trend: Moderately Positive

- Profit Trend: Negative due to lower operating spreads and margin pressure.

- Revenue Trend: Moderately Positive

Margin Analysis

Drivers:

- Higher natural gas procurement costs.

- Increase in finance costs.

- Elevated operating expenses.

- Margin pressure despite steady volume demand.

- Depreciation costs remained elevated due to infrastructure expansion.

Insight:

- Revenue growth did not fully convert into profit growth, indicating weaker margin realization during the quarter.

Segment insight

Business Summary:

IGL continues to benefit from strong urban gas distribution demand across Delhi NCR and adjoining regions, though profitability remains sensitive to gas sourcing economics and regulatory pricing structures.

Key Characteristics:

- Strong city gas distribution network.

- Stable demand profile.

- Infrastructure-heavy business model.

- Margin-sensitive earnings structure.

- Strong cash generation capability.

Earning quality check

Key Drivers:

- Strong operating cash flow generation of ₹1,935.58 crore.

- Low leverage profile maintained.

- Significant investments toward infrastructure and deposits.

- Healthy working capital management.

- Consistent profitability despite margin moderation.

Interpretations:

- The earnings quality remains strong because cash generation continues to support operations and expansion despite temporary profitability pressure.

balance sheet Analysis

- Total Assets: ₹17,028.36 crore

- Total Liabilities: ₹5,503.34 crore

Insight:

- The company maintains a strong balance sheet with low debt, high equity base, and healthy liquidity position, supporting long-term expansion plans.

key risks

- Gas allocation and pricing risk.

- Margin compression from higher sourcing costs.

- Regulatory intervention risk.

- Competitive intensity in CGD sector.

- Demand slowdown in industrial gas consumption.

- Capex execution and infrastructure expansion risks.

management strategy signals

Focus Area:

- Expansion of CNG station infrastructure.

- Increasing PNG household penetration.

- Long-term infrastructure investment.

- Operational efficiency enhancement.

- Maintaining balance sheet strength.

- Expanding customer network across licensed geographical areas.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹4,684.78 Crore | +2.33% | +5.72% |

| PBT | ₹446.60 Crore | -11.24% | -20.35% |

| PAT | ₹338.75 Crore | -13.59% | -25.25% |

Indraprastha Gas Limited delivered stable operational growth in Q4 FY26, but profitability weakened materially due to pressure on operating spreads and rising gas sourcing costs. Despite near-term earnings pressure, the company continues to maintain strong fundamentals with robust cash flows, low leverage, healthy balance sheet quality, and long-term structural demand support from the city gas distribution sector.

Official Exchange Filing: Indraprastha Gas Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED