Earnings Announcement & Strategic Expansion

Pitti Engineering Reports Strong FY26 Growth; Announces ₹290 Crore Greenfield Expansion

NSE

pitieng

BSE

513519

Pitti Engineering Limited reported steady FY26 financial performance with double-digit growth in revenue and EBITDA, supported by strong demand across value-added product segments. The company also announced an additional ₹290 crore greenfield capex plan to significantly expand casting and machined component capacity.

PRICE-SENSITIVE TRIGGER

Event: FY26 Financial Results and Greenfield Expansion Announcement

Type: Earnings Announcement & Strategic Expansion

Impact: Positive

Immediate Effect: Strong operational growth, improved margins, and announcement of a large expansion project strengthen long-term growth visibility for the company.

Key Metrics:

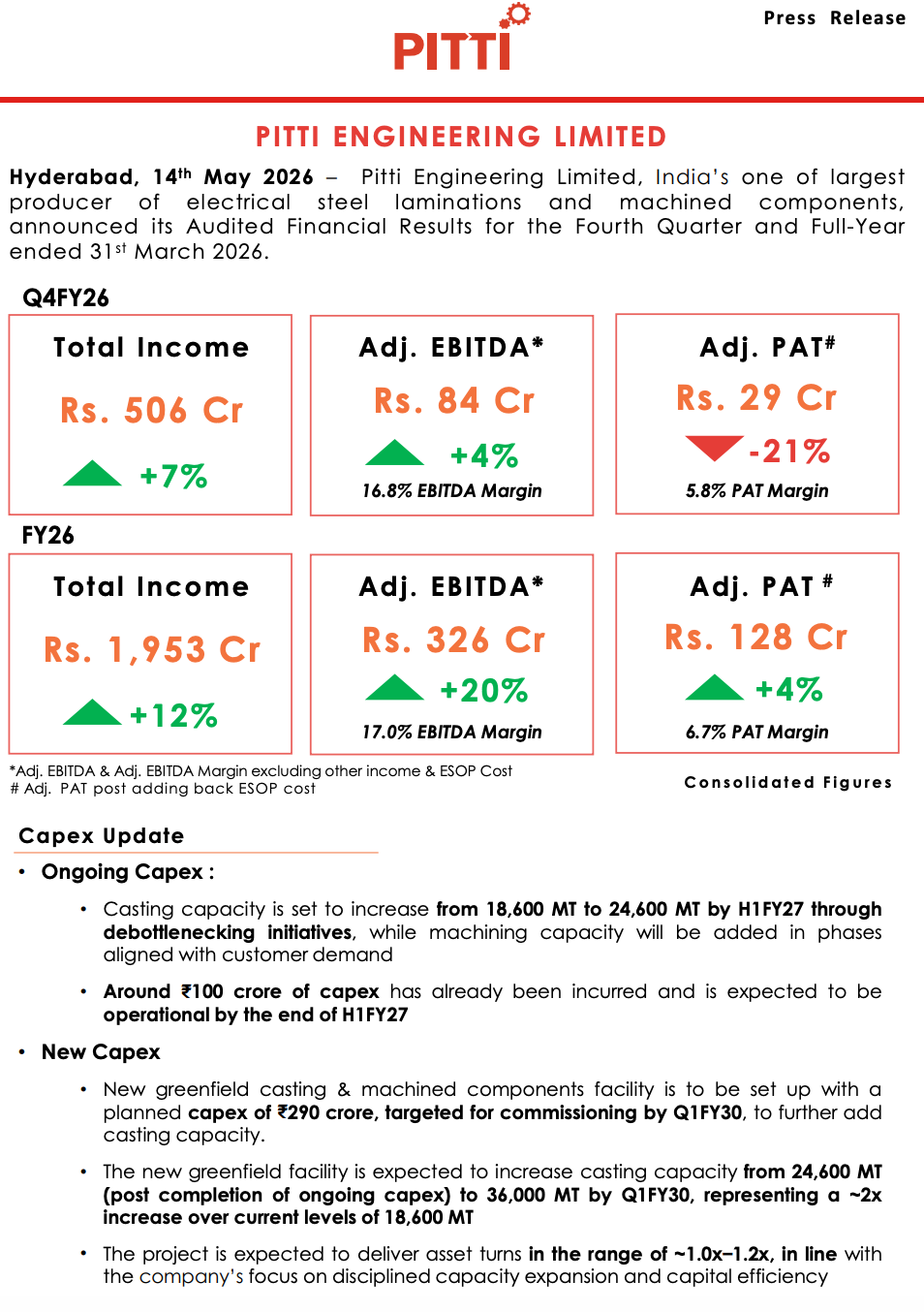

Q4 FY26 Highlights:

- Total Income: ₹506 crore, up 7% YoY

- Adjusted EBITDA: ₹84 crore, up 4% YoY

- Adjusted EBITDA Margin: 16.8%

- Adjusted PAT: ₹29 crore, down 21% YoY

- Adjusted PAT Margin: 5.8%

FY26 Highlights:

- Total Income: ₹1,953 crore, up 12% YoY

- Adjusted EBITDA: ₹326 crore, up 20% YoY

- Adjusted EBITDA Margin: 17.0%

- Adjusted PAT: ₹128 crore, up 4% YoY

- Adjusted PAT Margin: 6.7%

Capacity & Capex Highlight:

- Existing Casting Capacity: 18,600 MT per annum

- Capacity Expected by FY27: 24,600 MT through debottlenecking

- Target Capacity Post Greenfield Expansion: 36,000 MT per annum

- New Greenfield Capex: ₹290 crore

- Project Completion Timeline: Q1 FY30 target commissioning

- Current Capacity Utilization: Approximately 71%

Highlight:

- ₹290 Crore Additional Capex Approved for Greenfield Casting & Machined Components Facility

What Happened ?

Pitti Engineering Limited announced its audited Q4 FY26 and FY26 financial results, reporting healthy growth in revenue and profitability driven by robust demand from value-added product categories and industrial end-user sectors.

Alongside the earnings announcement, the company approved a ₹290 crore greenfield casting and machined components facility in Telangana to support future growth and rising customer demand.

key highlights

Financial Performance:

- FY26 revenue crossed ₹1,950 crore with 12% YoY growth.

- EBITDA increased 20% YoY to ₹326 crore with margin expansion to 17%.

- Demand remained strong from:

- Railways

- Power sector

- Industrial & mining

- Oil & gas

- Exports contributed around 27% of total revenue.

Capacity Expansion Plan:

- Ongoing debottlenecking initiatives are expected to increase casting capacity from 18,600 MT to 24,600 MT by H1FY27.

- Around ₹100 crore of existing capex has already been incurred.

- The newly approved greenfield facility will further increase total casting capacity to 36,000 MT annually.

- The project will be funded through:

- Internal accruals

- Lease finance

- Existing Hosakote facility may be monetized after commissioning of the new plant.

Product & Operational Trends:

- Strong Growth in Value-Added Assemblies

- High value-added laminations grew 14.7% YoY in Q4FY26.

- Rotor shaft integrated assemblies increased 43.4% YoY.

- Machined Components

- Overall machined components segment saw temporary moderation in quarterly volumes.

- Raw casting volumes remained healthy on a full-year basis.

Management Commentary:

- Management highlighted strong capacity utilization levels and sustained demand visibility.

- The company emphasized disciplined capital allocation and expansion into high-growth sectors such as:

- Renewable energy

- Data centers

- Industrial applications

Note:

- The greenfield expansion is expected to nearly double current casting capacity over the medium term and improve long-term operational scalability.

Risk Analysis

Key Risks:

- Delay in greenfield project commissioning.

- Industrial slowdown impacting OEM demand.

- Export market volatility due to geopolitical uncertainty.

- Margin pressure from commodity price fluctuations.

Worst Case Scenario:

- If demand weakens or expansion timelines are delayed, the expected return on the ₹290 crore investment may take longer to materialize.

Risk Level: Medium

Company Commentary

- Management stated that FY26 performance reflected strong demand across value-added product segments.

- The company highlighted improved operational efficiencies and margin expansion.

- Pitti Engineering believes the new capex will support long-term sustainable growth and enhance customer confidence.

- The company reiterated focus on disciplined execution, prudent capital allocation, and expansion into emerging industrial sectors.

Official Exchange Filing: Pitti Engineering Limited