Quarterly Earnings

Raghav Productivity Enhancers Reports Record Q1 FY27 Earnings with 68% Surge in PAT

NSE

rpel

BSE

539837

Raghav Productivity Enhancers Limited (RPEL) reported its highest-ever quarterly financial performance for Q1 FY27, driven by higher sales volumes, increasing contribution from value-added products, and expanding margins. Revenue grew 49% YoY to ₹87 crore, while EBITDA and PAT increased 62% and 68%, respectively. The company also maintained strong export momentum and confirmed that its brownfield expansion remains on track for commissioning in October 2026.

PRICE-SENSITIVE TRIGGER

Event: Q1 FY27 Financial Results and Business Update

Type: Quarterly Earnings

Impact: Positive

Immediate Effect: RPEL delivered record quarterly revenue, EBITDA, and PAT, supported by higher product realizations, volume growth, premium product mix, and improving operational efficiency. The company also reaffirmed its expansion roadmap and long-term growth strategy.

Financials:

Key Metrics:

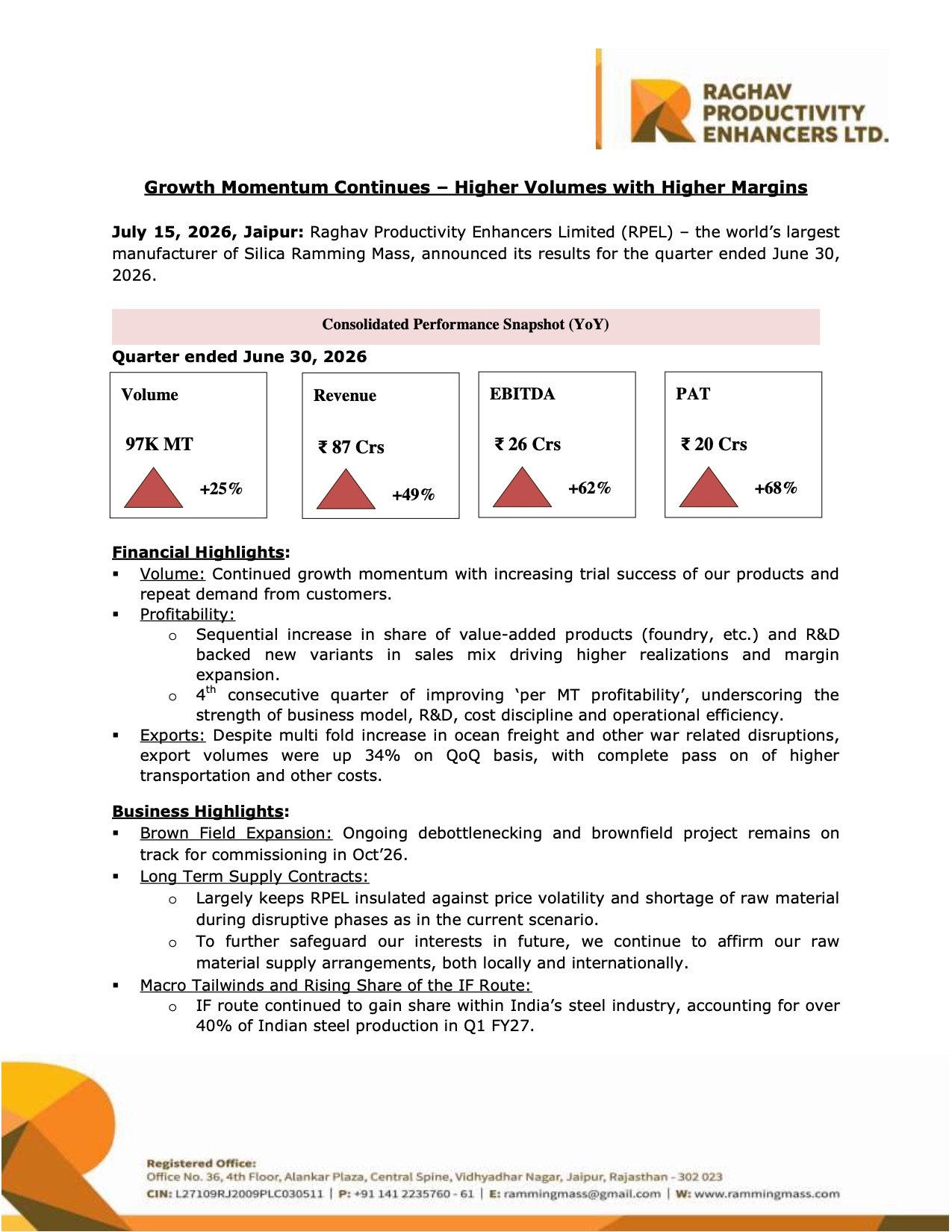

- Revenue: ₹87 crore (+49% YoY)

- EBITDA: ₹26 crore (+62% YoY)

- Profit After Tax (PAT): ₹20 crore (+68% YoY)

- Sales Volume: 97,000 MT (+25% YoY)

Highlight:

- RPEL reported its highest-ever quarterly Revenue, EBITDA, and PAT, with profitability growing faster than revenue for the fourth consecutive quarter of improving per-ton profitability.

What Happened ?

Raghav Productivity Enhancers Limited announced strong Q1 FY27 results, recording its best-ever quarterly financial performance. Growth was driven by higher sales volumes, increasing contribution from value-added products, and improved operational efficiencies.

The company also achieved robust export growth despite elevated ocean freight costs and geopolitical disruptions. In addition, management confirmed that the ongoing brownfield expansion project remains on schedule for commissioning in October 2026, which is expected to increase manufacturing capacity.

key details

Financial Performance:

- Revenue increased 49% YoY to ₹87 crore.

- EBITDA grew 62% YoY to ₹26 crore.

- PAT rose 68% YoY to ₹20 crore.

- Sales volume reached 97,000 MT, representing 25% YoY growth.

- The company achieved its fourth consecutive quarter of improvement in per-metric-ton profitability.

Business Performance:

- Higher contribution from value-added products, including foundry applications, improved overall realizations.

- Continued introduction of R&D-backed product variants supported margin expansion.

- Strong operational discipline and cost optimization contributed to profitability growth.

- Repeat customer demand and successful product trials continued to support volume growth.

Export Performance:

- Export volumes increased 34% QoQ despite sharp increases in ocean freight costs.

- The company successfully passed on higher transportation and logistics costs to customers.

- Export demand remained resilient despite geopolitical and shipping disruptions.

Capacity Expansion:

- Brownfield debottlenecking project remains on track.

- Commercial commissioning is expected in October 2026.

- Installed manufacturing capacity will increase from 414,000 MTPA to 534,000 MTPA after completion.

- Management is also evaluating multi-location manufacturing opportunities near major steel clusters as part of its long-term expansion strategy.

Industry Outlook:

- The Induction Furnace (IF) route accounted for more than 40% of India’s steel production during Q1 FY27.

- Government initiatives promoting green steel are expected to accelerate adoption of the IF route.

- Expanding DRI/sponge iron capacity across Africa and the Middle East continues to support long-term global demand for silica ramming mass.

Risk Analysis

Summary:

- RPEL continues to benefit from strong demand, premium product mix, and improving profitability. However, execution of expansion projects, export market conditions, and raw material availability remain important factors for sustaining growth.

Key Risks:

- Timely commissioning of the brownfield expansion project.

- Volatility in global freight and logistics costs.

- Dependence on continued demand from the steel and foundry industries.

- Raw material availability despite long-term supply agreements.

Worst Case:

- Any delay in capacity expansion, slowdown in steel production, or prolonged export disruptions could moderate volume growth and delay future earnings expansion.

Risk Level: Medium

Company Commentary

Managing Director Rajesh Kabra stated that the company began FY27 with its highest-ever quarterly Revenue, EBITDA, and PAT, with profitability continuing to outpace revenue growth.

- Increasing contribution from value-added and R&D-driven products.

- Brownfield expansion remains on schedule for October 2026 commissioning.

- Evaluation of additional manufacturing locations near key steel clusters.

- Long-term objective of expanding manufacturing capacity to 1 million MTPA and achieving 30% market sharein the silica ramming mass industry.

Official Exchange Filing: Raghav Productivity Enhancers Limited