Quarterly & Annual Financial Results

Sansera Engineering Reports Strong FY26 Growth with 51% Jump in PAT and Record Annual Revenue

NSE

sansera

BSE

543358

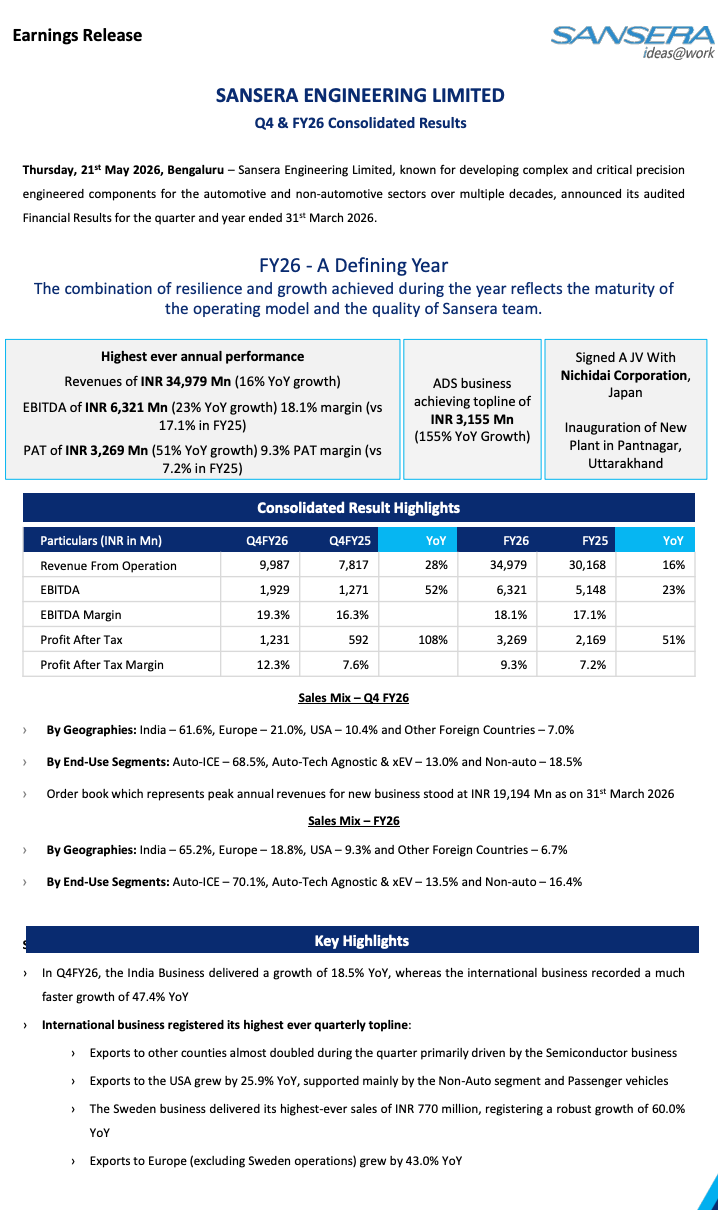

Sansera Engineering Limited announced its audited Q4 and FY26 consolidated financial results, reporting its highest-ever annual revenue of ₹3,497.9 crore and PAT of ₹326.9 crore. The company delivered strong growth across automotive and non-automotive businesses while expanding its international presence and semiconductor-related exports.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Consolidated Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company reported robust revenue growth, margin expansion, record international topline, and strong profitability growth, supported by diversification into semiconductor, non-auto, and EV-linked businesses.

Key Metrics:

- FY26 Revenue from Operations: ₹3,497.9 crore

- FY25 Revenue from Operations: ₹3,016.8 crore

- FY26 Revenue Growth: 16% YoY

- FY26 EBITDA: ₹632.1 crore

- FY26 EBITDA Growth: 23% YoY

- FY26 EBITDA Margin: 18.1%

- FY25 EBITDA Margin: 17.1%

- FY26 PAT: ₹326.9 crore

- FY26 PAT Growth: 51% YoY

- FY26 PAT Margin: 9.3%

- FY25 PAT Margin: 7.2%

- Q4 FY26 Revenue: ₹998.7 crore

- Q4 FY26 EBITDA: ₹192.9 crore

- Q4 FY26 EBITDA Margin: 19.3%

- Q4 FY26 PAT: ₹123.1 crore

- Q4 FY26 PAT Growth: 108% YoY

- ADS Business Topline: ₹315.5 crore

- Order Book Peak Annual Revenue Potential: ₹1,919.4 crore

Highlight Metric:

- Sansera Engineering delivered its highest-ever annual revenue of ₹3,497.9 crore with PAT growing 51% YoY to ₹326.9 crore during FY26.

What Happened ?

Sansera Engineering Limited announced its audited consolidated financial results for Q4 and FY26, showcasing strong growth across revenue, EBITDA, and profitability metrics.

The company reported FY26 revenue from operations of ₹3,497.9 crore, reflecting a 16% YoY increase, while EBITDA rose 23% YoY to ₹632.1 crore with margin expansion to 18.1%. Profit after tax surged 51% YoY to ₹326.9 crore. In Q4 FY26, revenue grew 28% YoY to ₹998.7 crore, while PAT more than doubled to ₹123.1 crore.

Sansera highlighted that FY26 was a defining year driven by resilience, operational maturity, and diversification across automotive, semiconductor, EV, and non-auto sectors. The company also signed a joint venture with Nichidai Corporation, Japan, and inaugurated a new manufacturing plant in Pantnagar, Uttarakhand.

International business delivered strong momentum during Q4 FY26, especially exports to semiconductor-linked markets and Europe. The Sweden business achieved its highest-ever quarterly sales at ₹77 crore with 60% YoY growth.

The ADS business achieved topline revenue of ₹315.5 crore during FY26, registering 155% YoY growth, further strengthening the company’s diversification strategy.

Key Details

FY26 Operational & Financial Performance Highlights:

- FY26 revenue from operations increased 16% YoY to ₹3,497.9 crore.

- FY26 EBITDA rose 23% YoY to ₹632.1 crore.

- EBITDA margin improved to 18.1% from 17.1% in FY25.

- FY26 PAT increased 51% YoY to ₹326.9 crore.

- PAT margin improved to 9.3% compared to 7.2% in FY25.

- Q4 FY26 revenue grew 28% YoY to ₹998.7 crore.

- Q4 FY26 EBITDA increased 52% YoY to ₹192.9 crore.

- Q4 FY26 PAT jumped 108% YoY to ₹123.1 crore.

- ADS business recorded revenue of ₹315.5 crore with 155% YoY growth.

- India business delivered 18.5% YoY growth during Q4 FY26.

- International business recorded 47.4% YoY growth in Q4 FY26.

- Exports to semiconductor-driven markets increased significantly during the quarter.

- Exports to the USA grew 25.9% YoY.

- Sweden operations achieved highest-ever quarterly sales of ₹77 crore with 60% YoY growth.

- Exports to Europe excluding Sweden operations grew 43% YoY.

- Auto-ICE segment contributed 70.1% of FY26 sales mix.

- Auto-Tech Agnostic & xEV segment contributed 13.5%.

- Non-auto segment contributed 16.4% of FY26 sales mix.

- Order book annualized revenue potential stood at ₹1,919.4 crore as of March 31, 2026.

- The company signed a JV with Nichidai Corporation, Japan.

- A new manufacturing facility was inaugurated in Pantnagar, Uttarakhand.

Note:

- Management stated that FY26 reflects the maturity of Sansera’s operating model and successful diversification into non-auto, EV, semiconductor, and global export-oriented businesses.

Risk Analysis

Summary:

- Despite strong operational performance, Sansera remains exposed to cyclical automotive demand, export market fluctuations, semiconductor sector dependency, and global macroeconomic risks.

Key Risks:

- Auto-ICE business still contributes over 70% of total sales mix.

- Export growth remains vulnerable to global economic slowdown and currency volatility.

- Semiconductor-linked demand may fluctuate depending on global chip industry cycles.

- Margin pressure may emerge from commodity inflation or supply-chain disruptions.

- Expansion into new facilities and joint ventures may involve execution risks.

- Dependence on overseas markets increases geopolitical and regulatory exposure.

- EV transition uncertainty may affect traditional automotive component demand over time.

Worst Case Scenario:

- A slowdown in global automotive demand, semiconductor weakness, or export disruptions could impact revenue growth, margins, and order inflows, especially across international operations.

Risk Level: Medium

Company Commentary

- Management described FY26 as a defining year for the company.

- The company stated that resilience and operational maturity drove strong performance during FY26.

- Sansera highlighted its highest-ever annual revenue and profitability performance.

- International business recorded its highest-ever quarterly topline during Q4 FY26.

- The company emphasized growth in semiconductor, non-auto, and EV-linked segments.

- Management highlighted strong export growth across the USA and European markets.

- Sansera stated that the new JV with Nichidai Corporation and the Pantnagar plant strengthen future growth capabilities.

Official Exchange Filing: Sansera Engineering Limited