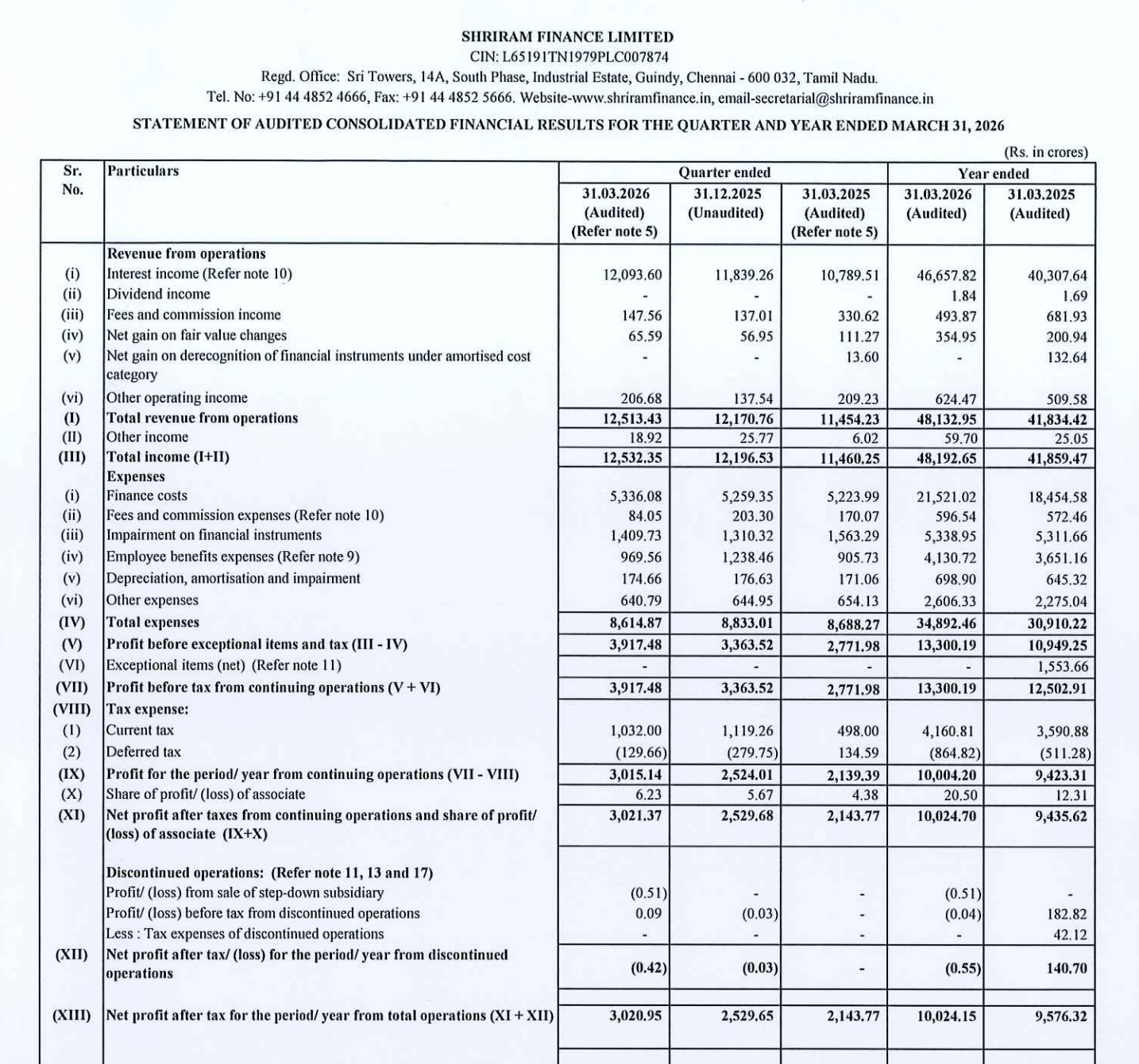

Quarter Ended: March 2026

Shriram Finance Ltd – Q4 FY26 Financial Results Analysis

NSE

shriramfin

BSE

511218

The company delivered strong YoY and QoQ growth supported by robust loan book expansion and steady margins despite high credit costs.

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹12,513.43 Cr

- QoQ Change: +2.81%

- YoY Change: +9.25%

- Previous Quarter (Q3 FY26): ₹12,170.76 Cr

- Previous Year (Q4 FY25): ₹11,454.23 Cr

- Total Income (Q4 FY26): ₹12,513.43 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹3,020.95 Cr

- QoQ Change: +19.42%

- YoY Change: +40.93%

- Previous Quarter (Q3 FY26): ₹2,529.65 Cr

- Previous Year (Q4 FY25): ₹2,143.77 Cr

- PAT (Q4 FY26): ₹3,020.95 Cr

- QoQ Performance

- Revenue Trend: Stable growth

- Profit Trend: Strong growth

Margin Analysis

Key Drivers:

- Strong growth in interest income

- Controlled operating expenses

- Stable finance cost structure

- High credit cost (impairment on financial instruments)

Key Signal: Margins remain stable with slight expansion driven by operating efficiency, though credit costs remain elevated.

Earning quality check

Drivers:

- Core lending-driven income growth

- High impairment charges (₹1,409 Cr)

- Strong cash inflows from interest income

- No dependency on exceptional gains

Interpretation:

- Earnings quality is strong but partially moderated by elevated credit costs typical of NBFC cycles

balance sheet Analysis

- Total Assets: ₹3,21,374.52 Cr

- Total Liabilities: ₹2,55,455.93 Cr

Insight:

- Strong balance sheet supported by large loan book expansion and diversified funding sources

key risks

- High credit cost / asset quality pressure

- Dependency on borrowing markets

- Interest rate sensitivity

- Regulatory risks in NBFC sector

management strategy signals

- Focus Areas:

- Loan book expansion

- Maintaining asset quality

- Diversifying funding sources

- Improving operational efficiency

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹12,532.35 Cr | +2.75% | +9.36% |

| PBT | ₹3,917.48 Cr | +16.44% | +41.30% |

| PAT | ₹3,020.95 Cr | +19.42% | +40.93% |

Shriram Finance delivered a strong quarter with solid growth in revenue and profitability. The company continues to benefit from loan book expansion and operational efficiency. However, elevated credit costs remain a key monitorable. Overall, the performance reflects a healthy growth trajectory within the NBFC space.

Official Exchange Filing: Shriram Finance Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

69%

NET PROFIT AS % OF REVENUE

24.14%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED