Earnings Release

Skipper Delivers Record FY26; Revenue Crosses ₹5,552 Cr with Strong Margin Expansion

NSE

skipper

BSE

538562

Skipper Limited reported its strongest-ever financial performance, with record revenue, profit growth, and margin expansion, backed by strong EPC execution and global order momentum.

PRICE-SENSITIVE TRIGGER

Event: Q4 & FY26 Result Announcement

Type: Earnings Release

Impact: Strong Positive

Immediate Effect: Record performance + strong order visibility

Key Metrics:

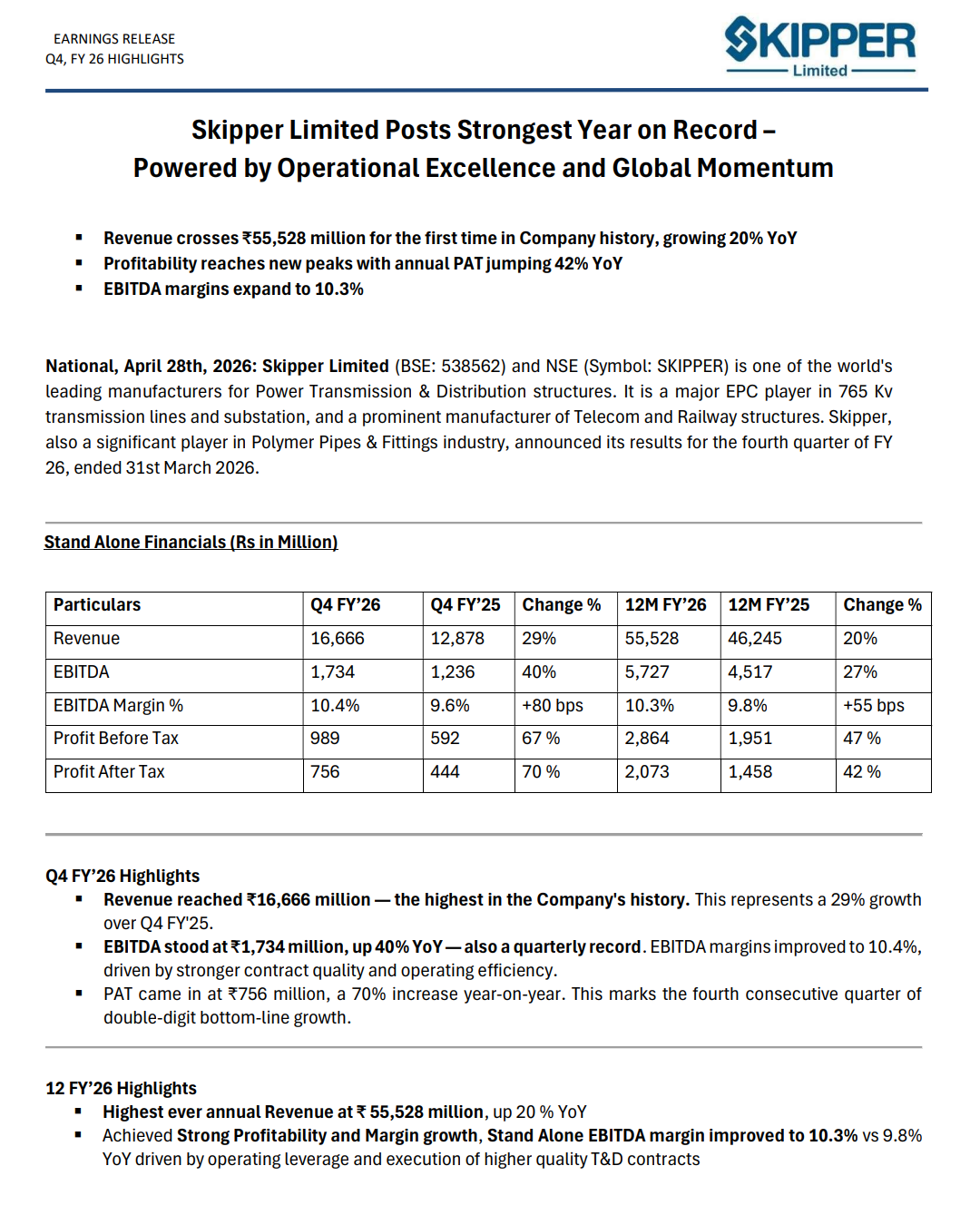

Q4 FY26:

- Revenue → ₹1,666.6 Cr (+29% YoY)

- EBITDA → ₹173.4 Cr (+40% YoY)

- EBITDA Margin → 10.4%

- PAT → ₹75.6 Cr (+70% YoY)

FY26:

- Revenue → ₹5,552.8 Cr (+20% YoY)

- EBITDA → ₹572.7 Cr (+27% YoY)

- EBITDA Margin → 10.3%

- PAT → ₹207.3 Cr (+42% YoY)

- PBT → ₹286.4 Cr (+47% YoY)

Order Book & Pipeline:

- Order Book → ₹8,502 Cr (highest ever)

- FY26 Order Inflow → ₹5,678 Cr

- Bidding Pipeline → ₹33,000 Cr

Highlight:

- Record all-time high revenue and profitability across all levels

- Strong operating leverage → margin expansion to 10%+

- Massive ₹33,000 Cr bidding pipeline ensures future growth visibility

- Order book at record levels → multi-year revenue visibility

- Global expansion traction (North America + LATAM entry)

What Happened ?

The company reported strong quarterly and annual performance, driven by operational efficiency, EPC execution strength, and robust order inflows.

key highlights

Performance Drivers:

- Operational excellence & execution discipline

- Strong EPC segment growth

- Margin expansion due to better contract mix

- Increasing global footprint

Order Book Strength:

- Highest-ever closing order book

- Strong domestic (90%) + export mix

- Continuous large EPC wins

Business Expansion:

- Entry into North America with largest-ever order

- LATAM expansion via Brazil subsidiary

- UAE & USA subsidiaries nearing execution

Operational Milestone:

- Execution of ~5,000 circuit km transmission lines

- Commissioned 765 kV projects worth ₹1,500 Cr

- Capacity expansion toward 450,000 MTPA

Risk Analysis

Key Risks

- EPC execution delays

- Raw material price volatility

- Export market dependency

- Working capital intensity

Risk Level: Medium

Company Commentary

- FY26 marked highest-ever revenue and profitability

- EBITDA margins improved due to operational efficiency

- Strong order book ensures future revenue visibility

- Global expansion gaining traction across regions

- Focus remains on long-term value creation and execution

Official Exchange Filing: Skipper Limited