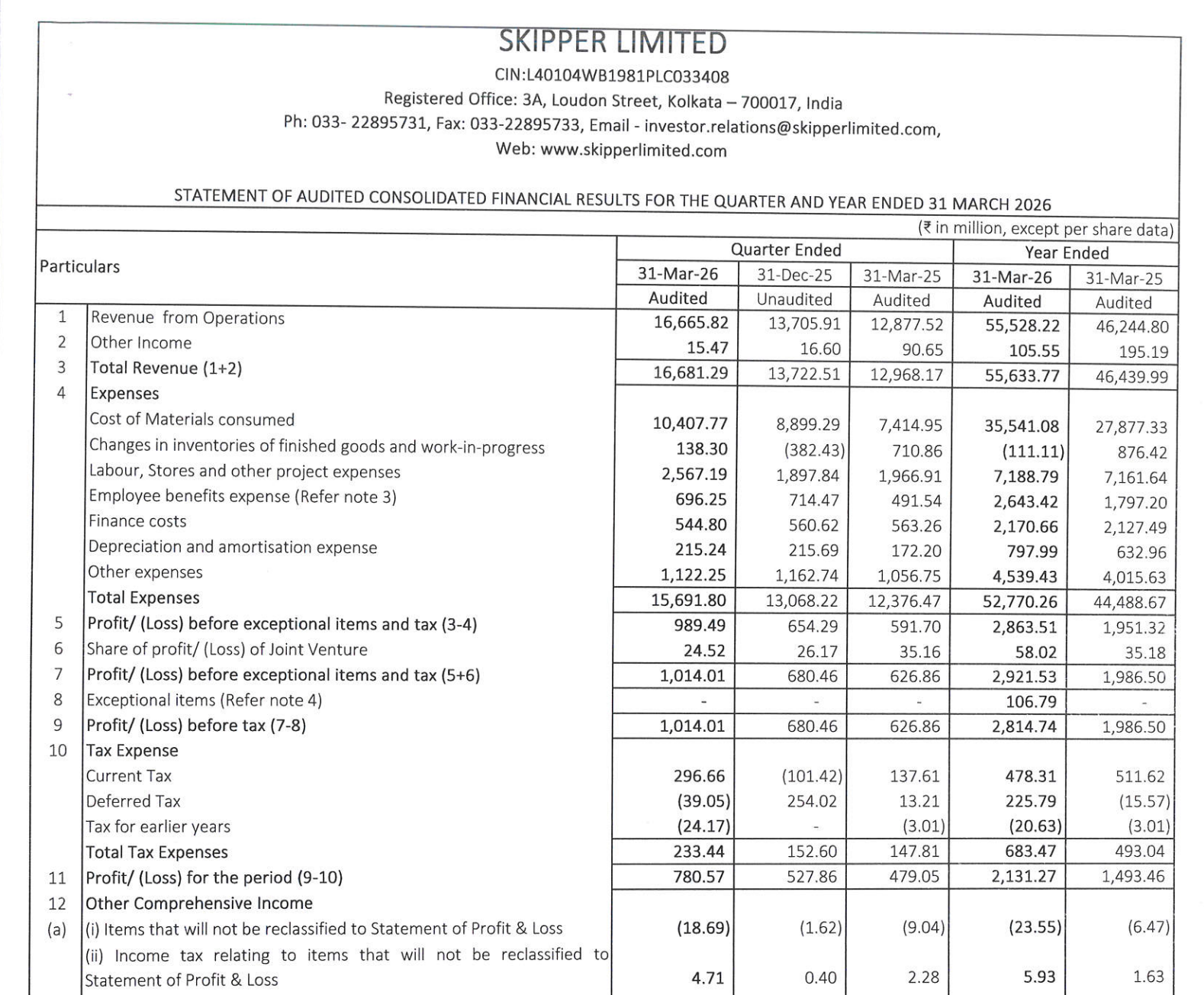

Quarter Ended: March 2026

Skipper Limited – Q4 FY26 Results

NSE

skipper

BSE

538562

Skipper delivered solid top-line growth driven by Engineering and Infra segments, but margin pressure and rising finance costs limited profit expansion

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹16,665.82 million

- QoQ Change: +21.6%

- YoY Change: +29.4%

- Previous Quarter (Q3 FY26): ₹13,705.91 million

- Previous Year (Q4 FY25): ₹12,877.52 million

- Revenue (Q4 FY26): ₹16,665.82 million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹780.57 million

- QoQ Change: +9.0%

- YoY Change: +53.7%

- Previous Quarter (Q3 FY26): ₹527.86 million

- Previous Year (Q4 FY25): ₹479.05 million

- PAT (Q4 FY26): ₹780.57 million

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Strong Recovery

Margin Analysis

Key Drivers:

- Increase in raw material consumption (steel-heavy business impact)

- Higher finance costs due to increased borrowings

- Operating leverage benefits partially offset cost pressures

Key Signal: Revenue growth is strong, but margin expansion is constrained due to cost structure

Segment performance

Segment: Engineering Products

Revenue: ₹12,487.38 Mn

Insights:

- Major contributor (~75% of revenue)

- Strong YoY and QoQ growth

- Core driver of profitability

Segment: Polymer Products

Revenue: ₹1,599.82 Mn

Insights:

- Moderate growth segment

- Lower margin compared to engineering

Segment: Infrastructure Projects

Revenue: ₹2,578.62 Cr

Insights:

- Stable contribution

- Growth driven by project execution

Segment insight

Summary:

- Engineering segment dominates revenue and profitability, indicating strong positioning in transmission & distribution infrastructure

Characteristics:

- High dependence on engineering segment

- Diversified but engineering-led business model

- Infra projects add execution-based volatility

Earning quality check

Drivers:

- Growth supported by core operations (not one-off gains)

- Limited exceptional items

- High finance cost impacting net profitability

Interpretation:

- Earnings are operationally driven but slightly pressured by leverage and cost factors

balance sheet Analysis

- Total Assets: ₹45,333.04 million

- Total Liabilities: ₹30,420.75 million

Insight:

- Significant increase in borrowings indicates expansion phase

- Working capital intensity remains high

- Balance sheet is leveraged but aligned with growth strategy

key risks

- High dependence on steel prices (raw material volatility)

- Rising debt and finance cost burden

- Working capital-intensive business

- Execution risk in infrastructure projects

management strategy signals

Focus Area:

- Expansion in engineering and infrastructure segments

- Scaling export opportunities

- Capacity expansion and project execution

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹16,681.29 Million | +21.6% | +28.6% |

| PBT | ₹1,014.01 Million | +49.1% | +61.7% |

| PAT | ₹780.57 Million | +47.9% | +62.9% |

Skipper Limited is in a strong growth phase, driven by robust demand in engineering and infrastructure. However, margin pressure and rising leverage are key concerns. The company remains fundamentally strong, but sustainability of margins and debt management will be critical going forward.

Official Exchange Filing: Skipper Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED