Quarterly & Annual Financial Results

Stallion India Fluorochemicals Reports Strong FY26 Performance Driven by Operational Resilience

NSE

stallion

BSE

544342

Stallion India Fluorochemicals Limited reported strong FY26 financial performance supported by operational resilience, supply-chain preparedness, and expanding specialty gas infrastructure. The company posted double-digit growth across revenue, EBITDA, PAT, and EPS while maintaining its expansion roadmap for the upcoming R-32 manufacturing facility in Rajasthan.

PRICE-SENSITIVE TRIGGER

Event: FY26 audited financial results announcement along with operational and expansion update.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The results indicate strong profitability growth, margin expansion, and continued progress on strategic manufacturing expansion plans.

Key Metrics:

FY26 Financial Performance:

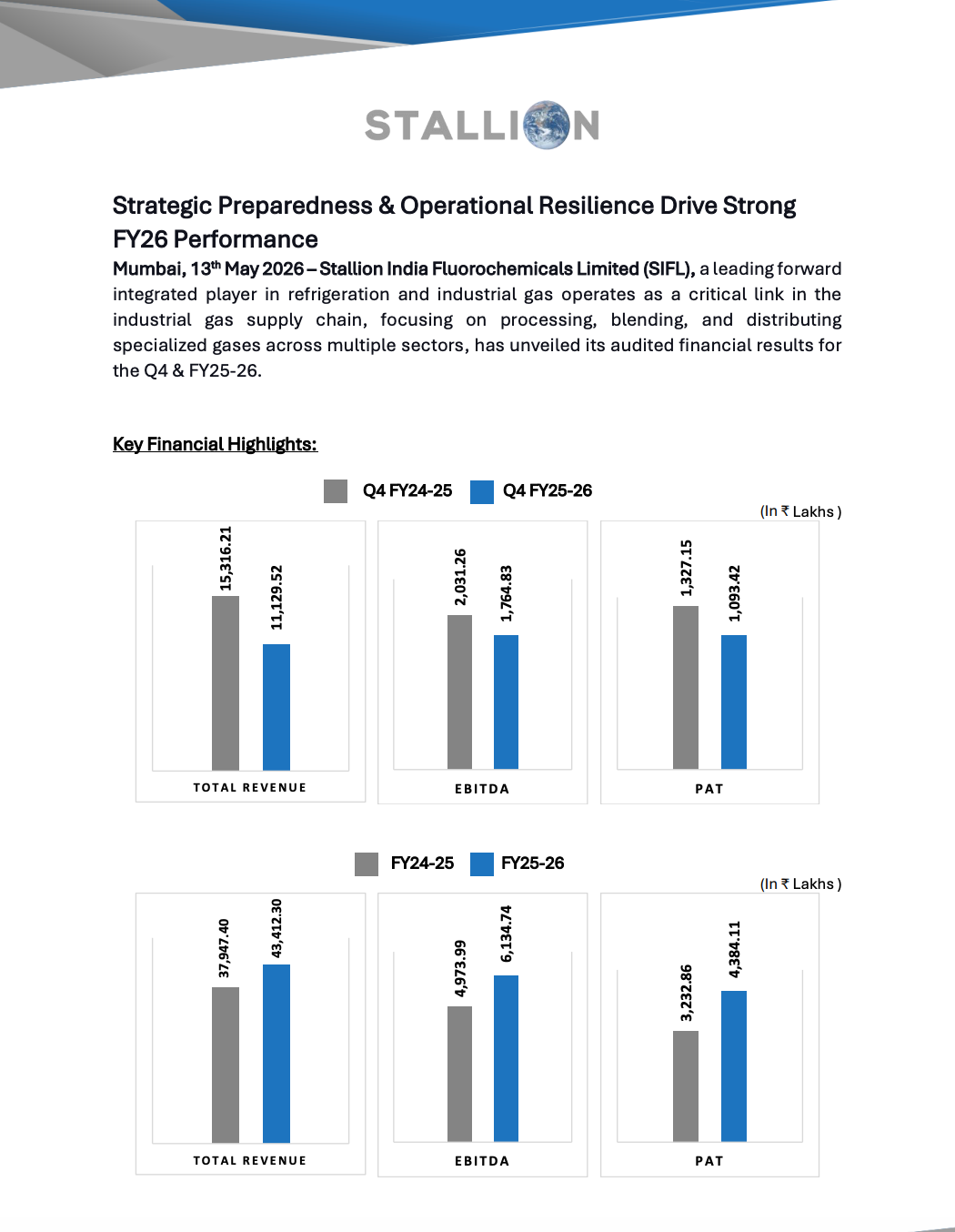

- Total Revenue increased to ₹434.12 crore, up 14.40% YoY

- EBITDA rose to ₹61.35 crore, up 23.34% YoY

- Profit After Tax (PAT) increased to ₹43.84 crore, up 35.61% YoY

- EPS improved to ₹5.34 from ₹4.38

Q4 FY26 Financial Performance:

- Q4 Revenue stood at ₹153.16 crore

- Q4 EBITDA came in at ₹20.31 crore

- Q4 PAT reported at ₹13.27 crore

Highlight Metric:

- PAT surged 35.61% YoY in FY26

What Happened ?

Stallion India Fluorochemicals Limited announced its audited Q4 and FY26 financial results, highlighting resilient operational execution despite global supply-chain disruptions and volatility in energy markets.

The company stated that proactive inventory planning, diversified sourcing arrangements, and operational contingency mechanisms helped maintain supply continuity across customer industries.

Management also reaffirmed that the proposed 10,000 MT R-32 manufacturing facility at Bhilwara, Rajasthan remains on track for commissioning by October 2026.

key highlights

Operational & Strategic Updates:

- Company achieved targeted topline guidance of approximately ₹430 crore

- R-32 manufacturing facility already received environmental clearance

- Manufacturing project supports backward integration and import substitution

- Expansion underway in specialty gases, semiconductor gases, helium, and HFO infrastructure

- Management targets revenue CAGR of 30–35% over the next three years

- Margin improvement guidance of 3–4% over medium term

Note:

- The company emphasized that strengthening backward integration and specialty gas capabilities are expected to support long-term scalability and profitability.

Business Overview:

- Stallion India Fluorochemicals operates across refrigeration and industrial gas segments

- Company serves industries including pharmaceuticals, semiconductors, refrigeration, automotive, and fire-fighting

- Manufacturing facilities located at Khalapur, Ghiloth, Manesar, and Panvel

- Business model focuses on processing, blending, and distribution of industrial gases

Risk Analysis

Key Risks:

- Rising energy and logistics costs may impact margins

- Global geopolitical tensions can disrupt supply chains

- Execution delays in the R-32 project may affect growth plans

- Industrial demand slowdown could impact gas consumption volumes

Worst Case Scenario:

- Extended supply-chain disruptions or delays in expansion projects may pressure profitability and postpone targeted growth trajectory.

Risk Level: Medium

Company Commentary

- Management highlighted resilient performance despite external market volatility

- Company maintained supply continuity through proactive sourcing and inventory management

- R-32 manufacturing facility remains on track for October 2026 commencement

- Specialty gases and semiconductor gas infrastructure continue to expand

- Management expects strategic initiatives to support long-term revenue and margin growth

Official Exchange Filing: Stallion India Fluorochemicals Limited