Quarterly Performances

Tata Motors Reports Strong Growth in Commercial Vehicle Production and Domestic Sales for Q1 FY27

NSE

tatamotors

BSE

500570

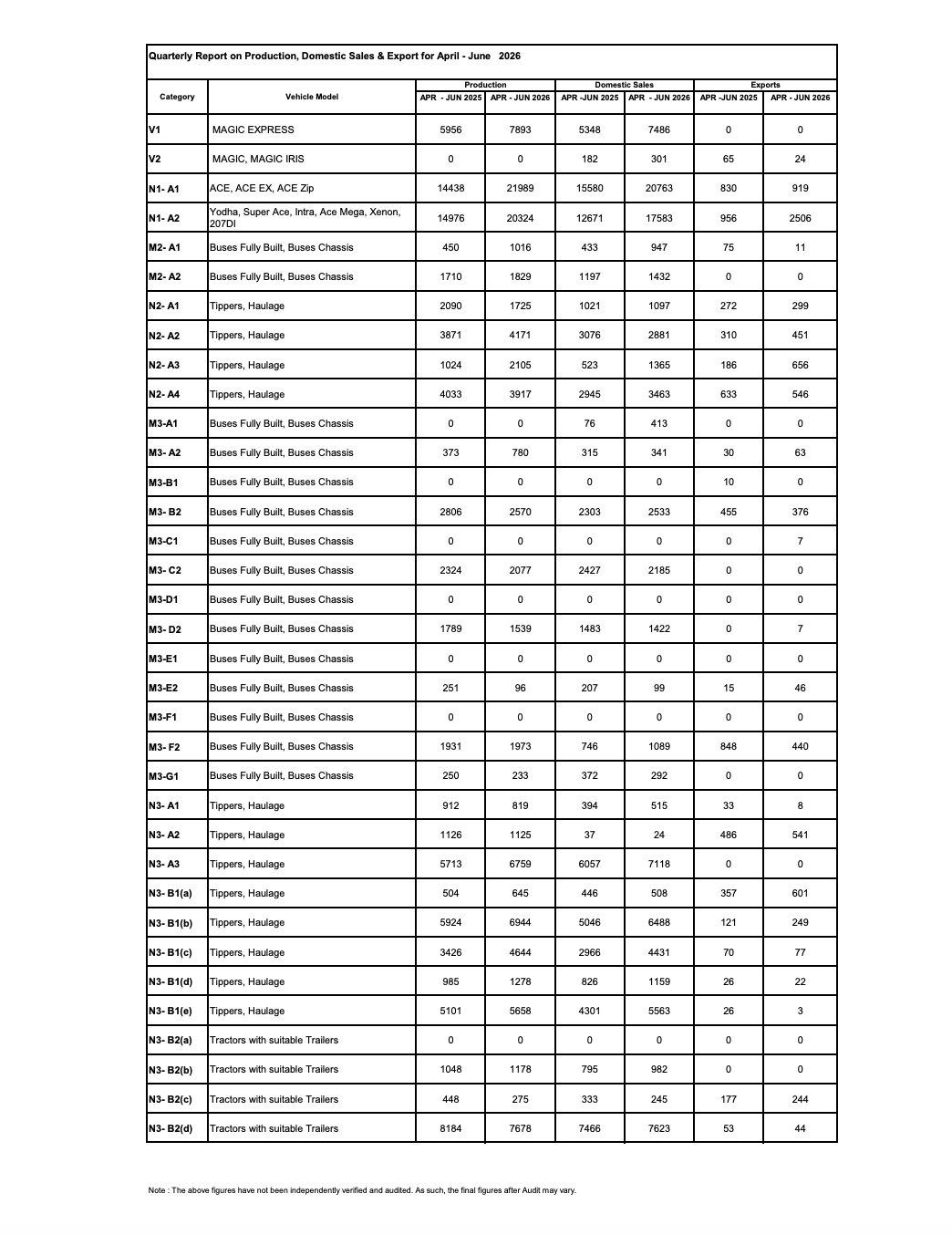

Tata Motors Limited released its SIAM report for April–June 2026, reporting healthy year-on-year growth in commercial vehicle production and domestic sales across several vehicle categories, led by light commercial vehicles and selected heavy truck segments.

PRICE-SENSITIVE TRIGGER

Event: Quarterly SIAM Production, Domestic Sales & Export Report (April–June 2026)

Type: Quarterly Performances

Impact: Positive

Immediate Effect: The quarterly operational update indicates improved production and domestic demand across key commercial vehicle segments, reflecting healthy business momentum during Q1 FY27.

Key Metrics:

- Production: Increased across several LCV and M&HCV categories.

- Domestic Sales: Strong growth in light commercial vehicles and selected heavy truck segments.

- Exports: Mixed performance across different product categories.

Highlight:

- The strongest operational growth was recorded in the ACE range, Magic Express, and multiple heavy truck categories during the quarter.

What Happened ?

Tata Motors submitted its SIAM operational report for April–June 2026, detailing production, domestic sales and export volumes for its commercial vehicle portfolio. The report reflects broad-based growth in domestic operations, supported by higher production across several vehicle categories.

Key Details

Key Developments:

- Magic Express production increased to 7,893 units from 5,956 units.

- ACE product family production rose to 21,989 units from 14,438 units.

- Yodha, Super Ace and Intra range production increased to 20,324 units from 14,976 units.

- Several heavy truck (N3) categories reported higher production and domestic sales compared with the previous year.

- Export performance remained mixed, with gains in selected segments and moderation in others.

Note:

- The SIAM figures are provisional and have not been independently audited. Final audited numbers may vary.

Risk Analysis

Summary:

- While domestic commercial vehicle demand remained healthy, export performance continued to vary across product segments.

Key Risks:

- Demand fluctuations in commercial vehicle markets.

- Export market volatility.

- Changes in freight, infrastructure and industrial activity.

Worst Case:

- A slowdown in commercial vehicle demand or weaker exports could affect production growth in upcoming quarters.

Risk Level: Medium

Company Commentary

- The company submitted its quarterly SIAM production, domestic sales and export report to the stock exchanges in compliance with SEBI Listing Regulations.

Official Exchange Filing: Tata Motors Limited