Quarterly & Annual Financial Results

TeamLease Services Reports Strong FY26 Performance; PAT Rises 33% YoY, Announces ₹238 Crore Buyback

NSE

TEAMLEASE

BSE

539658

TeamLease Services Limited reported a strong FY26 performance with consolidated PAT rising 33% YoY to ₹147.1 crore and EBITDA growing 14% YoY to ₹158 crore. The company also announced a ₹238 crore share buyback backed by strong cash generation and improved operating leverage.

PRICE-SENSITIVE TRIGGER

Event: Announcement of audited Q4FY26 and FY26 consolidated financial results along with buyback approval

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong profitability growth, improved margins, healthy cash position, and buyback announcement are expected to strengthen investor sentiment.

Key Metrics:

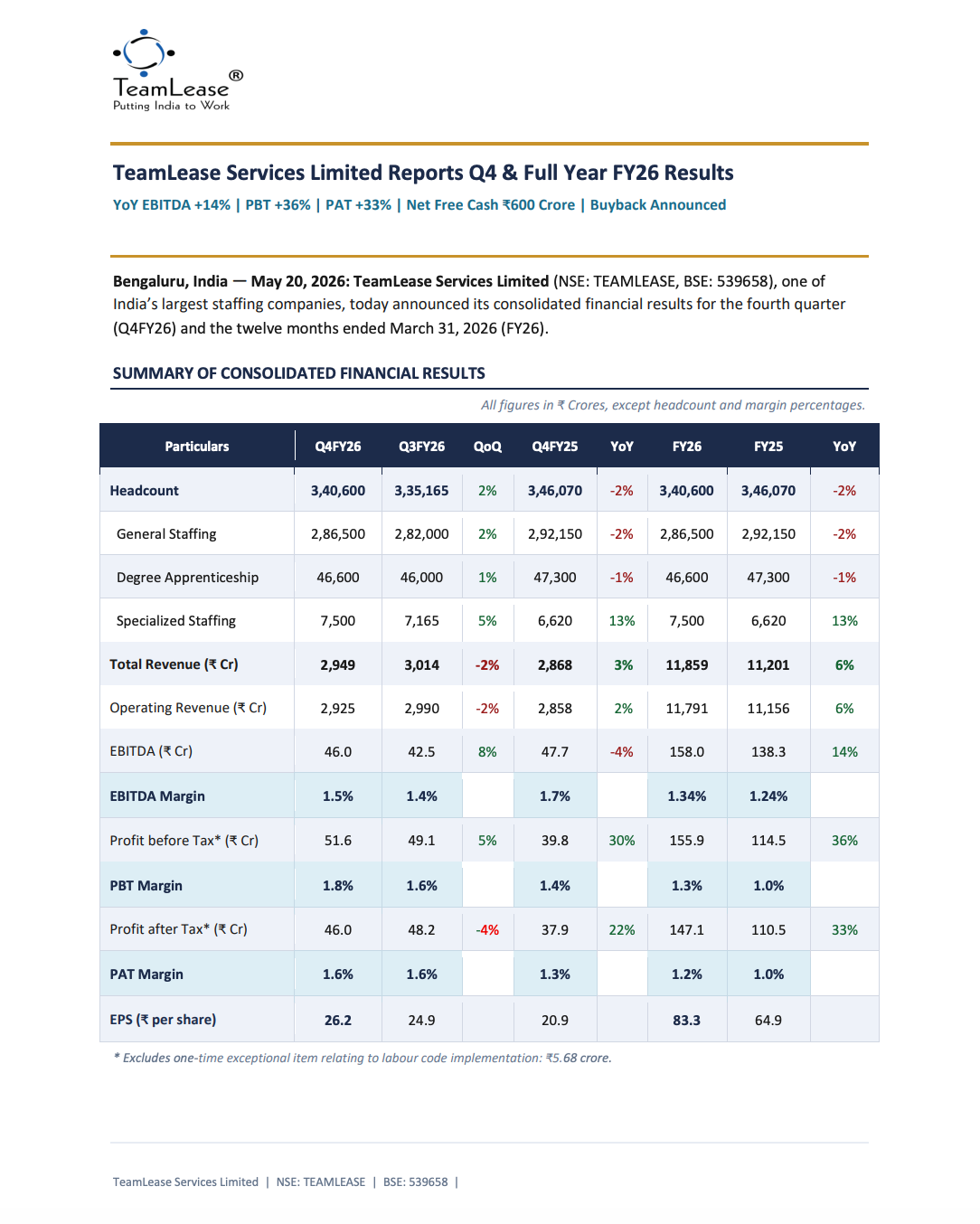

- FY26 Total Revenue: ₹11,859 Crore (+6% YoY)

- FY26 Operating Revenue: ₹11,791 Crore (+6% YoY)

- FY26 EBITDA: ₹158 Crore (+14% YoY)

- FY26 Profit Before Tax (PBT): ₹155.9 Crore (+36% YoY)

- FY26 Profit After Tax (PAT): ₹147.1 Crore (+33% YoY)

- FY26 EPS: ₹83.3 per share

- Net Free Cash: ₹600 Crore

- Buyback Size: ₹238 Crore

Highlight Metric:

- FY26 PAT Growth: +33% YoY to ₹147.1 Crore

What Happened ?

TeamLease Services Limited announced its audited consolidated financial results for Q4FY26 and FY26, reporting steady revenue growth and strong improvement in profitability metrics.

The company posted FY26 consolidated revenue of ₹11,859 crore, up 6% YoY, while EBITDA increased 14% YoY to ₹158 crore. Profit before tax rose 36% YoY to ₹155.9 crore, and PAT climbed 33% YoY to ₹147.1 crore.

The company highlighted improving operating leverage, disciplined cost management, and strong growth across HR Services and Specialized Staffing businesses. During the year, TeamLease also strengthened its liquidity position with net free cash reaching ₹600 crore following receipt of income tax refunds.

Additionally, the Board approved a buyback proposal worth ₹238 crore.

Key Details

Operational & Business Highlights:

- EBITDA margins expanded by 10 basis points over FY25.

- Specialized Staffing revenue grew 13% YoY during FY26.

- HR Services revenue and EBITDA each grew 23% YoY.

- Around 109 new enterprise client logos were added during Q4FY26.

- Approximately 24% of associates hired during the quarter were first-time job seekers.

- The company added nearly 6,000 net headcount during the quarter.

- General Staffing business maintained receivable discipline with DSO at 6 days.

- GCC clients contributed over 67% of Specialized Staffing revenue.

- The company approved a buyback representing 8.87% of equity capital.

Note:

- The company stated that the buyback will be funded from existing free cash balances and remains subject to shareholder and regulatory approvals.

Risk Analysis

Key Risks:

- BFSI hiring demand remained softer compared to other sectors.

- Staffing businesses remain sensitive to economic slowdown and corporate hiring trends.

- Margin expansion remains dependent on maintaining operating leverage.

- Regulatory changes in labour and staffing sectors may impact future profitability.

Worst Case Scenario:

- A slowdown in hiring demand or pressure on staffing margins could affect revenue growth momentum and profitability in FY27.

Risk Level: Medium

Company Commentary

- Managing Director & CEO Suparna Mitra stated that FY26 reflected disciplined execution and improving operating leverage.

- Management highlighted focus on accelerating profitable growth and strengthening client relationships.

- The company emphasized strong momentum across HR Services, Degree Apprenticeship, and Specialized Staffing businesses.

- TeamLease reiterated its long-term focus on employment, employability, and workforce platform expansion.

Official Exchange Filing: TeamLease Services Limited

Given TeamLease’s impressive 33% YoY PAT growth and the announced ₹238 crore buyback for FY26, the company is clearly maximizing its operating leverage and cash generation. However, the risk analysis mentions that corporate hiring trends and macroeconomic shifts remain a key dependency. Since institutional investors look closely at capital allocation and risk diversification during such high-growth phases, how well-positioned is the company to maintain this momentum if the BFSI sector remains soft? On a related note regarding corporate structures and transparency in highly regulated markets, I was reading an analysis on how international operators manage compliance and risk at — does TeamLease face similar stringent regulatory compliance bottlenecks in its specialized staffing segments that could impact the projected FY27 margins?