Quarter Ended: March 2026

Vishal Mega Mart Limited – Q4 FY26 Results

NSE

vmm

BSE

544307

Vishal Mega Mart Limited reported healthy double-digit revenue growth in Q4 FY26, supported by strong retail demand and inventory expansion, although profitability moderated sequentially due to higher operating and finance costs.

key financial highlights

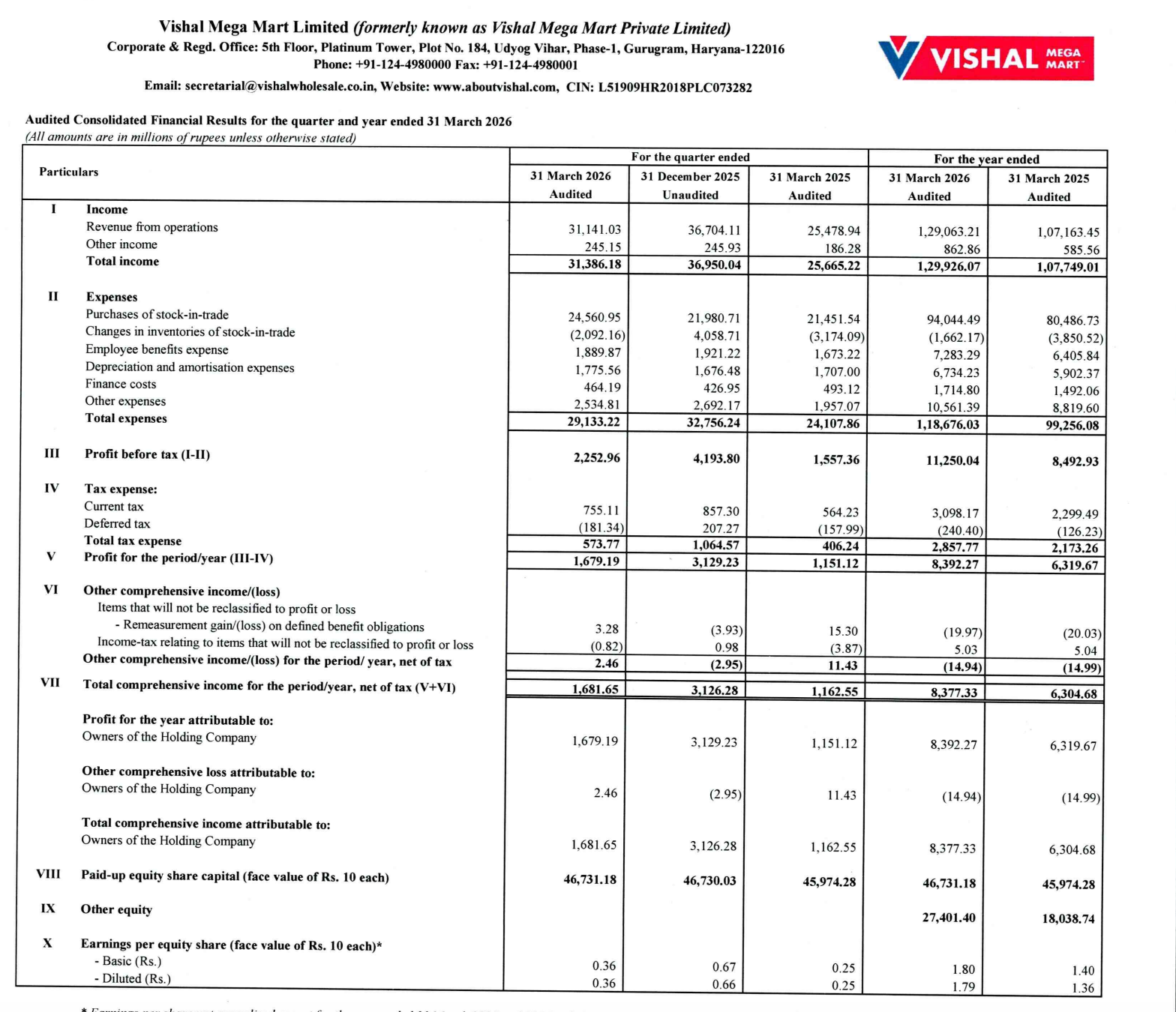

- Revenue from Operations:

- Revenue (Q4 FY26): ₹31,141.03 Million

- QoQ Change: -15.16%

- YoY Change: +22.23%

- Previous Quarter (Q3 FY26): ₹36,704.11 Million

- Previous Year (Q4 FY25): ₹25,478.94 Million

- Revenue (Q4 FY26): ₹31,141.03 Million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹1,679.19 Million

- QoQ Change: +46.34%

- YoY Change: +45.87%

- Previous Quarter (Q3 FY26): ₹3,129.23 Million

- Previous Year (Q4 FY25): ₹1,151.12 Million

- PAT (Q4 FY26): ₹1,679.19 Million

- QoQ Performance:

- Revenue Trend: Sequential moderation after festive-driven Q3

- Profit Trend: Sharp Sequential Decline

Margin Analysis

Drivers:

- Purchases of stock-in-trade increased significantly during the quarter.

- Employee benefit expenses remained elevated due to expansion activities.

- Finance costs increased YoY due to lease liabilities and scale expansion.

- Depreciation costs rose as store footprint and assets expanded.

- Inventory adjustments negatively impacted quarterly margins.

- Operating leverage weakened sequentially after the festive quarter.

Insight:

- Despite strong annual growth, margin pressure emerged in Q4 as operational expenses rose faster than sequential revenue growth.

Earning quality check

Key Drivers:

- Operating cash flow remained robust at ₹16,212.66 million.

- Cash generated from operations improved versus FY25.

- Investment activity increased substantially due to store expansion and investments.

- Strong improvement in cash balances year-on-year.

- Finance costs remained manageable relative to operating profit generation.

Interpretations:

- The company’s earnings quality remains healthy as profits are supported by strong operating cash flows and expanding retail operations despite near-term margin pressure.

balance sheet Analysis

- Total Assets: ₹1,14,494.28 million

- Total Liabilities: ₹40,361.70 million

Insight:

- The balance sheet strengthened materially with growth in inventories, investments, and cash balances, while equity expanded sharply through retained earnings and fresh capital infusion.

key risks

- Margin pressure from rising operating costs.

- Inventory management risk in value retail business.

- Seasonal demand fluctuations impacting quarterly profitability.

- Higher lease liabilities due to store expansion.

- Consumer spending slowdown may affect discretionary retail demand.

- Competitive intensity in organized retail sector.

management strategy signals

Focus Area:

- Expansion of retail store footprint.

- Strengthening value retail positioning.

- Inventory-led merchandising strategy.

- Improving operational efficiencies.

- Enhancing customer acquisition and repeat purchases.

- Maintaining strong cash generation profile.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹31,386.18 Million | -15.06% | +22.27% |

| PBT | ₹2,252.96 Million | -46.28% | +44.67% |

| PAT | ₹1,679.19 Million | -46.34% | +45.87% |

Vishal Mega Mart Limited delivered a healthy FY26 closing quarter with strong YoY growth in revenue and profits backed by continued retail expansion and robust operating cash generation.

However, sequential profitability softness and rising operational costs indicate that margin sustainability will remain a key monitorable factor as the company continues scaling its retail network.

Official Exchange Filing: Vishal Mega Mart Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED