Earnings Release

Waaree Energies Delivers Record FY26 Performance; Revenue Jumps 84% YoY, PAT Doubles

NSE

waareeener

BSE

544277

Waaree Energies Limited reported a record-breaking FY26 performance with revenue surging ~84% YoY to ₹26,536.77 crore and PAT rising ~101% YoY, driven by strong scale-up in production and operational efficiency

PRICE-SENSITIVE TRIGGER

Event: Q4 & FY26 Financial Results Announcement

Type: Earnings Release

Impact: Positive

Immediate Effect: Strong growth across revenue, EBITDA, and PAT reinforces leadership in solar manufacturing and boosts investor confidence

Key Metrics:

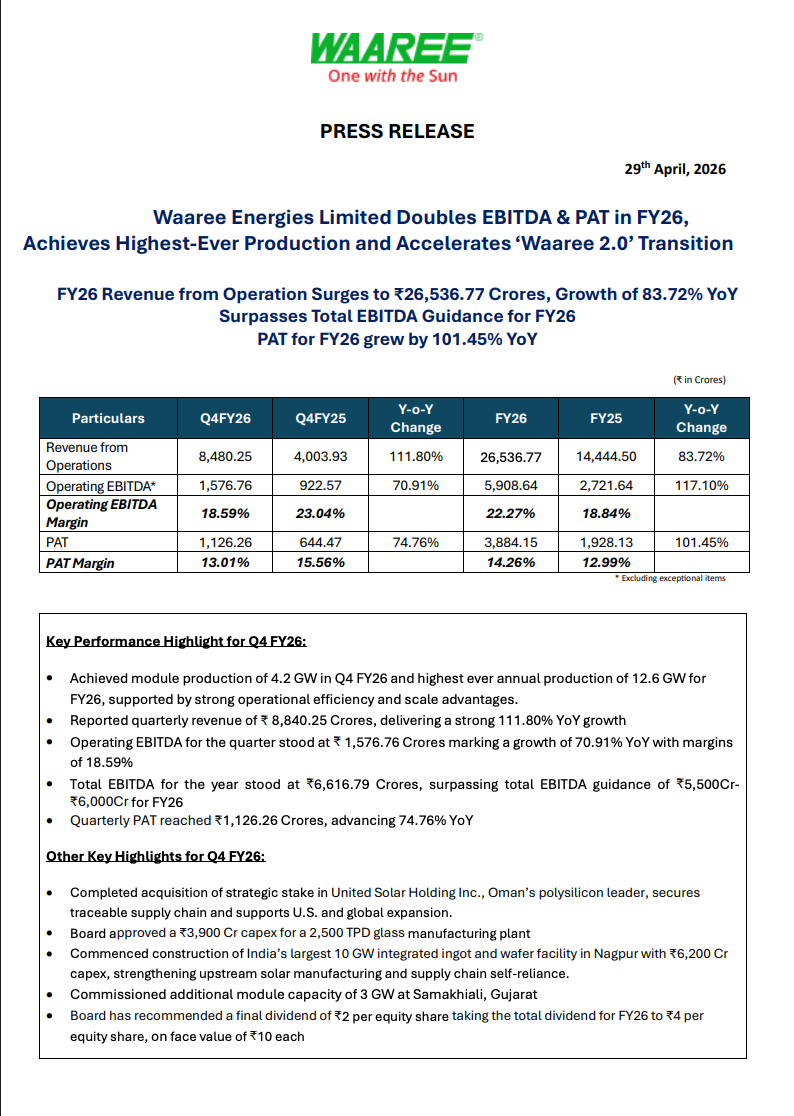

- FY26 Revenue: ₹26,536.77 crore (+83.72% YoY)

- FY26 EBITDA: ₹5,908.64 crore (+117.10% YoY)

- FY26 PAT: ₹3,884.15 crore (+101.45% YoY)

- Q4 Revenue: ₹8,480.25 crore (+111.80% YoY)

- Q4 EBITDA: ₹1,576.76 crore (+70.91% YoY)

- Q4 PAT: ₹1,126.26 crore (+74.76% YoY)

Highlight:

- EBITDA more than doubled, surpassing guidance of ₹5,500–6,000 crore

What Happened ?

Waaree Energies Limited announced its audited financial results for Q4 and FY26, reporting record-high revenue, EBITDA, and profit.

The performance was driven by strong production scale-up, backward integration, and operational efficiency improvements across solar manufacturing.

key highlights

Financial Performance & Strategic Expansion:

- Record production:

- Q4 module production: 4.2 GW

- FY26 production: 12.6 GW

- Margin profile:

- EBITDA margin (FY26): ~22.27%

- PAT margin (FY26): ~14.26%

- Strategic developments:

- Acquisition of stake in Oman-based polysilicon company

- ₹3,900 crore capex for glass manufacturing plant

- ₹6,200 crore integrated solar manufacturing facility (Nagpur)

- Additional 3 GW module capacity commissioned

- Dividend:

- Final dividend ₹2/share

- Total FY26 dividend ₹4/share

- Future guidance:

- FY27 EBITDA target: ₹7,000–7,700 crore

- Strategic direction:

- “Waaree 2.0” transformation

- Expansion into BESS, inverters, transformers, electrolyzers

Note:

Strong backward integration strategy enhances cost efficiency and supply chain control

Risk Analysis

Key Risks

- Solar module pricing volatility

- Global demand-supply imbalances

- High capex execution risks

- Policy and tariff changes

- Dependence on export markets

Worst Case Scenario

- If global solar demand weakens or pricing declines sharply, margins could compress despite high capacity

Risk Level: Medium

Company Commentary

- Delivered record-breaking financial performance

- Surpassed EBITDA guidance for FY26

- Strong focus on backward integration and scale expansion

- Transitioning to fully integrated global clean energy player

- Targeting higher EBITDA growth in FY27

Official Exchange Filing: Waaree Energies Limited