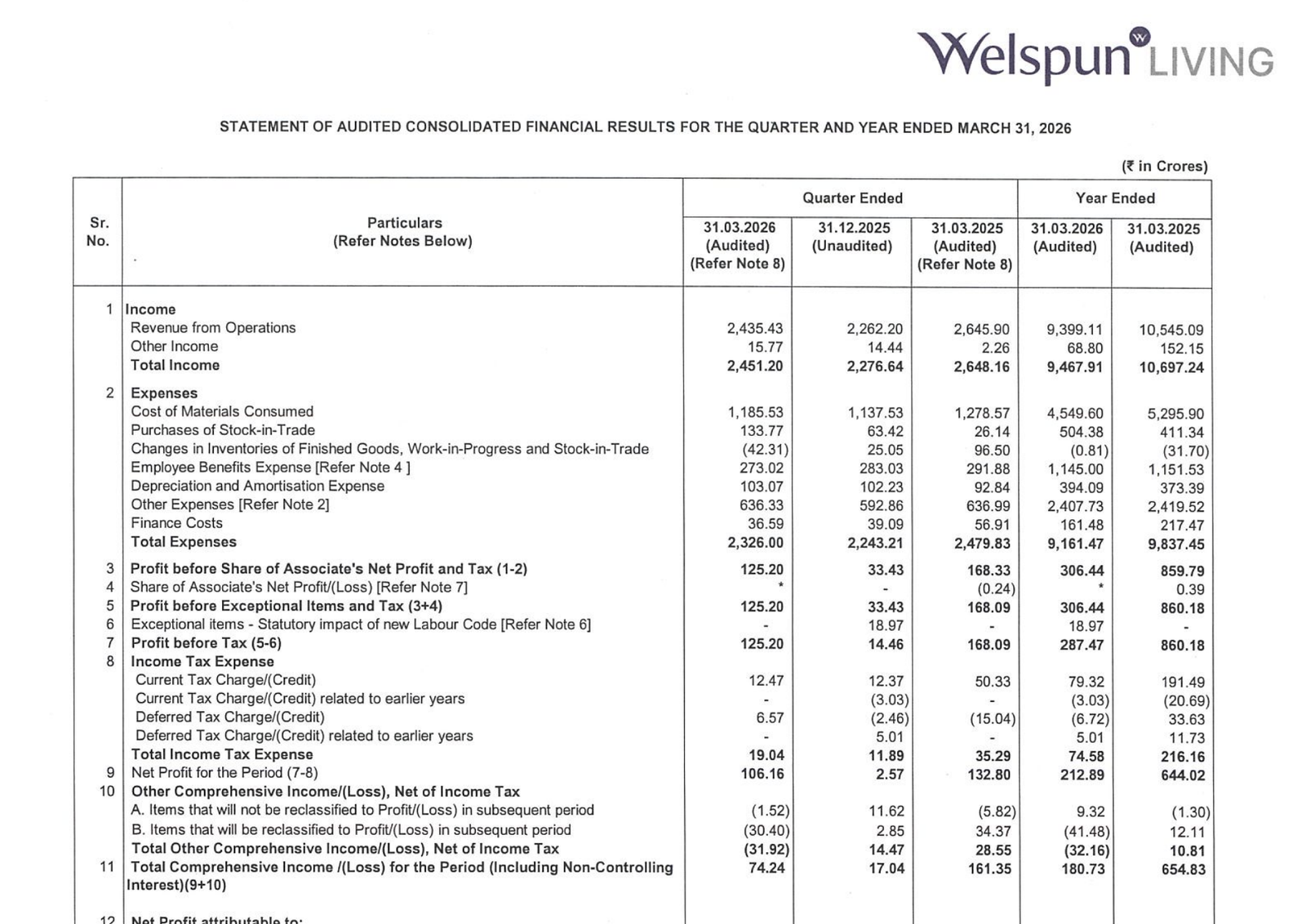

Quarter Ended: March 2026

Welspun Living Limited – Q4 FY26 Results

NSE

welspunliv

BSE

514162

Welspun Living Limited reported sequential improvement in profitability during Q4 FY26, supported by operational recovery and better cost management, though yearly performance remained below FY25 levels.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹2,435.43 Crore

- QoQ Change: +7.66%

- YoY Change: -7.96%

- Previous Quarter (Q3 FY26): ₹2,262.20 Crore

- Previous Year (Q4 FY25): ₹2,645.90 Crore

- Revenue (Q4 FY26): ₹2,435.43 Crore

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹106.16 Crore

- QoQ Change: +4030.74%

- YoY Change: -20.06%

- Previous Quarter (Q3 FY26): ₹2.57 Crore

- Previous Year (Q4 FY25): ₹132.80 Crore

- PAT (Q4 FY26): ₹106.16 Crore

- QoQ Performance:

- Revenue Trend: Sequential recovery supported by improved operational performance and inventory normalization.

- Profit Trend: Sharp improvement in profitability due to operating leverage benefits and lower quarterly disruptions.

- Revenue Trend: Sequential recovery supported by improved operational performance and inventory normalization.

Margin Analysis

Drivers:

- Better inventory management supported gross margins.

- Finance costs declined materially YoY.

- Flooring business continued to impact consolidated margins.

- Operational efficiencies improved sequentially.

- Employee and other operating expenses remained elevated.

Insight:

- Margins recovered sequentially but remained below historical highs due to weaker annual demand environment.

Segment performance

Segments: Home Textiles

- Revenue: ₹2,319.60 Crore

- Insights:

- Remained the primary revenue and profit contributor.

- Export demand softness impacted YoY performance.

- Sequential operational improvement supported recovery.

Segments: Flooring

- Revenue: ₹188.88 Crores

- Insights:

- Flooring operations remained relatively weak.

- Segment profitability stayed under pressure.

- Sequential growth indicates gradual stabilization.

Segment insight

Business Summary:

Home Textiles remained the dominant business segment, while Flooring continued to operate in a challenging profitability environment.

Key Characteristics:

- Strong global home textile exposure.

- Export-oriented business structure.

- Raw material sensitivity to cotton prices.

- Flooring business remains in scaling phase.

- Demand linked to global retail and housing markets.

Earning quality check

Key Drivers:

- Strong operating cash flow generation during FY26.

- Trade receivable reduction improved cash conversion.

- Working capital efficiency improved materially.

- Continued investment in capex and operational assets.

- Cash balances declined due to financing outflows.

Interpretations:

- Despite softer annual profitability, operational cash generation remained healthy, indicating stable underlying business efficiency.

balance sheet Analysis

- Total Assets: ₹10,455.06 Crores

- Total Liabilities: ₹5,477.11 Crores

Insight:

- The company maintained a stable balance sheet with controlled leverage and healthy equity base despite lower yearly earnings.

key risks

- Weak global consumer demand environment.

- Volatility in cotton and raw material prices.

- Export market slowdown risk.

- Currency fluctuation exposure.

- Margin pressure from higher operating costs.

- Flooring segment profitability uncertainty.

management strategy signals

Focus Area:

- Strengthening branded product portfolio.

- Improving operational efficiencies.

- Expanding value-added textile offerings.

- Stabilizing flooring segment profitability.

- Maintaining disciplined working capital management.

- Continuing sustainability and automation investments.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹2,451.20 Crores | +7.67% | -7.43% |

| PBT | ₹125.20 Crores | +765.98% | -25.52% |

| PAT | ₹106.16 Crores | +4030.74% | -20.06% |

Welspun Living Limited delivered a strong sequential recovery in Q4 FY26 after a weak preceding quarter. Operational improvements, lower finance costs, and better working capital management supported earnings recovery.

However, annual revenue and profitability remained below FY25 levels due to continued softness in export demand and pressure within the flooring business. Strong cash flow generation and a stable balance sheet remain positive indicators for medium-term business stability.

Official Exchange Filing: Welspun Living Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED