Quarterly & Annual Financial Results

Xpro India Limited Reports Q4 FY26 Results: Revenue Declines, But Profitability Improves Sequentially

NSE

xproindia

BSE

590013

Xpro India Limited announced its audited standalone Q4 FY26 and FY26 financial results. The company reported a year-on-year decline in revenue due to softer refrigerator production and lower offtake, while EBITDA, PBT, and PAT improved sequentially. The company also highlighted commissioning of its new dielectric film line at Barjora and ongoing UAE project execution.

PRICE-SENSITIVE TRIGGER

Event: Xpro India Limited announced audited standalone financial results for Q4 FY26 and FY26 along with operational and expansion updates.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Revenue declined YoY, while margins and profitability improved sequentially. New dielectric film capacity was commissioned and UAE expansion remains on track.

Key Metrics:

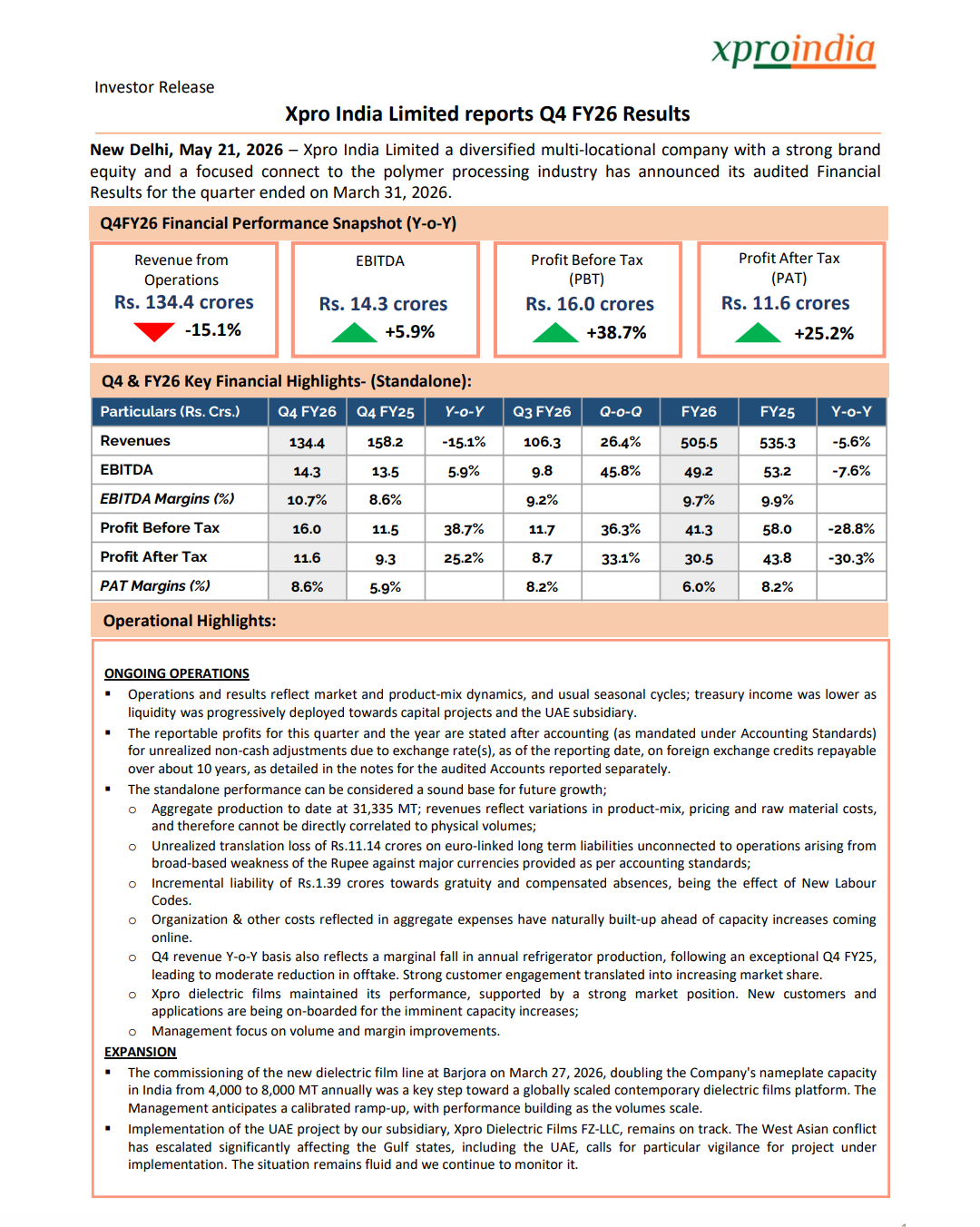

- Q4 FY26 Revenue stood at Rs. 134.4 crore, down 15.1% YoY.

- FY26 Revenue stood at Rs. 505.5 crore, down 5.6% YoY.

- Q4 FY26 EBITDA came at Rs. 14.3 crore, up 5.9% YoY.

- Q4 FY26 EBITDA Margin improved to 10.7% from 8.6% in Q4 FY25.

- FY26 EBITDA stood at Rs. 49.2 crore versus Rs. 53.2 crore in FY25.

- FY26 EBITDA Margin was 9.7% compared to 9.9% in FY25.

- Q4 FY26 Profit Before Tax (PBT) stood at Rs. 16.0 crore, up 38.7% YoY.

- FY26 PBT stood at Rs. 41.3 crore, down 28.8% YoY.

- Q4 FY26 Profit After Tax (PAT) stood at Rs. 11.6 crore, up 25.2% YoY.

- Q4 FY26 PAT Margin improved to 8.6% from 5.9% in Q4 FY25.

- FY26 PAT stood at Rs. 30.5 crore, down 30.3% YoY.

- FY26 PAT Margin came at 6.0% compared to 8.2% in FY25.

- Q4 FY26 Revenue increased 26.4% QoQ from Q3 FY26.

- Q4 FY26 EBITDA increased 45.8% QoQ.

- Q4 FY26 PBT increased 36.3% QoQ.

- Q4 FY26 PAT increased 33.1% QoQ.

- FY26 Return on Capital Employed (RoCE) stood at 5.3%.

- FY26 Return on Equity (RoE) stood at 4.6%.

- Net Debt to Equity ratio improved to -0.08x in FY26.

- Equity base increased to Rs. 715.5 crore in FY26 from Rs. 616.9 crore in FY25.

Highlight Metric:

- Q4 FY26 EBITDA margin improved to 10.7% from 9.2% in Q3 FY26 and 8.6% in Q4 FY25.

What Happened ?

Xpro India Limited reported a mixed financial performance for Q4 FY26. While standalone revenue declined year-on-year due to moderation in annual refrigerator production and lower offtake following an exceptional Q4 FY25, the company delivered strong sequential improvement in profitability metrics.

EBITDA increased 5.9% YoY to Rs. 14.3 crore, while PAT rose 25.2% YoY to Rs. 11.6 crore. Margin expansion was supported by better operational execution, product mix improvements, and disciplined cost management.

The company also announced the commissioning of its new dielectric film manufacturing line at Barjora on March 27, 2026. This expansion doubled the company’s dielectric films nameplate capacity in India from 4,000 MT to 8,000 MT annually.

Management stated that the UAE dielectric films project remains on track despite geopolitical uncertainties and rising regional tensions in West Asia.

Key Details

Q4 FY26 Operational Highlights:

- Revenue from operations declined 15.1% YoY to Rs. 134.4 crore in Q4 FY26.

- FY26 total revenue declined 5.6% YoY to Rs. 505.5 crore.

- EBITDA increased 5.9% YoY to Rs. 14.3 crore despite lower revenue.

- EBITDA margin expanded to 10.7% in Q4 FY26 versus 8.6% in Q4 FY25.

- PAT increased 25.2% YoY to Rs. 11.6 crore.

- PAT margin improved sharply to 8.6% compared to 5.9% last year.

- Sequentially, Q4 FY26 revenue rose 26.4% over Q3 FY26.

- Sequential EBITDA growth stood at 45.8%.

- Sequential PAT growth stood at 33.1%.

- Production during FY26 aggregated 31,335 MT.

- Treasury income declined as liquidity was progressively deployed toward capital projects and UAE subsidiary investments.

- Reported profits included unrealized non-cash foreign exchange adjustments related to euro-linked liabilities.

- Unrealized translation loss of Rs. 11.14 crore was recorded due to rupee weakness against major currencies.

- Additional liability of Rs. 1.39 crore toward gratuity and compensated absences was recognized due to implementation impact of New Labour Codes.

- Organization and operational costs increased ahead of planned capacity additions.

- Dielectric films business maintained performance supported by strong market positioning.

- New customers and applications are being onboarded ahead of capacity scale-up.

- Management continues focusing on volume growth and margin improvement initiatives.

Note:

- Management clarified that revenue movement cannot be directly correlated with production volumes because product mix, raw material pricing, and customer pricing dynamics significantly influence realizations.

Expansion & Strategic Developments:

- Xpro India commissioned its new dielectric film line at Barjora on March 27, 2026.

- The commissioning doubled domestic dielectric film capacity from 4,000 MT to 8,000 MT annually.

- Management views the expansion as a key step toward building a globally scaled dielectric films platform.

- Performance ramp-up is expected to happen gradually as utilization improves over time.

- UAE dielectric films project through subsidiary Xpro Dielectric Films FZ-LLC remains on schedule.

- Management acknowledged rising geopolitical tensions in West Asia could impact project execution and monitoring requirements.

Note:

- The company is pursuing calibrated international expansion while maintaining a conservative balance sheet structure with negative net debt-to-equity ratio.

Risk Analysis

Summary:

- Xpro India faces near-term demand moderation, forex volatility, geopolitical uncertainties, and margin sensitivity linked to product mix and capacity ramp-up execution.

Key Risks:

- Refrigerator production slowdown impacted annual revenue growth.

- Unrealized forex losses affected reported profitability.

- Large capital deployment may pressure near-term return ratios.

- UAE project execution carries geopolitical and operational risks.

- Margin sustainability depends on successful utilization ramp-up of new dielectric film capacity.

- Increased organizational costs ahead of utilization growth may temporarily suppress earnings efficiency.

- Seasonal demand cycles and raw material fluctuations remain ongoing operational risks.

Worst Case Scenario:

- If demand recovery remains weak and capacity ramp-up is delayed while forex volatility persists, profitability and return ratios could remain under pressure despite expanded manufacturing capacity.

Risk Level: Medium

Company Commentary

- Operations reflected normal market and product mix dynamics along with seasonal cycles.

- Treasury income reduced as liquidity was deployed toward strategic capital projects.

- The standalone business provides a strong foundation for future growth.

- Strong customer engagement is translating into increasing market share.

- Dielectric films business continues to benefit from strong market positioning.

- New customer additions and application development support long-term growth visibility.

- Management remains focused on improving both volumes and margins.

- UAE project execution continues despite fluid geopolitical conditions.

Official Exchange Filing: Xpro India Limited