Credit Rating Upgrade

YES Bank: CareEdge Upgrades Long-Term Rating to AA+; Stable Outlook Reaffirmed

NSE

yesbank

BSE

532648

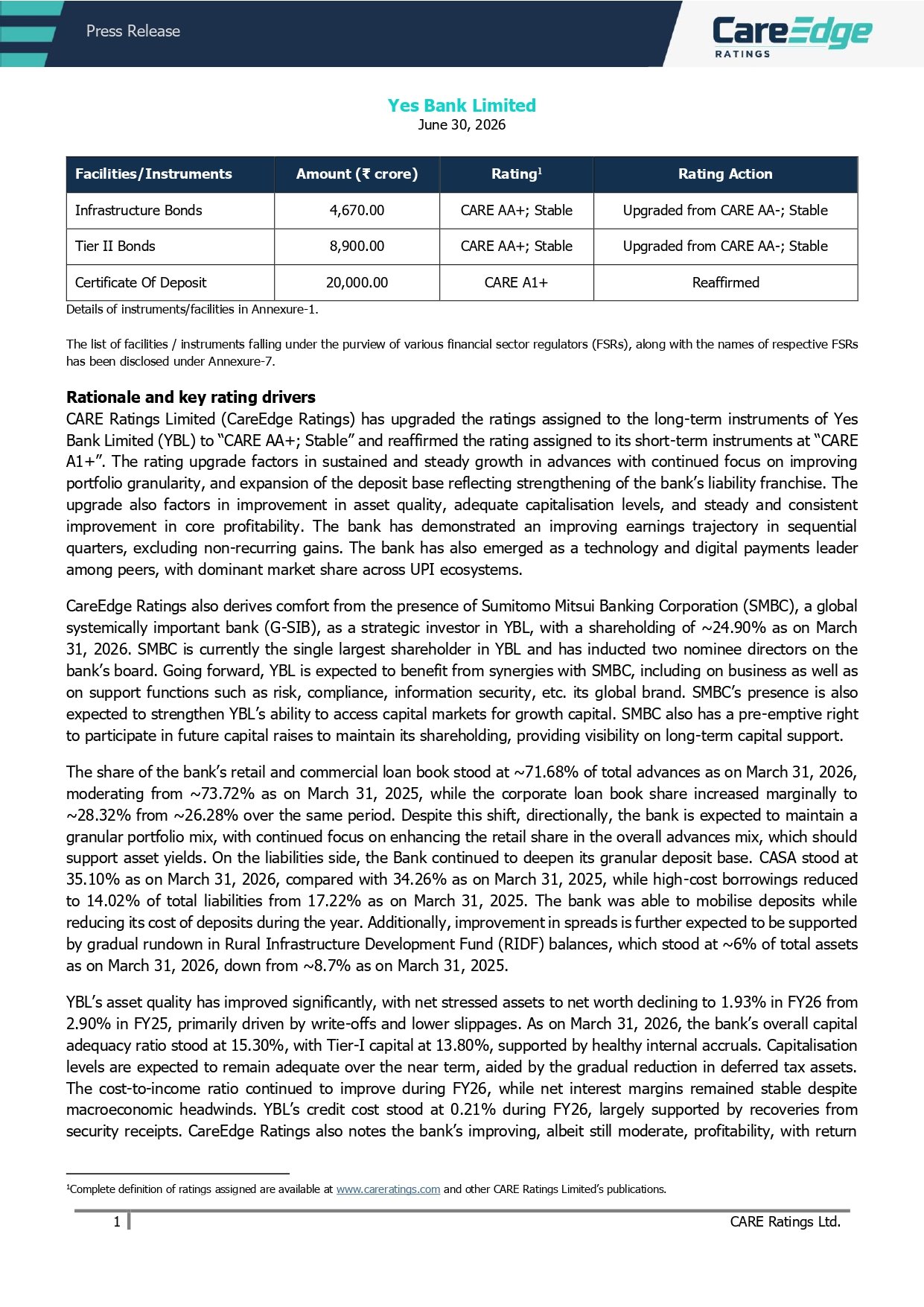

YES Bank has informed the stock exchanges that CareEdge Ratings has upgraded the Bank’s long-term Infrastructure Bonds and Tier II Bonds rating from CARE AA-/Stable to CARE AA+/Stable, while reaffirming its short-term Certificate of Deposit rating at CARE A1+. The upgrade reflects improving asset quality, stronger profitability, steady business growth, enhanced liability franchise, and adequate capitalisation.

PRICE-SENSITIVE TRIGGER

Event: CareEdge Ratings upgrades YES Bank’s long-term credit ratings.

Type: Credit Rating Upgrade

Impact: Positive

Immediate Effect: The upgrade strengthens YES Bank’s credit profile, improves confidence among investors and debt market participants, and may enhance the Bank’s future borrowing flexibility.

Key Metrics:

- Total Income: ₹36,928 crore (FY26) vs ₹36,752 crore (FY25)

- Profit After Tax (PAT): ₹3,476 crore vs ₹2,406 crore (~42% YoY growth)

- Total Assets: ₹4,62,552 crore vs ₹4,15,767 crore

- Net Interest Margin (NIM): 2.21% vs 2.20%

- Gross NPA: Improved to 1.30% from 1.60%

- Net NPA: Improved to 0.20% from 0.30%

- Capital Adequacy Ratio (CAR): 15.30%

- Tier-I Capital Ratio: 13.80%

- Return on Total Assets (RoTA): Improved to 0.80% from 0.60%

- CASA Ratio: Increased to 35.10%

- Credit Cost: Declined to 0.21%

Highlight:

- PAT increased approximately 42% year-on-year while asset quality continued to improve significantly.

What Happened ?

CareEdge Ratings upgraded YES Bank’s long-term debt instruments to CARE AA+/Stable after assessing sustained improvement across the Bank’s operating and financial profile.

The rating agency cited:

- steady growth in advances,

- stronger deposit franchise,

- improved asset quality,

- consistent profitability improvement,

- healthy capital position,

- expanding digital banking leadership,

- and strategic support from Sumitomo Mitsui Banking Corporation (SMBC).

The short-term Certificate of Deposit rating was reaffirmed at CARE A1+.

Key Details

Rating Upgrade Drivers:

- Infrastructure Bonds upgraded from CARE AA-/Stable to CARE AA+/Stable.

- Tier II Bonds upgraded from CARE AA-/Stable to CARE AA+/Stable.

- Certificate of Deposit reaffirmed at CARE A1+.

- Deposit base continued expanding with improving CASA ratio.

- High-cost borrowings reduced, improving funding quality.

- Retail and commercial banking continue to dominate the advances portfolio.

- Asset quality improved through lower slippages and stronger recoveries.

- PAT and operating profitability strengthened during FY26.

- Digital payments franchise remains among India’s market leaders with significant UPI market share.

- SMBC, holding approximately 24.9%, continues to provide strategic support and governance strength.

Operational Significance:

- The rating upgrade reflects a broad-based strengthening of YES Bank’s balance sheet rather than a single event. Improvements across deposits, profitability, capital, asset quality and operating efficiency collectively contributed to the higher credit rating.

Risk Analysis

Summary:

- Although the rating action is positive, CareEdge notes that several operating risks continue to require monitoring before further upgrades become likely.

Key Risks:

- Profitability remains moderate relative to higher-rated peers.

- Retail loan slippages remain elevated despite recent improvement.

- Sustaining lower cost-to-income ratio remains important.

- Asset quality deterioration could pressure future ratings.

- Regulatory or legal developments relating to historical AT1 bond matters remain monitorable.

- Capital adequacy must remain comfortably above regulatory requirements.

Worst Case:

- A sustained decline in profitability, weakening capitalisation or deterioration in asset quality could result in future rating pressure or downgrade.

Risk Level: Medium

Company Commentary

- CareEdge expects business performance to continue improving under a Stable outlook.

- The Bank is expected to benefit from stronger retail deposits and a granular funding profile.

- Continued reduction in low-yield assets should support margins.

- Synergies with SMBC are expected to strengthen business growth, governance, risk management and future capital access.

- Management focus remains on maintaining capital adequacy while improving profitability and operating efficiency.

Official Exchange Filing: YES Bank Limited