Credit Rating Upgrade

YES Bank Receives ICRA Credit Rating Upgrade to AA/Stable on Infrastructure and Basel III Tier II Bonds

NSE

yesbank

BSE

532648

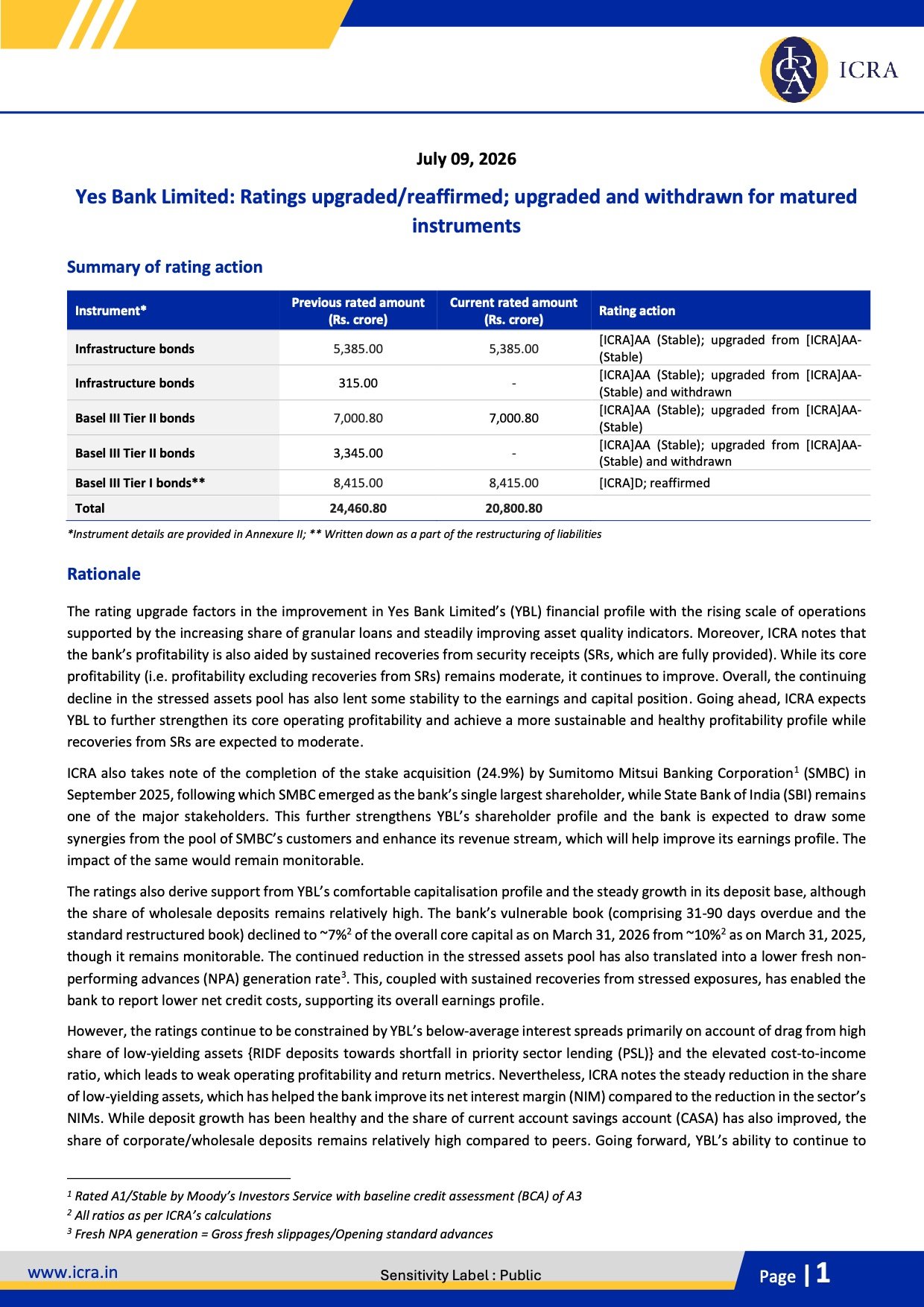

ICRA has upgraded YES Bank’s long-term rating on its Infrastructure Bonds and Basel III Tier II Bonds from ICRA AA-/Stable to ICRA AA/Stable, reflecting continued improvement in the bank’s financial profile, asset quality, profitability, capitalization, and business scale. The rating on the written-down Basel III Tier I Bonds remains reaffirmed at ICRA D.

PRICE-SENSITIVE TRIGGER

Event: ICRA Credit Rating Upgrade

Type: Credit Rating Upgrade

Impact: Positive

Immediate Effect: The rating upgrade strengthens YES Bank’s credit profile, potentially lowering future borrowing costs, improving investor confidence, and reinforcing the bank’s access to capital markets. The reaffirmation of the AT-1 bonds at ICRA D has no incremental impact as these instruments were written down during the 2020 reconstruction.

Financials:

Key Metrics:

- Total Income: ₹15,826 crore (↑ 10.2% YoY from ₹14,358 crore)

- Profit After Tax (PAT): ₹3,476 crore (↑ 44.5% YoY from ₹2,406 crore)

- Total Assets: ₹4.69 lakh crore (↑ 10.9% YoY from ₹4.23 lakh crore)

- CET-1 Ratio: 13.78% (vs 13.52% in FY2025)

- Capital Adequacy Ratio (CRAR): 15.27% (vs 15.64% in FY2025)

- Gross NPA: 1.30% (improved from 1.58%)

- Net NPA: 0.24% (improved from 0.33%)

Highlight:

- ICRA upgraded YES Bank’s Infrastructure Bonds and Basel III Tier II Bonds to ICRA AA/Stable, citing stronger financial performance, improving asset quality, comfortable capitalisation, and sustained business growth.

What Happened ?

YES Bank informed the stock exchanges that ICRA has upgraded the ratings on its Infrastructure Bonds and Basel III Tier II Bonds from ICRA AA-/Stable to ICRA AA/Stable.

According to ICRA, the upgrade reflects:

- Continuous improvement in the bank’s financial profile.

- Growth in granular retail lending.

- Improving asset quality.

- Better profitability supported by recoveries from legacy stressed assets.

- Comfortable capital position.

- Healthy deposit growth.

- Strategic benefits expected from Sumitomo Mitsui Banking Corporation (SMBC) becoming the bank’s largest shareholder following its 24.9% stake acquisition in September 2025.

Key details

ICRA Rating Rationale:

- Infrastructure Bonds upgraded to ICRA AA/Stable.

- Basel III Tier II Bonds upgraded to ICRA AA/Stable.

- Basel III Tier I Bonds reaffirmed at ICRA D (already written down during the 2020 reconstruction).

- Loan book expanded to ₹2.73 lakh crore.

- Deposit base increased to ₹3.19 lakh crore.

- Retail loan mix continued to improve.

- Gross NPA declined to 1.30%.

- Net NPA reduced to 0.24%.

- Profitability improved with PAT rising nearly 45% YoY.

- Daily average Liquidity Coverage Ratio (LCR): 119%.

- Net Stable Funding Ratio (NSFR): 118%, comfortably above regulatory requirements.

- Recoveries from legacy stressed assets continue to support earnings.

- SMBC’s strategic investment is expected to create business synergies and enhance long-term earnings.

Note:

- ICRA also withdrew ratings on certain redeemed Infrastructure Bonds and Basel III Tier II Bonds as no outstanding amount remains against those instruments.

Risk Analysis

Summary:

- While YES Bank’s operating profile continues to strengthen, ICRA highlighted that profitability remains below leading private-sector peers and several factors continue to warrant monitoring.

Key Risks:

- Net interest margins remain below industry leaders.

- Cost-to-income ratio is still relatively high.

- Corporate/wholesale deposits remain elevated versus peers.

- Vulnerable loan book, although declining, remains under watch.

- Future recoveries from security receipts are expected to moderate.

- Supreme Court’s pending decision regarding the ₹8,415 crore AT-1 bond write-off could impact reported CET-1 capital if an adverse ruling requires a write-back.

Worst Case:

- If asset quality weakens significantly, credit costs rise, or the Supreme Court ruling adversely affects capital buffers, the bank’s profitability and capital adequacy could come under pressure, potentially affecting future ratings.

Risk Level: Medium

Company Commentary

- ICRA has upgraded the ratings on its Infrastructure Bonds and Basel III Tier II Bonds to ICRA AA/Stable.

- The Basel III Tier I Bonds remain rated ICRA D, as these instruments were written down during the bank’s restructuring.

- The bank has placed the rating release on its website for stakeholders.

Official Exchange Filing: YES Bank Limited