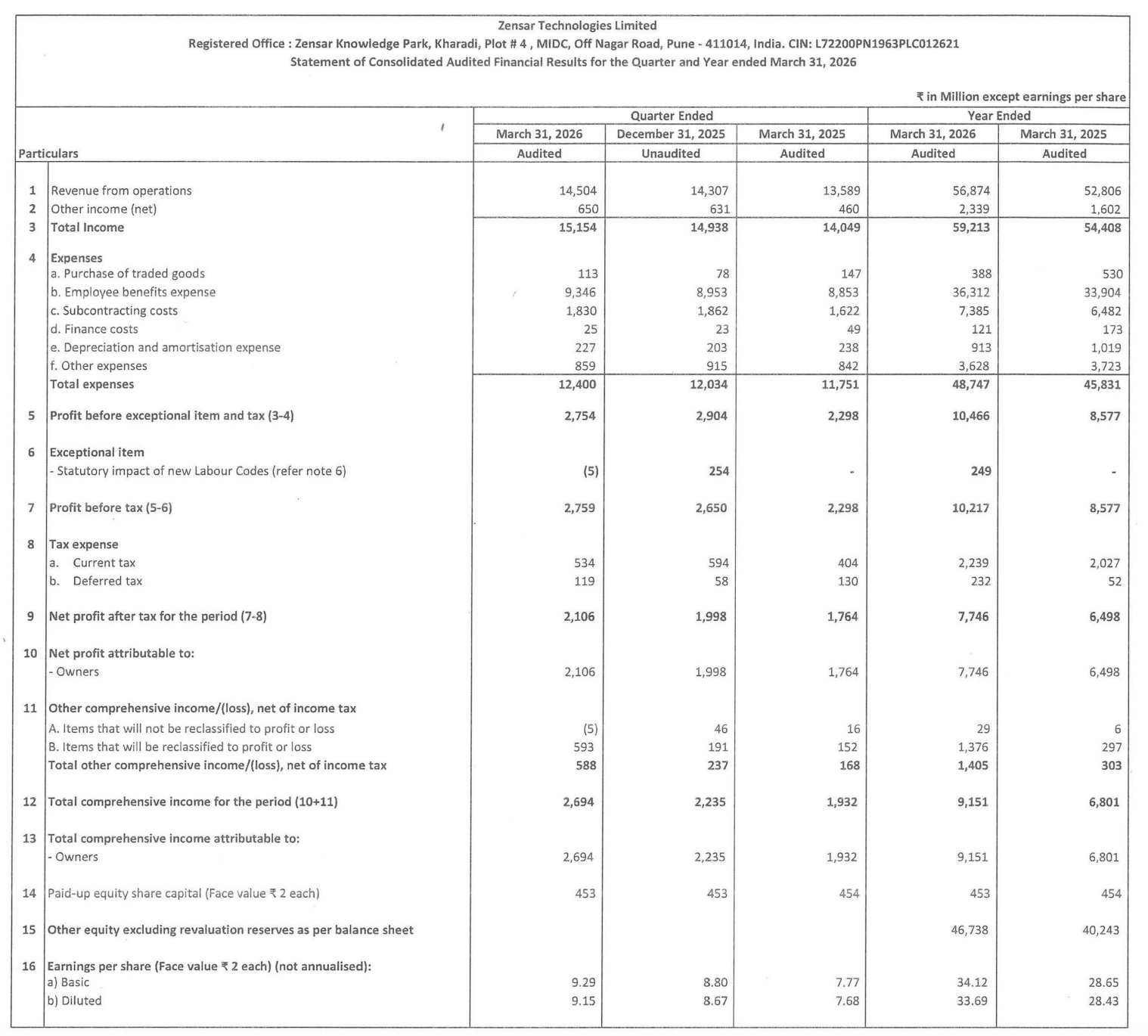

Quarter Ended: March 2026

Zensar Technologies Ltd – Q4 FY26 Financial Results Analysis

NSE

zensartech

BSE

504067

Revenue growth remains stable, but margin pressure due to rising employee and operational costs is limiting profit expansion

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹14,504 Mn

- QoQ Change: +1.38%

- YoY Change: +6.74%

- Previous Quarter (Q3 FY26): ₹14,307 Mn

- Previous Year (Q4 FY25): ₹13,589 Mn

- Total Income (Q4 FY26): ₹14,504 Mn

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,106 Mn

- QoQ Change: +5.41%

- YoY Change: +19.38%

- Previous Quarter (Q3 FY26): ₹1,998 Mn

- Previous Year (Q4 FY25): ₹1,764 Mn

- PAT (Q4 FY26): ₹2,106 Mn

- QoQ Performance

- Revenue Trend: Stable

- Profit Trend: Moderate growth

Margin Analysis

Key Drivers:

- Increase in employee benefit expenses

- Higher subcontracting costs

- Stable but slightly rising operating expenses

- Limited operating leverage

Key Signal: Margins are under pressure as expense growth slightly outpaces revenue growth

Segment performance

Segment: Digital & Application Services

- Revenue: ₹11,145 Mn

Insights:

- Core revenue contributor

- Stable QoQ performance

Segment: Cloud Infrastructure & Security

- Revenue: ₹3,359 Mn

Insights:

- Faster YoY growth compared to core segment

- Increasing contribution share

Segment insight

Summary:

- Zensar is gradually shifting toward higher growth cloud and digital services, though traditional segments still dominate.

Characteristics:

- IT services-driven model

- Transition toward digital transformation services

- Balanced segment mix improving

Earning quality check

Drivers:

- Core operating income driven

- No major exceptional dependence

- Strong operating cash flow

- Stable depreciation and finance costs

Interpretation:

- Earnings quality is good, though margin compression slightly impacts overall strength

balance sheet Analysis

- Total Assets: ₹60,835 Mn

- Total Liabilities: ₹13,644 Mn

Insight:

- Strong balance sheet with high equity cushion and low leverage

key risks

- Margin pressure due to rising employee costs

- Dependency on IT spending cycles

- Currency fluctuations

- Competitive IT services landscape

management strategy signals

- Focus Areas:

- Expansion in cloud and digital services

- Cost optimization

- Improving operating efficiency

- Strengthening client base

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹15,154 Million | +1.44% | +7.87% |

| PBT | ₹2,759 Million | +4.11% | +20.06% |

| PAT | ₹2,106 Million | +5.41% | +19.38% |

Zensar Technologies delivered a stable quarter with consistent revenue growth and moderate profit expansion. However, margin pressure remains a concern due to rising costs. The company is steadily transitioning toward higher-growth digital segments, which may support future profitability.

Official Exchange Filing: Zener technologies Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED