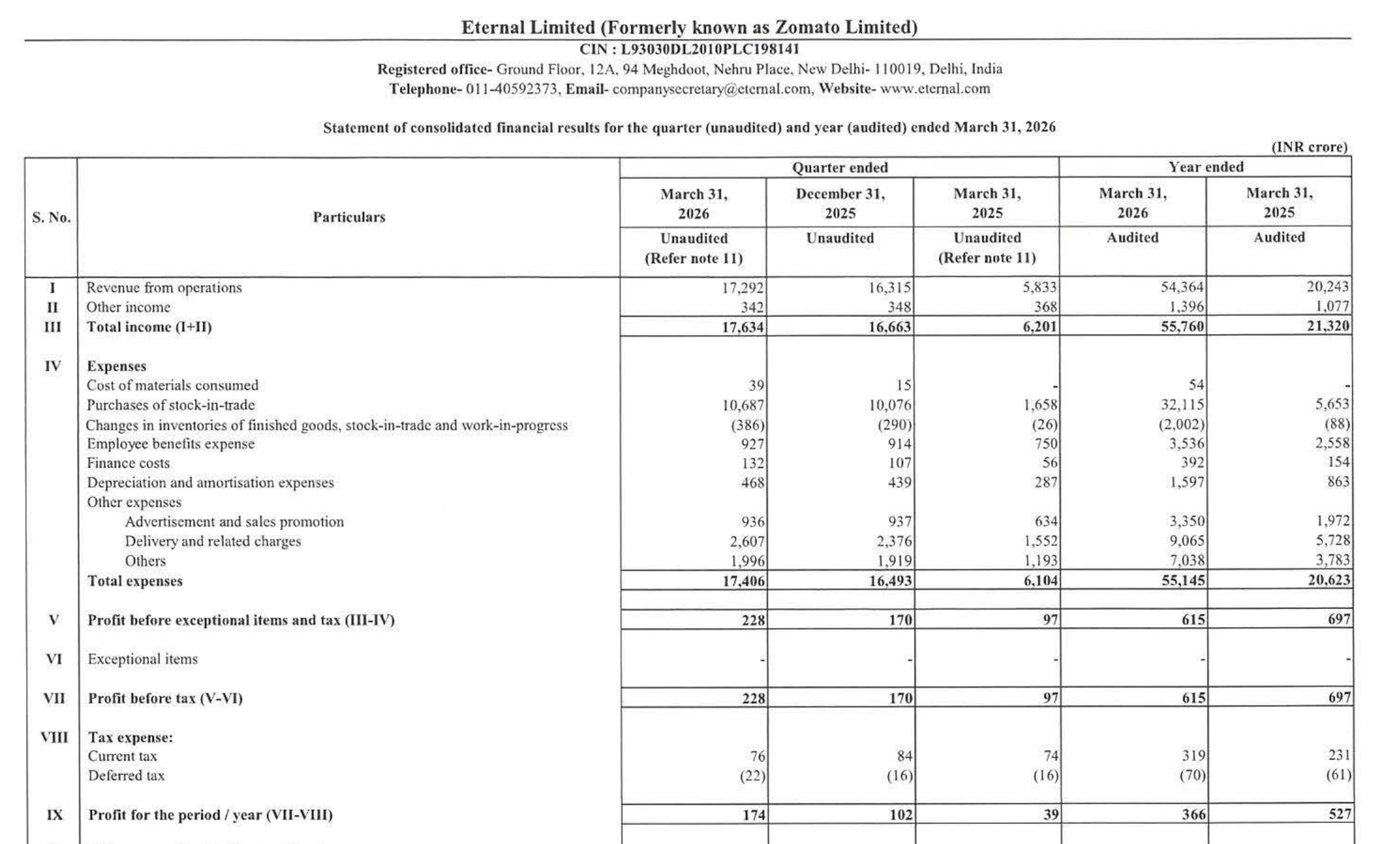

Quarter Ended: March 2026

Zomato (Eternal) – Q4 FY26 Results

NSE

zomato

BSE

543320

Strong topline growth driven by business expansion, but higher costs and operating leverage challenges led to sharp decline in profits.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹17,292 Cr

- QoQ Change: +6.0%

- YoY Change: +196.5%

- Previous Quarter (Q3 FY26): ₹16,315 Cr

- Previous Year (Q4 FY25): ₹5,833 Cr

- Revenue (Q4 FY26): ₹17,292 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹174 Cr

- QoQ Change: +70.6%

- YoY Change: +346%

- Previous Quarter (Q3 FY26): ₹102 Cr

- Previous Year (Q4 FY25): ₹39 Cr

- PAT (Q4 FY26): ₹174 Cr

- Note: Quarterly profit is up YoY, but FY profit declined significantly

- QoQ Performance

- Revenue Trend: Moderate growth

- Profit Trend: Strong recovery

Margin Analysis

Key Drivers:

- Significant rise in delivery & logistics costs (₹2,607 Cr)

- High advertising & promotional expenses

- Increased employee and platform costs

- Heavy reinvestment in growth segments

Key Signal: Despite strong growth, profit margins remain thin, reflecting aggressive expansion strategy

Segment insight

Summary:

- Business driven by food delivery + quick commerce + platform expansion, where growth is prioritized over margins

Characteristics:

- High customer acquisition cost

- Platform-led scalability

- High operating leverage potential

- Continuous reinvestment phase

Earning quality check

Drivers:

- Strong operating cash flow: ₹632 Cr

- High non-cash adjustments (depreciation ₹1,291 Cr)

- Significant working capital movements

- Share-based payments impact

Interpretation:

- Earnings quality is moderate to strong, supported by positive cash flow but diluted by high reinvestment and non-cash expenses.

balance sheet Analysis

- Total Assets: ₹40,736 Cr

- Total Liabilities: ₹9,763 Cr

Insight:

- Strong equity base (~₹30,973 Cr)

- Low leverage structure

- High cash & investment reserves

- Strong liquidity position

key risks

- High competition in food delivery & quick commerce

- Sustained margin pressure due to discounting

- Rising logistics and operational costs

- Execution risk in new verticals

management strategy signals

Focus Area:

- Expansion in quick commerce

- Market share growth

- Cost optimization over time

- Platform monetization

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹17,634 Crore | +5.8% | +184.3% |

| PBT | ₹228 Crore | +34.1% | +135.1% |

| PAT | ₹174 Crore | +70.6% | +346% |

Zomato (Eternal) continues to deliver explosive revenue growth, but profitability remains fragile due to aggressive expansion and high cost structure. The company is clearly prioritizing market dominance over margins, making it a high-growth, high-risk story.

Official Exchange Filing: Zomato (Eternal) Ltd

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED