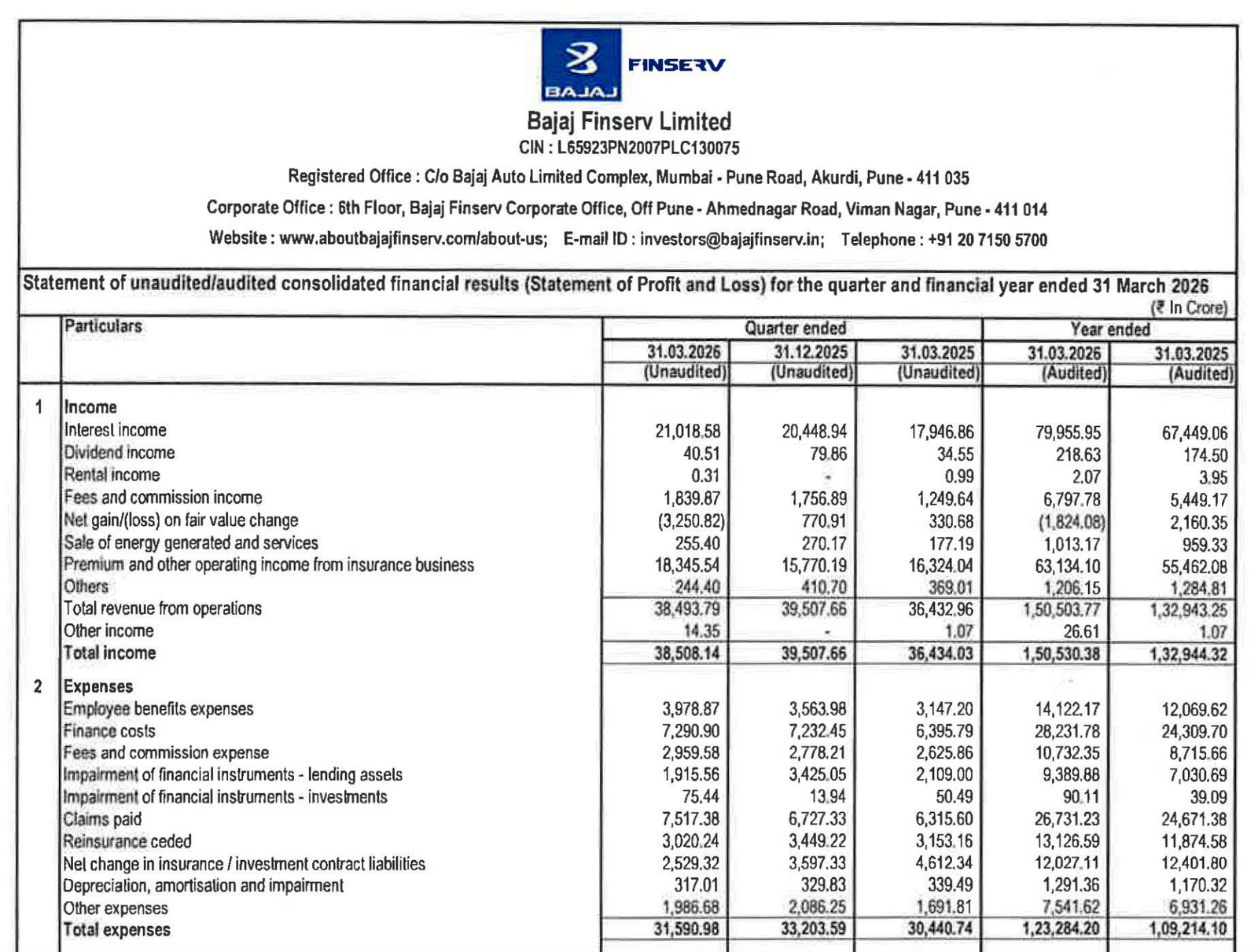

Quarter Ended: March 2026

Bajaj Finserv Ltd – Q4 FY26 Results

NSE

BAJAJFINSV

BSE

532978

Robust revenue and profit growth driven by insurance and lending segments, though rising credit costs and negative operating cash flows remain key monitorables

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹38,508.14 Cr

- QoQ Change: -2.5%

- YoY Change: +5.7%

- Previous Quarter (Q3 FY26): ₹39,507.66 Cr

- Previous Year (Q4 FY25): ₹36,434.03 Cr

- Total Income (Q4 FY26): ₹38,508.14 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,538.67 Cr

- QoQ Change: +13.9%

- YoY Change: +5.0%

- Previous Quarter (Q3 FY26): ₹2,229.15 Cr

- Previous Year (Q4 FY25): ₹2,416.64 Cr

- PAT (Q4 FY26): ₹2,538.67 Cr

- QoQ Performance

- Revenue Trend: Slight decline

- Profit Trend: Strong improvement

Margin Analysis

Drivers:

- Growth in high-margin insurance business

- Elevated finance costs (₹7,290 Cr) impacting margins

- Increase in impairment costs

Insight:

- Margins stable but under pressure due to rising credit costs and financing expenses

Segment performance

Segment: Insurance

- Revenue: ₹17,058.51 Cr

- Major growth contributor

- Life + General insurance driving scale

Segment: Retail Financing

- Revenue: ₹21,606.51 Cr

- Core earnings engine

- Strong growth but higher risk exposure

Segment: Investments & Other

- Revenue: ₹496.33 Cr

- Minor contribution

Segment insight

Summary:

- Bajaj Finserv remains a diversified financial conglomerate with strong dual engines: lending + insurance

Charcateristics:

- Credit-driven growth model

- Insurance provides stability + margin support

- High dependence on economic cycle

Earning quality check

Drivers:

- Strong operating profit growth

- Rising impairment on financial instruments

- Dependence on lending spreads

Interpretations:

- Earnings are strong but slightly risk-adjusted due to credit cycle exposure

balance sheet Analysis

- Total Assets: ₹7,58,497.54 Cr

- Total Liabilities: ₹6,08,320.92 Cr

Insight:

- Large and expanding balance sheet reflecting aggressive credit growth; leverage is inherent to NBFC structure

Cash flow analysis

Operating Cash Flow: ₹(55,301.41 Cr) → Negative

Investing Cash Flow: ₹(12,634.87 Cr)

Financing Cash Flow: ₹66,610.32 Cr

Insight:

- Negative operating cash flow is typical for lending businesses due to loan book expansion; funding supported via financing inflows.

key risks

- Rising NPAs / credit costs

- Interest rate sensitivity

- Regulatory changes in financial services

- Insurance claim volatility

management strategy signals

Focus Area:

- Expansion in retail lending

- Strengthening insurance penetration

- Digital financial ecosystem

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹38,508.14 Cr | -2.5% | +5.7% |

| Total Expense | ₹31,590.98 Cr | -4.8% | +3.8% |

| Net Profit | ₹2,538.67 Cr | +13.9% | +5.0% |

Bajaj Finserv continues to deliver consistent growth backed by strong lending and insurance businesses. However, rising credit costs and negative operating cash flows indicate increasing dependence on funding markets. The long-term story remains intact, but near-term risk lies in asset quality trends.

Official Exchange Filing: Bajaj Finders Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED