Quarter Ended: March 2026

Saregama India Limited – Q4 FY26 Results

NSE

saregama

BSE

532163

Saregama India Limited reported strong Q4 FY26 profitability growth led by healthy music monetisation, rapid artist management expansion, and improved operational efficiency despite weakness in events and video businesses.

key financial highlights

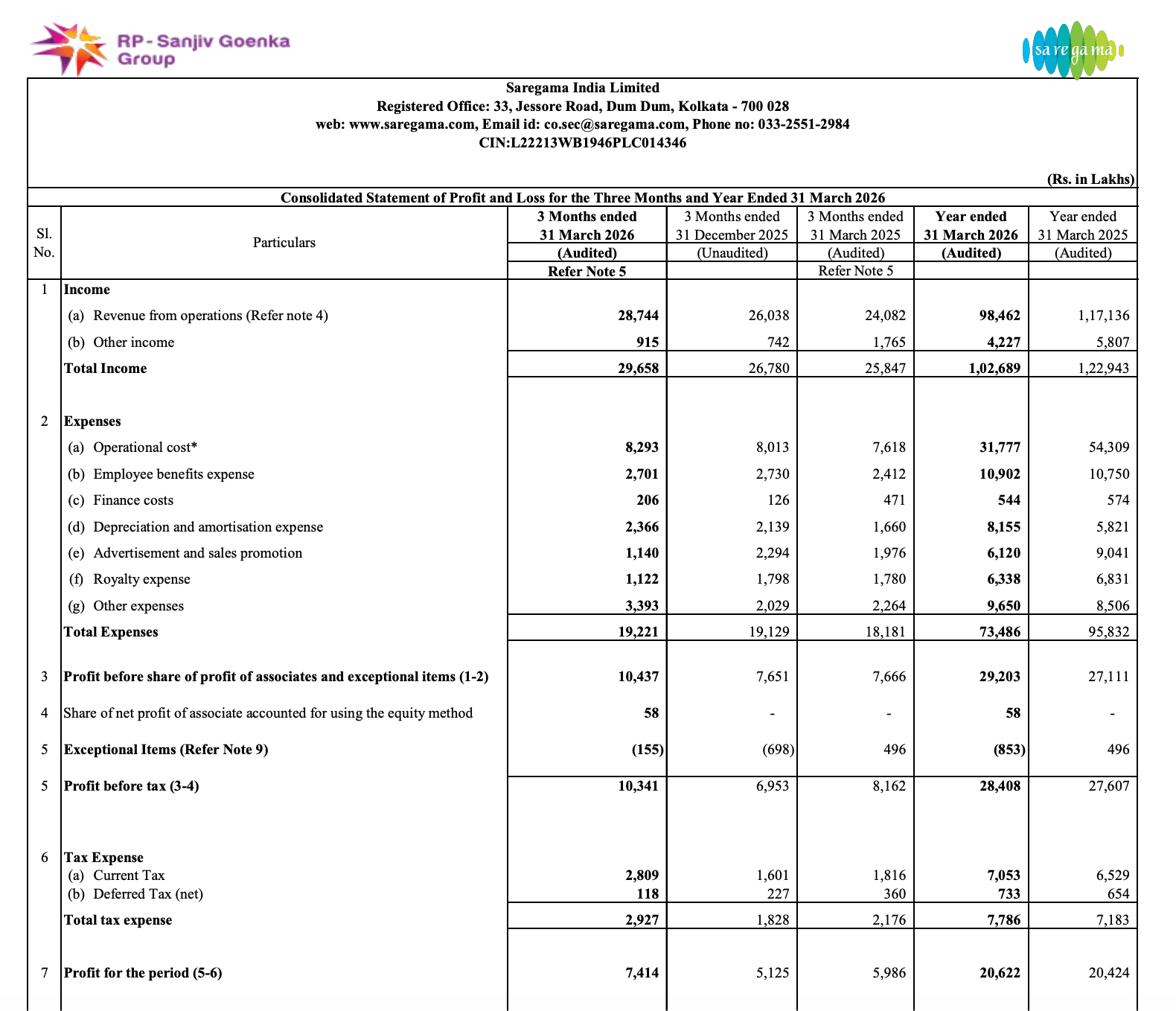

- Revenue from Operations:

- Revenue (Q4 FY26): ₹28,744 Lakh

- QoQ Change: +10.39%

- YoY Change: +19.36%

- Previous Quarter (Q3 FY26): ₹26,038 Lakh

- Previous Year (Q4 FY25): ₹24,082 Lakh

- Revenue (Q4 FY26): ₹28,744 Lakh

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹7,414 Lakh

- QoQ Change: +44.66%

- YoY Change: +23.86%

- Previous Quarter (Q3 FY26): ₹5,125 Lakh

- Previous Year (Q4 FY25): ₹5,986 Lakh

- PAT (Q4 FY26): ₹7,414 Lakh

- QoQ Performance:

- Revenue Trend: Sequential Growth with strong operational momentum

- Profit Trend: Strong Sequential Expansion

Margin Analysis

Drivers:

- Music segment EBIT improved strongly during the quarter.

- Advertising and sales promotion expenses declined materially QoQ.

- Royalty costs reduced compared to previous quarters.

- Artist management delivered high growth contribution.

- Finance costs remained low despite business expansion.

- Operational cost growth remained under control relative to revenue growth.

Insight:

- The company demonstrated strong operating leverage as revenue growth translated efficiently into higher profitability and improved earnings quality.

Segment performance

Segments: Music

- Revenue: ₹20,043 lakh

- Insights:

- Music remained the largest contributor to overall revenue and profitability.

- Segment revenue grew strongly YoY from ₹16,806 lakh.

- Segment profit expanded sharply to ₹12,798 lakh.

- Continued monetisation across streaming, licensing, and catalogue consumption supported growth.

Segments: Artist Management

- Revenue: ₹4,246 lakh

- Insights:

- Artist management emerged as the fastest-growing segment.

- Revenue more than doubled YoY from ₹1,883 lakh.

- Segment profitability improved significantly to ₹442 lakh.

- Growth indicates increasing traction in live entertainment and celebrity management ecosystem.

Segments: Video

- Revenue: ₹3,225 lakh

- Insights:

- Video revenue declined YoY from ₹4,916 lakh.

- However, segment profitability turned positive versus loss in previous year.

- Indicates improved cost discipline and selective content investment.

Segments: Events

- Revenue: ₹1,231 lakh

- Insights:

- Events business remained weak compared to FY25.

- Segment reported operating loss during the quarter.

- Demand normalisation and execution timing likely impacted performance.

Segment insight

Business Summary:

The company’s business mix is increasingly shifting toward scalable digital music monetisation and artist-led entertainment ecosystems, while video and events remain cyclical and execution dependent.

Key Characteristics:

- Music business remains the core profit engine.

- Artist management is becoming a strategic growth vertical.

- Video business profitability is improving despite revenue pressure.

- Events business continues to face volatility.

- Digital streaming monetisation continues to strengthen earnings visibility.

Earning quality check

Key Drivers:

- Operating cash flow remained positive at ₹10,002 lakh.

- Strong profitability translated into healthy operational cash generation.

- Lower bank balances indicate strategic deployment of capital.

- Acquisition-related investments impacted investing cash flows.

- Finance costs remained very low relative to operating profits.

Interpretations:

- The earnings quality remains healthy as profits are backed by operating cash generation and expanding operating margins despite ongoing investment activity.

balance sheet Analysis

- Total Assets: ₹2,32,196 lakh

- Total Liabilities: ₹62,675 lakh

Insight:

- The company maintains a strong balance sheet with substantial equity reserves, manageable liabilities, and strong asset growth driven by investments, intangible assets, and business expansion initiatives.

key risks

- Dependence on digital platform monetisation trends.

- Content success remains inherently unpredictable.

- Events business continues to show earnings volatility.

- Increased investment in acquisitions and entertainment assets may pressure near-term cash flows.

- Competitive pressure from streaming and digital content platforms.

- Dependence on artist monetisation cycles and audience engagement.

management strategy signals

Focus Area:

- Expansion of music catalogue monetisation.

- Scaling artist management business.

- Improving monetisation of intellectual property assets.

- Selective investments in content and acquisitions.

- Strengthening digital entertainment ecosystem.

- Margin-focused operational execution.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹29,658 Lakh | +10.75% | +14.75% |

| PBT | ₹10,341 Lakh | +48.72% | +26.70% |

| PAT | ₹7,414 Lakh | +44.66% | +23.86% |

Saregama India Limited delivered a strong Q4 FY26 performance with healthy revenue growth, sharp profitability expansion, and strong momentum in music and artist management businesses.

The company’s transition toward a scalable digital entertainment ecosystem continues to strengthen earnings quality and long-term monetisation potential, although volatility in events and video operations remains a key monitorable factor.

Official Exchange Filing: Saregama India Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED